For investors looking to balance the search for growth with a degree of caution, the "Growth at a Reasonable Price" (GARP) method presents a thoughtful middle path. This method tries to find companies that are increasing their earnings and revenue faster than average, but whose stock prices do not reflect extreme valuations. It steers clear of the high-risk edges of pure momentum investing while still focusing on businesses with good forward progress. One instrument for applying this method is an "Affordable Growth" stock filter, which selects for equities showing good growth, firm profitability and financial soundness, and a valuation that seems fair. Vertex Pharmaceuticals Inc (NASDAQ:VRTX) appears as a candidate from this filter, justifying a more detailed examination to understand how its basic facts fit this investment idea.

Growth Path and Expectations

The central idea of any growth method is, expectedly, growth. For a GARP investor, the attention is on lasting, high-caliber increase rather than temporary jumps. Vertex Pharmaceuticals displays a detailed but finally solid growth picture. The company's revenue growth is a main positive, having risen by 10.33% over the last year and displaying a good average yearly growth rate of 21.50% over recent years. While future revenue growth is predicted to slow to a still-sound 9.75% each year, the forecast for earnings is especially notable.

- Past Earnings Growth: The company recorded a remarkable 3,303.92% increase in Earnings Per Share (EPS) over the last year, though this comes after a time of negative average yearly EPS growth, pointing to variability.

- Future Earnings Increase: More critical for future-focused investors, analysts predict a very solid comeback. EPS is forecast to increase at an average pace of 150.51% each year in the near future, signaling a notable rise in profitability.

- Growth Rating: This mix of solid past revenue increase and strong predicted earnings rise adds to Vertex's firm Growth Rating of 7 out of 10 in its fundamental analysis report.

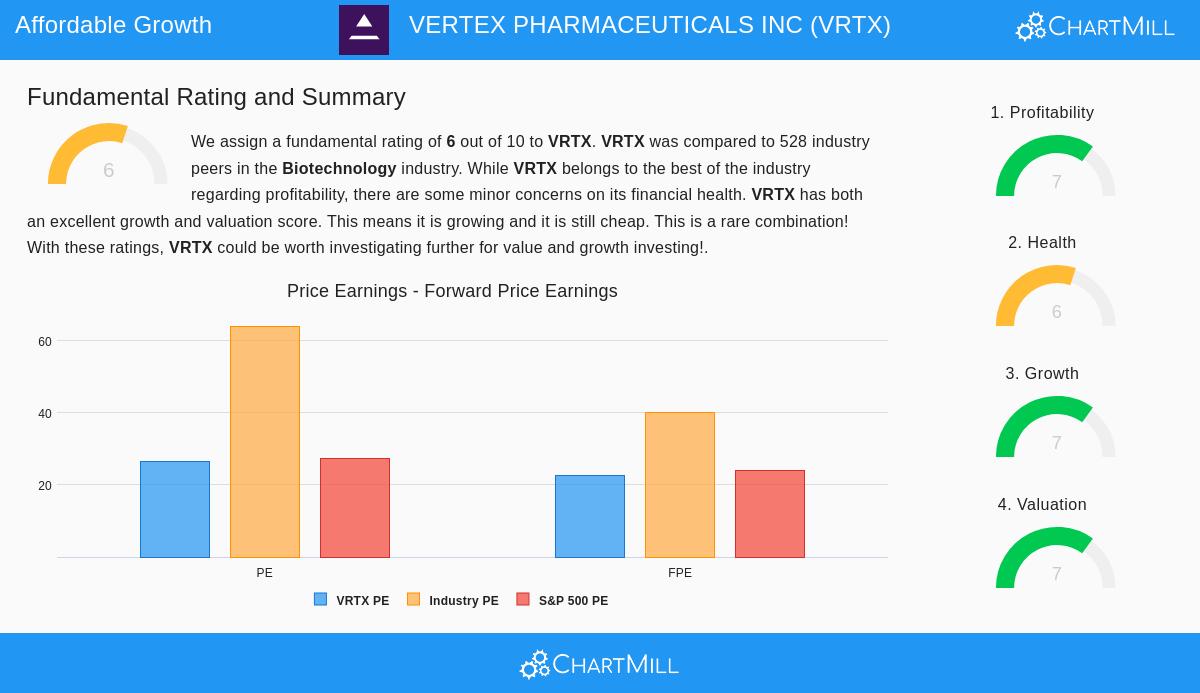

Valuation in Perspective

A fair valuation is what divides a GARP candidate from an overvalued growth stock. Vertex's valuation numbers show an interesting view that leans positive when considered with comparison. While its absolute Price-to-Earnings (P/E) ratio of 26.53 may appear high alone, perspective is key.

- Industry Comparison: Vertex sells at a notable markdown compared to its biotech counterparts. Its P/E ratio is lower than 93.56% of companies in the biotechnology field, where the average P/E is above 64.

- Broader Market Comparison: Its P/E is also nearly equal to the current S&P 500 average of 27.25, implying the market is not adding a high extra cost for its growth potential.

- Growth-Considered Measures: The valuation argument becomes stronger when growth is included. The company's low PEG ratio, which modifies the P/E for predicted earnings growth, suggests a fairly low valuation. Also, measures like Enterprise Value to EBITDA and Price to Free Cash Flow also indicate Vertex is valued lower than over 93% of its industry rivals.

- Valuation Rating: This comparative value idea is seen in its Valuation Rating of 7, implying the stock is not overpriced considering its growth picture.

Basic Financial Soundness and Profitability

Lasting growth cannot happen without a strong financial base and the capacity to produce profits. This is where the "affordable" part of the filter is supported by quality measures. Vertex is strong in profitability, having margins that are with the best in its industry.

- Notable Margins: The company holds a gross margin of 86.28%, an operating margin of 38.70%, and a profit margin of 31.35%, each one better than most industry peers.

- Solid Returns: Its returns on assets (14.78%), equity (21.22%), and invested capital (17.58%) are all high-quality, showing very effective use of capital.

- Cautious Balance Sheet: From a soundness view, Vertex carries no debt, putting its solvency measures with the best available. Its current and quick ratios show enough liquidity to cover near-term needs, though they are average compared to some industry companies. This careful financial setup offers notable stability and room to act.

These positives in profitability (Rating: 7) and financial soundness (Rating: 6) give important support for the growth story. They show that Vertex's increase is supported by a profitable, well-run operation with a strong balance sheet, lowering the risk for investors.

Summary and Next Steps

Vertex Pharmaceuticals Inc shows the key features of an "affordable growth" candidate. It combines a strong predicted rise in earnings with a valuation that is fair both inside its high-growth field and compared to the wider market. This possibility for growth at a logical price is supported by notable profitability measures and a very strong, debt-free balance sheet. For investors using a GARP method, these traits—solid forward growth, comparative value, and basic quality—form a thoughtful picture deserving more detailed investigation.

The hunt for companies matching this picture continues. Investors curious about finding other stocks that satisfy similar standards of acceptable growth, good profitability and soundness, and fair valuation can look further using the Affordable Growth stock filter.

Disclaimer: This article is for information only and does not form financial guidance, a suggestion, or an offer or request to buy or sell any securities. The information shown is based on supplied data and should not be the only foundation for any investment choice. Investors should perform their own study and talk with a qualified financial consultant before making any investment decisions.