For investors looking to find possible opportunities in the market, a disciplined method focused on fundamental value can offer a structured system. One such technique involves searching for companies that seem priced below their intrinsic worth, while still showing good basic business condition. This plan, frequently used by value investors, searches for stocks where the market price may not completely show the company's financial might, earnings power, and future possibilities. The aim is to find cases where a short-term price reduction offers a margin of safety for a long-term holding.

A recent search using this "decent value" method has pointed to Vertex Pharmaceuticals Inc (NASDAQ:VRTX) as a candidate worth more detailed study. The search specifically looked for stocks with a good valuation score, indicating they trade at appealing multiples compared to similar companies, while also needing acceptable scores in earnings power, financial condition, and expansion. This mix tries to steer clear of the classic "value trap," where a low-priced stock is inexpensive for a basically worsening reason. Instead, it looks for companies that are financially stable and expanding, yet priced cautiously by the market.

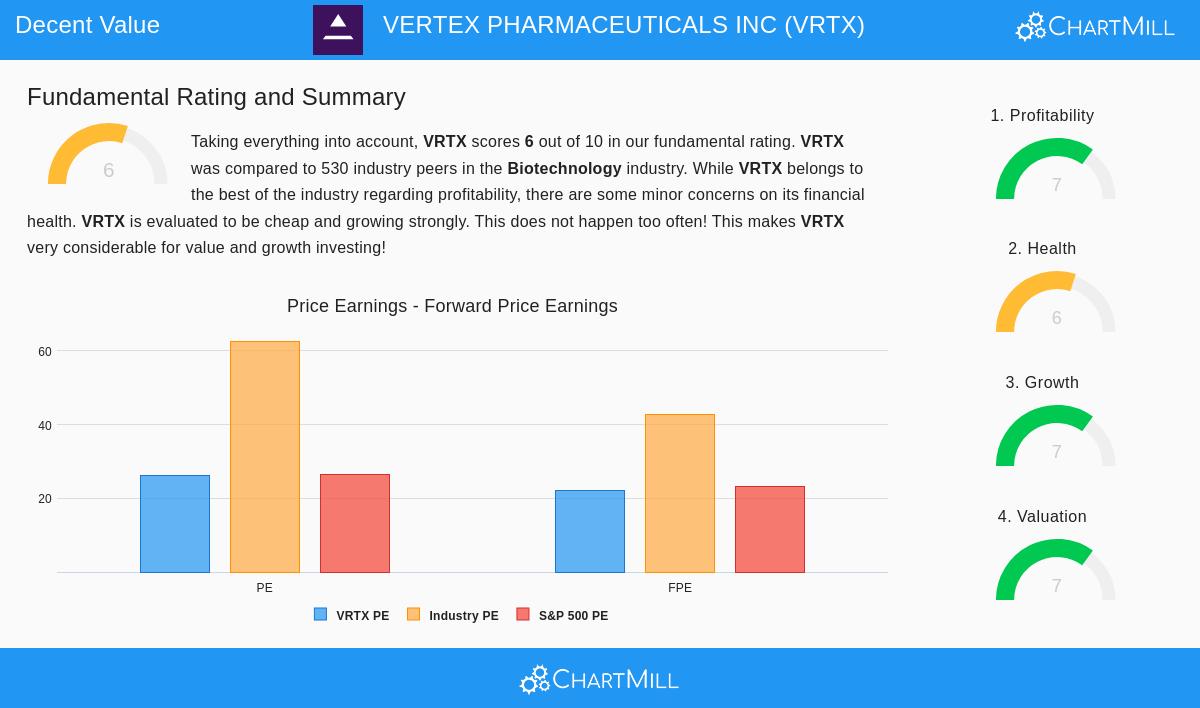

Valuation: A Relative Discount in Biotech

The central idea of value investing is buying an asset for less than its calculated intrinsic worth. For Vertex, the quantitative argument for being undervalued is strong, especially inside its high-expansion industry. The company's valuation measures compare well against the wider biotechnology field.

- Price-to-Earnings (P/E) Ratio: At 26.12, Vertex's P/E ratio is noticeably below the industry average of about 62.62. This means 93.4% of its biotech peers are valued more highly on this common earnings multiple.

- Forward P/E Ratio: Looking forward, Vertex's forward P/E of 22.17 is also much lower than the industry's forward average of 42.81, again putting it in the more reasonably priced part of its sector.

- Enterprise Value to EBITDA & Price/Free Cash Flow: The company receives high marks on other valuation multiples. Its Enterprise Value/EBITDA and Price/Free Cash Flow ratios are viewed as low relative to over 93% of industry rivals.

While a P/E in the mid-20s might not seem "low" in absolute terms, context is key. In a field known for high valuations, often explained by high-risk, high-reward pipelines, Vertex's mix of good current earnings power and a reduced price is uncommon. The valuation score of 7/10 from ChartMill's fundamental analysis report highlights this relative chance.

Financial Health: A Strong Balance Sheet

A solid financial base is essential for a value investment, as it offers stability during market declines and pays for future expansion without too much risk. Vertex does very well here, having a balance sheet that many companies admire, not only those in the capital-heavy biotech area.

- Zero Debt: Vertex has no outstanding debt. This removes interest cost risk and gives great strategic freedom.

- Creating Value: The company's Return on Invested Capital (ROIC) of 17.58% is much higher than its cost of capital, proving it is effectively creating value for shareholders.

- Shareholder-Friendly Actions: The company has been lowering its share count over the past one and five years, a move that can raise the ownership stake and earnings per share for remaining investors.

The main point of care in the condition review relates to liquidity ratios like the Current and Quick ratios, which, while at levels showing no short-term payment problems, are below many industry peers. However, for a company with no debt and good cash flows, this is a small point rather than a major weakness, adding to its overall condition score of 6/10.

Profitability: Top-Tier Margins

Earnings power is the motor that pushes intrinsic value. A company can be low-priced and healthy, but without the ability to produce profits, it has little attraction. Vertex shows excellent earnings power, which helps support its business model and future potential.

- High Margins: The company's Profit Margin (31.35%) and Operating Margin (38.70%) are in the top 4% of the biotechnology industry.

- High Returns: Its Return on Assets (14.78%) and Return on Equity (21.22%) are also top-level, doing better than over 95% of peers.

- Stable Model: These high margins have been kept or gotten better recently, showing a lasting and scalable business model around its main cystic fibrosis franchise.

This excellent earnings power, receiving a score of 7/10, is a key distinguishing feature. It indicates that Vertex's profits are high-quality and can continue, a vital factor when judging whether a low valuation is a market mistake or a logical reaction to weak basics.

Growth: A Strong Motor with a Hopeful Future

Lastly, for a value stock to achieve its potential, it needs an expansion path that can drive a re-rating from the market. Vertex shows a detailed but finally positive expansion picture.

- High Recent EPS Growth: Over the past year, Earnings Per Share rose by a very high 3303.92%, though from a smaller base after the launch and growth of its key drug, Trikafta.

- Good Revenue Path: Revenue grew 10.33% last year and has increased at a notable average of 21.50% over recent years.

- Bright Future Earnings: Analysts predict very good EPS growth of about 150.35% on average in the coming years, pointing to speeding up earnings power.

The expansion story recognizes a slowdown in top-line growth is expected, with future revenue growth forecast near 9.70%. However, the large predicted profit growth points to major operating leverage and margin improvement from its existing sales base. This mix of good past performance and a hopeful earnings view supports its expansion score of 7/10.

Conclusion: A Strong Case for More Study

Vertex Pharmaceuticals offers a strong example for the "decent value" search method. It is not a deeply troubled asset trading at breakup value, but instead a high-quality, profitable industry leader trading at a clear discount to its sector. The search effectively found a company where the valuation seems separate from its financial might, excellent earnings power, and notable expansion prospects, exactly the outline value investors look for to avoid speculative traps and find lasting chances.

The market may be applying a discount because of worries over the long-term expansion of its main franchise or the risks present in its clinical pipeline. However, the basic measures suggest the underlying business is very stable. For investors, this difference between business results and market price makes the potential for a good risk/reward situation if the company's expansion plans happen.

Interested in finding other stocks that match this disciplined value method? You can use the same "Decent Value" search used to find Vertex to look for more possible chances. Click here to see the search and view the current results.

Disclaimer: This article is for informational and educational reasons only and does not form financial advice, a suggestion, or an offer or request to buy or sell any securities. The information shown is based on data supplied and should not be the only base for any investment choice. Investing in stocks includes risk, including the possible loss of principal. Always do your own complete research and think about talking with a qualified financial advisor before making any investment choices.