In the world of investing, the search for undervalued opportunities is a constant pursuit. One systematic approach involves screening for companies that appear fundamentally sound yet trade at a discount to their intrinsic value. This "decent value" strategy specifically targets stocks with good underlying business health and profitability, but whose market price does not fully reflect these qualities. By focusing on a good valuation rating alongside solid scores for financial health, profitability, and growth, investors aim to identify companies that are not simply cheap, but cheap for the wrong reasons. Instead, these are businesses with the operational strength to potentially see their market valuation realign with their fundamental worth over time.

Urban Outfitters Inc. (NASDAQ:URBN) presents an interesting case study for this methodology. The specialty retailer, which operates brands like Anthropologie, Free People, and its namesake Urban Outfitters, has built a diverse portfolio spanning retail, wholesale, and the Nuuly subscription rental service. A detailed review of its financials suggests the market may be undervaluing the company's consistent operational performance and strong balance sheet.

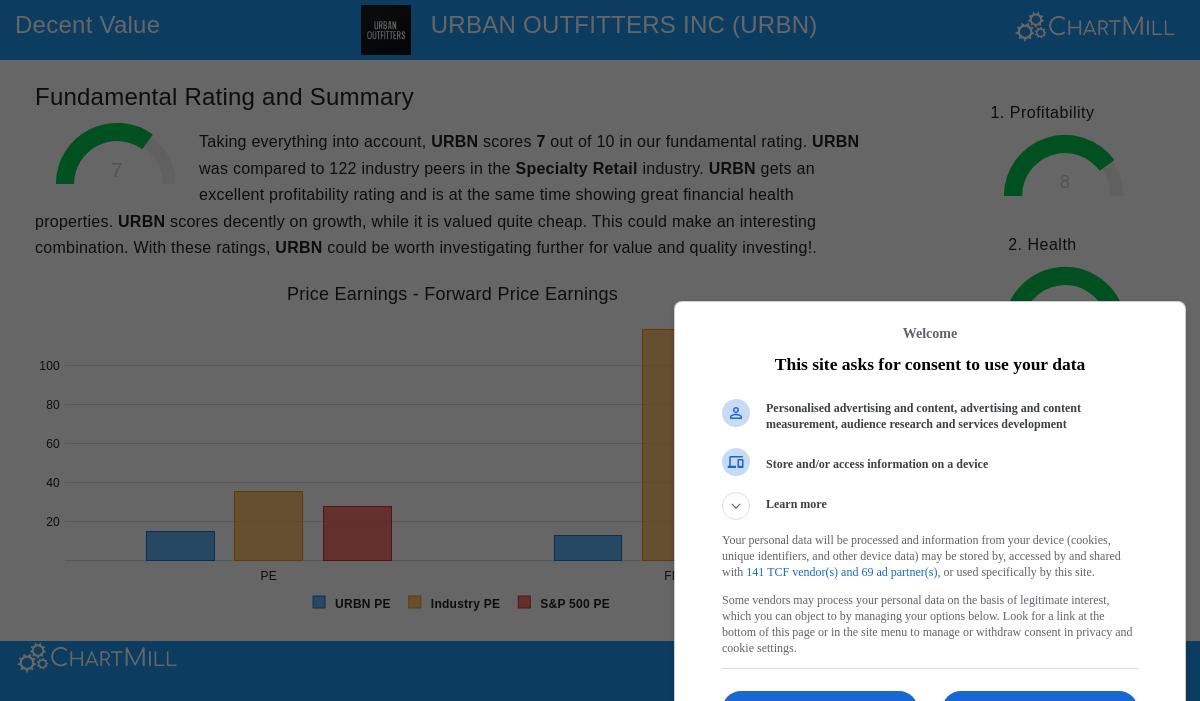

Valuation: A Price Tag Out of Sync with Peers

The core of any value investment thesis is an attractive valuation, and URBN scores well here with a ChartMill Valuation Rating of 7 out of 10. The company's stock appears inexpensive relative to both its industry and the broader market, a key starting point for investors seeking a margin of safety.

- Price-to-Earnings (P/E): URBN's P/E ratio of 14.46 is significantly cheaper than the average for its Specialty Retail industry (35.15) and the S&P 500 (27.30). It is cheaper than over 80% of its direct competitors.

- Forward P/E: Looking ahead, the picture remains similar. A forward P/E of 12.37 compares favorably to an industry average that is nearly ten times higher and a market average of 24.04.

- Cash Flow & EBITDA: The valuation attractiveness extends to cash-based metrics. The company's Price-to-Free Cash Flow and Enterprise Value-to-EBITDA ratios are also cheaper than a majority of its industry peers.

This discounted valuation is especially notable because it is not paired with weak profitability. In fact, the company's strong earnings power makes these low multiples stand out, suggesting the market may be overlooking its fundamental strength.

Financial Health: A Strong Balance Sheet

For a value investor, a cheap stock is only a good investment if the company is financially sound enough to endure market cycles and execute its strategy. URBN performs well in this area, holding a top-tier ChartMill Health Rating of 9. Its financial foundation is very strong, mitigating a key risk in value investing.

- Zero Debt: Perhaps the most striking feature is URBN's balance sheet, which carries no interest-bearing debt. This gives the company significant operational flexibility and removes the risk of financial distress.

- Strong Solvency: The company's Altman-Z score of 4.32 indicates a very low risk of bankruptcy and places it in the top 15% of its industry for financial stability.

- Shareholder-Friendly Actions: Management has been reducing the number of shares outstanding, an action that, all else being equal, increases the ownership stake and earnings per share for remaining investors.

This clean financial health provides the stability value investors seek, ensuring the company can invest in growth, weather economic downturns, or return capital to shareholders without the overhang of debt obligations.

Profitability: Consistent and Improving Earnings Power

A low valuation is meaningless if a company cannot generate profits. URBN's operational performance is good, earning a ChartMill Profitability Rating of 8. The company not only earns money but does so at rates that often exceed its competitors, justifying a closer look from investors focused on quality.

- Superior Returns: The company generates attractive returns on its assets (ROA of 9.96%) and invested capital (ROIC of 11.96%), outperforming over 80% of the specialty retail industry. Its Return on Equity is a healthy 18.08%.

- Expanding Margins: Both operating margin (9.57%) and profit margin (8.15%) are in the top tier of the industry. Importantly, these margins have been growing over recent years, indicating improving operational efficiency and pricing power.

This consistent and superior profitability is critical for the value thesis. It confirms that the business is high-quality and that the discounted valuation is not a reflection of poor operations, but potentially a market oversight.

Growth: A Stable Trajectory with Positive Momentum

While not a high-growth story, URBN demonstrates a steady and respectable growth profile that complements its value characteristics, scoring a 6 for Growth. Value investments do not require explosive growth, but a stable or improving trajectory helps support the case for future valuation expansion.

- Strong Recent EPS Growth: Earnings per share grew by an impressive 36% over the past year, building on a solid historical average annual growth rate of 15.5%.

- Revenue Acceleration: Revenue growth is expected to accelerate, with forecasts pointing to an average annual increase of 8.24% in the coming years, up from the recent historical trend.

- Sustainable Forward Outlook: Analysts expect EPS to continue growing at a rate near 11% annually, a pace that is considered quite good for a company trading at its current valuation multiples.

This growth profile suggests URBN is not a stagnant business. The combination of accelerating revenue expectations and continued earnings growth provides a pathway for the market to reappraise the stock, potentially closing the gap between its price and intrinsic value.

Conclusion: A Case for Fundamental Reassessment

Urban Outfitters Inc. embodies the characteristics sought by a disciplined value strategy. It trades at a clear discount to its industry and the market, as evidenced by its valuation metrics. However, this discount exists alongside a strong balance sheet with no debt, industry-leading profitability with expanding margins, and a stable, improving growth outlook. This disconnect, a high-quality business with a low-quality valuation multiple, is exactly what value screens are designed to uncover.

The company's strong financial health provides downside protection, while its profitability and growth prospects offer a rationale for why the valuation gap might close over time. For investors employing a "decent value" approach, URBN represents a candidate where the numbers suggest the current market price may not fully reflect the underlying strength and future potential of the enterprise.

Interested in exploring more stocks that fit this profile? You can run the "Decent Value" screen yourself to see other potential opportunities here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions. The fundamental data and ratings referenced are provided by ChartMill and are based on the company's publicly available financial reports.