The search for quality companies trading at reasonable prices is a foundation of many long-term investment methods. One well-regarded method is the "Growth at a Reasonable Price" (GARP) strategy, made famous by noted investor Peter Lynch during his time at the Magellan Fund. His approach centers on finding companies with good, lasting earnings growth, sound financial condition, and profit, all while making sure the stock price does not overvalue those future results. By using a disciplined filter based on Lynch's ideas, investors can sort the market for possible choices that mix growth possibility with sensible valuation.

A Profile Based on Lynch: Urban Outfitters Inc (NASDAQ:URBN)

Urban Outfitters Inc (URBN) runs a group of lifestyle retail brands including Anthropologie, Free People, FP Movement, and its namesake Urban Outfitters stores, as well as a developing subscription rental service named Nuuly. A recent filter built on Peter Lynch's standards has identified URBN as a company deserving more examination from investors focused on GARP. The filter looks for firms with a particular mix of growth, value, and financial soundness, which URBN seems to meet.

Fitting the Lynch Standards

Peter Lynch stressed lasting growth, careful finances, and good valuation. The filter used several important measures, and URBN's current numbers match these goals.

- Lasting Earnings Growth: Lynch looked for companies increasing earnings per share (EPS) between 15% and 30% each year over five years, a rate good enough to be interesting but not so high as to be temporary. URBN's five-year EPS growth rate of 15.5% sits exactly at the start of this range, pointing to a consistent, controlled increase.

- Valuation Matched by Growth: Maybe the most important Lynch number is the Price/Earnings to Growth (PEG) ratio, which tries to find stocks where the price is fair relative to the growth rate. A PEG ratio at or under 1.0 is usually seen as good. URBN's PEG ratio, based on its past five-year growth, is about 0.92, showing the market might be pricing its historical growth path too low.

- Strong Profitability: Lynch wanted a high return on equity (ROE) to make sure management was using shareholder money well. The filter set a minimum of 15%. URBN's ROE of 18.1% easily passes this level, indicating good profit generation.

- Financial Condition: To avoid companies with too much debt, the filter required a debt-to-equity ratio below 0.6, with Lynch himself liking levels under 0.25. Notably, URBN reports a debt-to-equity ratio of 0.0, showing it works with no interest-bearing debt, a sign of careful financial management. Also, its current ratio of 1.51 meets the filter's need to be above 1.0, showing enough short-term cash to pay bills.

Fundamental Condition Review

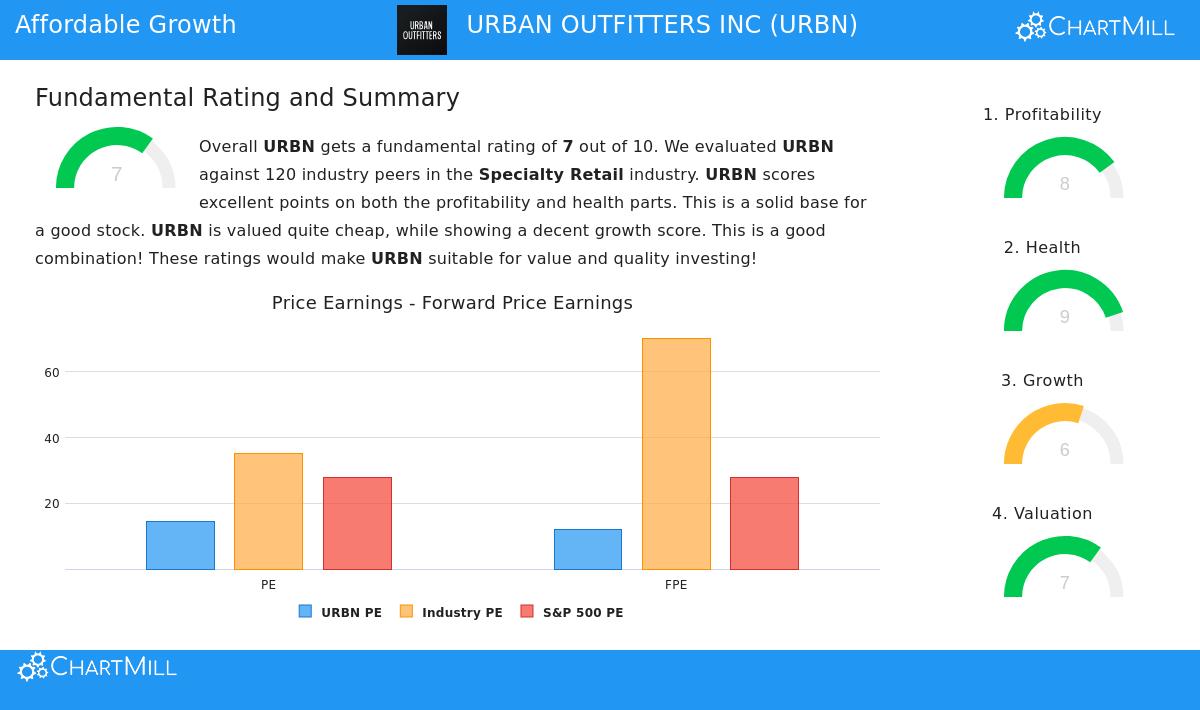

A wider fundamental analysis of URBN supports the view from the Lynch filter. The company gets a good overall fundamental score of 7 out of 10, doing especially well in profitability and financial health.

- Profitability & Margins: URBN's profit numbers are strong. Its profit margin of 8.15% and operating margin of 9.57% are in the higher part of the specialty retail industry. Both margins have gotten better in recent years, and important returns on assets, equity, and invested capital are all solid.

- Excellent Balance Sheet: The lack of debt is a major positive, leading to a very good Altman-Z score of 4.30, which shows a very small chance of near-term business failure. The company has also been lowering its share count over time, a move Lynch liked as it can increase value for each share.

- Growth and Valuation View: While past EPS growth has been good, future projections point to a slowdown to a still-reasonable rate near 11%. On valuation, URBN sells at a P/E ratio of 14.3, which is less expensive than about 80% of its industry competitors and much lower than the current S&P 500 average. When paired with its good profitability, this offers an interesting value case.

Is URBN a Stock Fitting Lynch's "GARP" Idea?

For investors following Peter Lynch's ideas, Urban Outfitters offers an interesting study. It shows several of his main beliefs: a business in retail that is easy to understand, a record of steady EPS growth, and a clean balance sheet with no debt. The low PEG ratio suggests the market has not priced this growth too high, and the high ROE confirms the company's effective operations.

However, Lynch also suggested thorough study beyond the figures. Investors would need to judge the staying power of URBN's brand strength, its plan to compete with large online sellers, and the future of its Nuuly subscription business. The company works in the competitive and changing retail industry, which has its own risks.

Looking for More

URBN came from a particular set of filters made to copy a traditional investment method. For investors wanting to find other companies that pass this "Peter Lynch" check, you can see the full filter and its current findings here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.