For investors aiming to create a portfolio that produces steady passive income, a methodical screening process is necessary. One useful method is to find companies that provide an appealing dividend now and also have the fundamental financial soundness to maintain and possibly increase those payments in the future. This method frequently includes selecting for stocks with high dividend ratings, which combine elements like yield, growth, and payout safety, while also confirming the company holds satisfactory scores for earnings power and financial soundness. These extra ratings are important; solid earnings power finances the dividend, and a sound balance sheet offers protection in difficult economic periods.

A stock that appears from such a methodical screen is United Parcel Service Inc. (NYSE:UPS), the worldwide logistics and package delivery leader. The company's basic profile makes a strong case for dividend-oriented investors, mixing a high present yield with the operational size of a sector frontrunner.

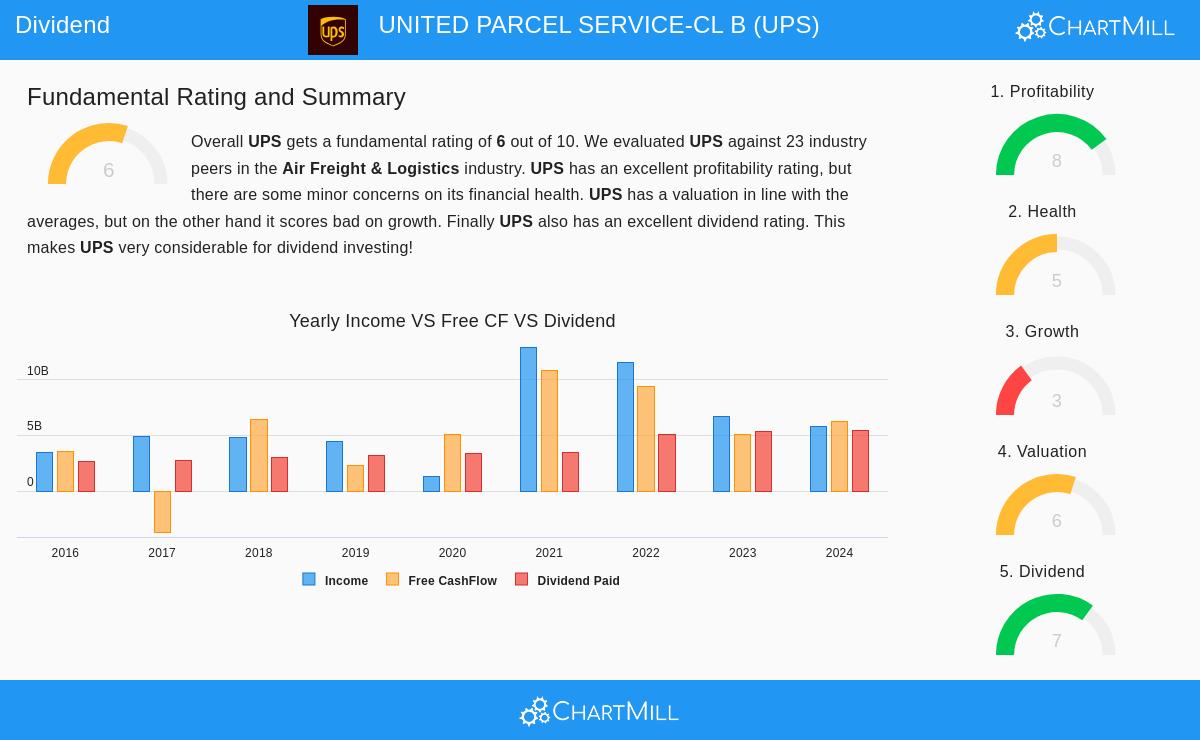

A Notable Dividend Profile

The central attraction of UPS for income investors is clear in its dividend measures. The company receives a solid ChartMill Dividend Rating of 7 out of 10, indicating a high-quality income payment compared to the wider market.

- Appealing Current Yield: UPS provides a significant yearly dividend yield of 6.13%. This is over three times the present average yield of the S&P 500 (about 1.92%) and is notable inside its Air Freight & Logistics sector, where it pays more than 95% of similar companies.

- Dependable and Increasing Payout: The company has established a reliable history, having paid and, critically, raised its dividend for at least ten straight years. This record of yearly increases, averaging a solid 11.17% over the last five years, shows a dedication to giving capital back to shareholders.

- A Point on Safety: While the yield and growth record are very good, the basic report does indicate a key area to watch: the payout ratio. Presently, UPS uses about 98% of its earnings for dividends. This is a high amount that implies little margin for shortfall if earnings were to fall, and it highlights why the screen's extra filters for earnings power and soundness are so important. A high payout ratio is less worrisome if the company is strongly profitable and financially secure.

Supporting Basics: Earnings Power and Soundness

The screening rules ask for more than just a high dividend score; they need "satisfactory" earnings power and soundness. For UPS, "satisfactory" is a modest description regarding earnings power, while its soundness rating shows a firm but varied financial state.

Strong Earnings Power (Rating: 8/10): This is a major positive for UPS. The company's capacity to produce profits is well above normal, supplying the necessary earnings base that upholds its dividend. Important figures include:

- A Return on Equity (ROE) of 34.77%, which beats 95% of sector rivals.

- Good profit and operating margins that also place in the top group of its sector.

- A steadily positive cash flow from operations over the past five years.

This notable earnings power is the base that allows its high dividend payout to work. A company cannot maintain substantial shareholder payments without first being very good at creating profits from its business.

Satisfactory Financial Soundness (Rating: 5/10): The financial soundness rating shows a mixed view. On the good side, UPS builds value, as its Return on Invested Capital (ROIC) is higher than its cost of capital. Its Altman-Z score shows a low short-term chance of bankruptcy. However, the report mentions a somewhat high level of financial borrowing, with a Debt-to-Equity ratio of 1.51. While not unusual for industries requiring large capital investment, this borrowing is something for investors to acknowledge, as it makes the company more affected by interest rates and economic changes. The screen’s need for a minimum soundness rating of 5 helps remove companies with more serious balance sheet dangers, confirming a basic level of financial steadiness.

Price and Growth Setting

From a price standpoint, UPS seems fairly valued. Its Price-to-Earnings (P/E) ratio of 14.35 is lower than both the S&P 500 average and the sector average, implying the stock is not priced too high. This is especially significant given its high earnings power and dividend yield.

The main challenge mentioned in the basic study is growth, or the comparative absence of it. The company has seen a small decrease in revenue over the last year, and future growth projections for both revenue and earnings are low. This matches UPS's place as an established, cyclical company in a competitive international market. For a dividend investor, this exchange is often acceptable—the focus is on income and steadiness rather than large share price gains.

Is UPS Suitable for a Dividend Portfolio?

United Parcel Service Inc. illustrates the kind of company a methodical dividend screen tries to find. It provides a high, well-supported yield supported by a ten-year record of growth, all upheld by the strong earnings power of a global logistics frontrunner. The screening process properly points out both its positives—the excellent dividend and profit figures—and the areas needing investor careful review, specifically the high payout ratio and increased debt levels.

For an investor whose main objective is producing income, UPS offers a strong candidate. Its high present yield, confirmed history of raises, and the economic strength given by its large delivery network are important benefits. The analysis indicates it is a company made to withstand economic fluctuations and keep providing shareholders with cash payments.

Interested in examining other stocks that fit similar rules for high dividend quality, earnings power, and financial soundness? You can use the same "Best Dividend Stocks" screen yourself here to see the complete list of findings.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. All investments involve risk, including the potential loss of principal. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions. The fundamental data and ratings referenced are based on past performance and analyst estimates, which are not guarantees of future results.