For investors looking for a dependable source of passive income, a systematic screening strategy is necessary to steer clear of the dangers of high-yield traps. One useful technique involves selecting for stocks that provide an appealing dividend and are also supported by good core business condition and earnings. This method focuses on long-term viability over maximum yield, seeking to find companies with the monetary resources to continue and possibly increase their distributions over time. A screen set for a high ChartMill Dividend Rating, along with minimum levels for Profitability and Health Ratings, achieves this goal, revealing companies that mix income production with basic quality.

A recent result from this type of screen is United Parcel Service Inc. (NYSE:UPS), the worldwide logistics and package delivery leader. The company's basic profile, especially its dividend attributes, deserves additional examination from investors focused on income.

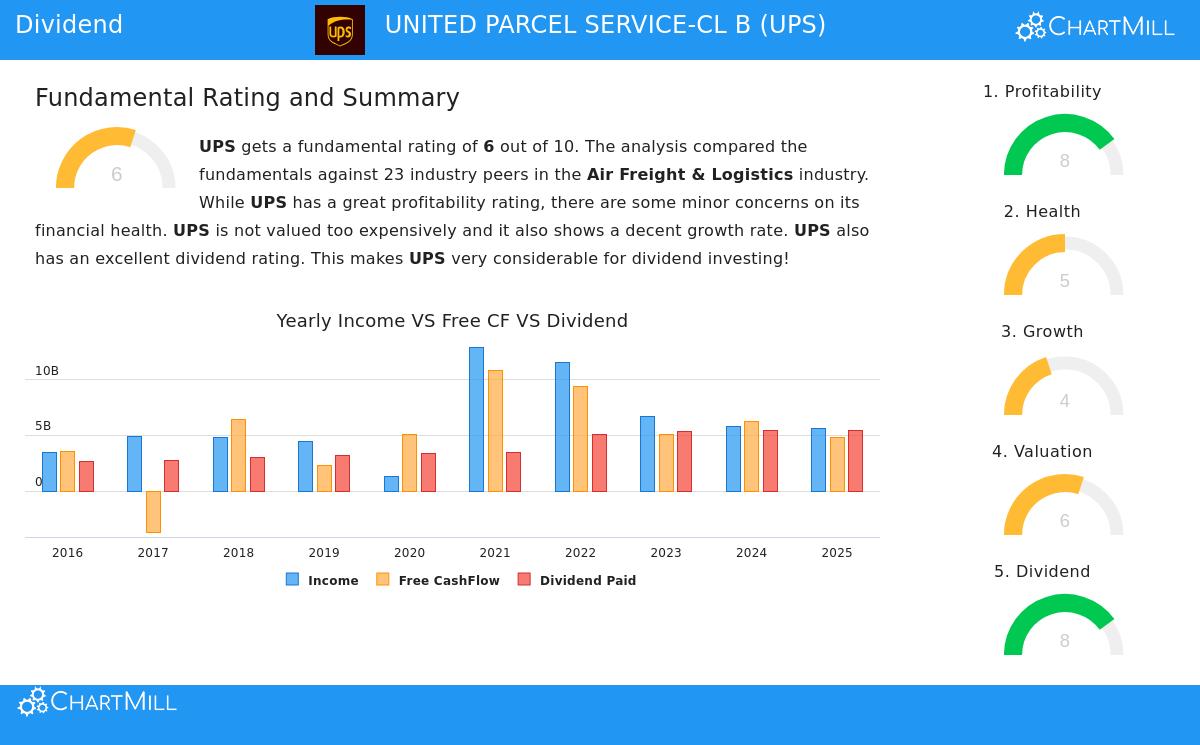

Dividend Strength and Sustainability

The central attraction of UPS for dividend investors is its convincing and well-backed income offering. The company's dividend measurements show a background of consistency and a favorable path for future distributions.

- Appealing Current Yield: UPS provides a considerable yearly dividend yield of about 5.68%. This is much higher than both the S&P 500 average (near 1.80%) and the average for its Air Freight & Logistics industry counterparts (roughly 1.08%), putting it in the leading group of dividend payers in its field.

- Notable Growth History: The dividend is not fixed. UPS has shown a solid dedication to giving more capital to shareholders, with a yearly dividend growth rate of 10.10% over the last five years. Also, the company has a consistent history, having paid, and not reduced, its dividend for at least ten years.

- Earnings Growth Match: A key test for viability is comparing dividend growth to earnings growth. Analysts forecast UPS's earnings per share (EPS) to increase by about 10.78% each year in the near future. This match indicates the current solid dividend growth rate is backed by anticipated gains in earnings, a good signal for its ongoing nature.

However, a point for care comes from the payout ratio, which is currently at a high 96.88% of net income. This shows that almost all of the company's recent earnings are being paid out as dividends, allowing little room for unexpected issues. While this is an item to watch, it is lessened by the solid projected earnings growth and the company's past strong cash flow production, which is a more direct source for dividend payments.

Supporting Basic Pillars: Profitability and Health

A high dividend yield by itself is not a complete investment argument; it must be backed by a lasting business. This is why the screening rules include evaluations for profitability and monetary condition, two areas where UPS displays notable ability with some detailed points.

Profitability Quality: UPS gets a high ChartMill Profitability Rating of 8, highlighting its operational effectiveness and market standing.

- The company’s Return on Equity (ROE) of 34.34% and Return on Invested Capital (ROIC) of 10.69% are some of the top in its industry, showing very efficient use of investor capital.

- Margins are strong, with a Profit Margin of 6.28% and an Operating Margin of 8.91%, both doing better than most industry rivals.

Satisfactory Monetary Condition: UPS receives a ChartMill Health Rating of 5, showing an acceptable but varied monetary state. This rating confirms the screen's filter for "decent" health, making sure the company is not in a weak position.

- Solvency is good: The company's Altman-Z score of 3.03 points to a low short-term chance of monetary trouble and is more favorable than many peers. Its Debt to Free Cash Flow ratio is also workable.

- Leverage and Liquidity are points to note: The Debt/Equity ratio is high at 1.45, showing a notable use of debt financing. Also, its Current and Quick Ratios, while sufficient for covering immediate debts, are less than those of many industry competitors. These elements are weighed against the company's solid and steady cash flow, which is key for handling debt and financing activities.

Valuation Context

For income investors, valuation is significant to make sure they are not paying too much for the dividend stream. UPS seems fairly valued in the present market.

- The stock sells at a P/E ratio of 15.90 and a Forward P/E of 15.96, which is below the wider S&P 500 and less expensive than most of its industry peers.

- Other valuation measures, like Price/Free Cash Flow and Enterprise Value/EBITDA, also indicate UPS is valued favorably within its sector. This fair valuation, mixed with its high yield, adds to a convincing income offering.

Conclusion

United Parcel Service Inc. offers a detailed case for dividend investors. It mixes a high, increasing yield with a long history of distribution consistency. This appealing income profile is built on a base of outstanding profitability and a satisfactory, though debt-influenced, monetary condition position. The screen’s approach, focusing on a high dividend rating along with checks for profitability and health, is made to find exactly this kind of result: one where the dividend is not an isolated trait but is connected with a basically good business.

While the high payout ratio and raised debt level deserve continued observation, the company’s solid market place, projected earnings growth, and fair valuation provide balancing positives. For investors building a portfolio for lasting income, UPS stands as a notable candidate worth more study.

You can inspect the full "Best Dividend Stocks" screen and see other passing companies here.

For a complete summary of all basic factors behind the ratings discussed, you can inspect the full ChartMill Fundamental Analysis report for UPS here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation to buy or sell any security, or an endorsement of any investment strategy. All investments involve risk, including the potential loss of principal. The financial data and ratings referenced are based on past performance and analyst estimates, which are not guarantees of future results. Investors should conduct their own thorough research and consider their individual financial circumstances and risk tolerance before making any investment decisions.