The Fed held rates steady and basically told markets, “We’ll wait for the data.” Meanwhile, Big Tech kicked off earnings season by proving one thing: AI demand is real, but the bill is enormous and investors are getting pickier about who’s converting capex into growth.

Indexes barely budged, yet the storylines were loud, Fed policy on one side, and an AI infrastructure spending contest on the other.

The Close: Quiet Indexes, Noisy Drivers

Stocks finished essentially flat after the Fed decision, with the Dow up a hair and the S&P 500 down a hair. The Dow Jones Industrial Average rose 0.02% to 49,015.60, while the S&P 500 slipped 0.01% to 6,978.03.

The Nasdaq ended up about 0.3%, and the S&P briefly touched 7,000 intraday, one of those “new milestone” moments that feels exciting until you remember it mostly reflects mega-cap gravity.

The Macro Pulse: A Defensive Pause From the Fed

The Federal Reserve held its benchmark rate steady at 3.50%–3.75% in a 10–2 decision.

Jerome Powell’s tone was noticeably “defensively patient”: the economy is still holding up, the job market looks more stable, but inflation remains too high for comfort. He also flagged tariffs as a key inflation driver and suggested we should know by mid-year whether that impulse fades the way the Fed hopes.

One detail I’m not brushing off: Powell pointed to reduced labor-force growth tied to tighter immigration flows, which makes the labor market harder to read in real time. That’s the kind of structural wrinkle that can keep policymakers cautious even when the headline numbers look fine.

On the “markets as mood ring” front, gold and silver are still acting like investors are quietly hedging against policy surprises (and maybe a bit of geopolitical chaos): gold pushed above $5,300/oz intraday and silver spiked hard as well.

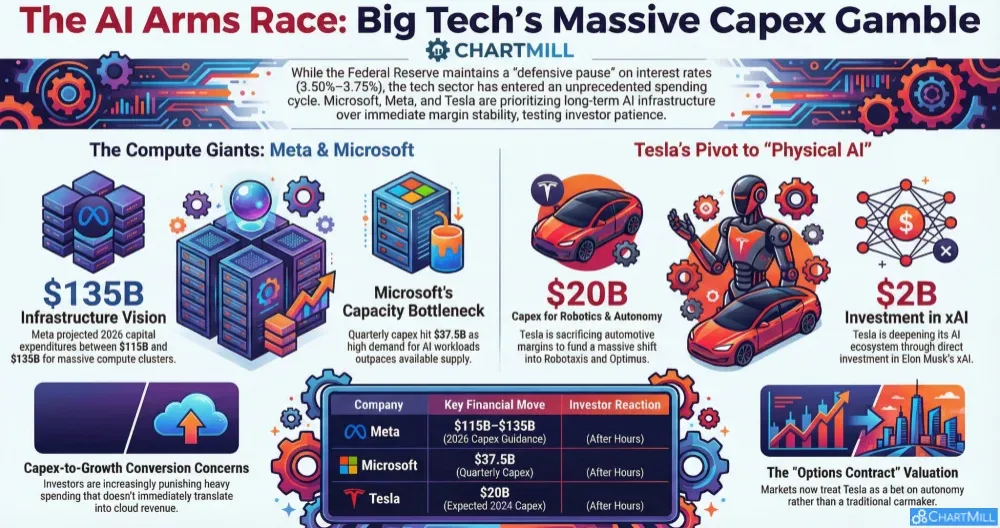

The AI Capex Arms Race: Investors Want Proof, Not Poetry

This earnings cycle is starting with a simple test: who’s spending big on AI and showing credible payback?

Meta: Ads are paying the AI bills

Meta Platforms (META | After Hours +6.64%) beat expectations on revenue and EPS, and - crucially - guided Q1 revenue above what the Street expected.

But the real headline is spending: Meta is now talking $115B–$135B in 2026 capex, essentially asking investors to trust that better AI tooling improves ad performance enough to justify building an industrial-scale compute empire, without the obvious enterprise cloud monetization lever that Microsoft has.

Microsoft: Great quarter, awkward after-hours

Microsoft (MSFT | After Hours -6.14%) delivered a clean beat on revenue and profit, with Azure growth still strong, but the market response turned sour because investors are increasingly sensitive to the “capex-to-growth conversion rate.”

Microsoft is spending like the AI future is arriving tomorrow morning - capex hit $37.5B for the quarter - and management has been explicit that capacity constraints and internal AI workloads are competing with Azure expansion.

Here’s the part I can’t ignore: when a company tells you demand is there but supply/capacity is the bottleneck, the question becomes how fast the bottleneck clears, and how much margin gets sacrificed while it does.

Tesla: The Car Business Is Funding the Robot Dream

Tesla (TSLA | After Hours +3.00%) delivered a quarter that looks like a car company report, until you read it like an AI company trying to disguise its capex appetite.

On the numbers, the message was mixed but coherent: profit fell sharply, with GAAP EPS at $0.24 and adjusted EPS at $0.50, while revenue dipped 3% to $24.9B. Automotive revenue slid 11%, but the battery/energy side grew 25%, and that split matters because it tells you where the momentum is coming from right now.

Tesla itself pinned the margin pressure on heavier AI-focused R&D spending and a slump in regulatory credit income (down 44% to $417M). That’s not a trivial footnote: it’s basically Tesla admitting the “easy money” tailwind is fading just as it chooses to spend aggressively on autonomy and robotics.

Tesla explicitly leaned into the “physical AI” identity, highlighting its Robotaxi push and Optimus work, and even noted it began removing the safety monitor from its robotaxis in Austin in January.

Reuters also reported Tesla will invest $2B in Elon Musk’s xAI and reiterated that Cybercab production is expected to start.

Capex potentially topping $20B this year.

Investors are treating Tesla less like an automaker with cyclical demand headaches and more like an options contract on autonomy + robotics.

That’s why the market can shrug at weak-ish vehicle dynamics but still get excited by robotaxi breadcrumbs. The risk, of course, is that “AI narrative” is cheap to sell and very expensive to build—and this quarter made it clear Tesla is choosing expensive.

Corporate Cross-Currents: Layoffs, Fiber, and Old-School Industrial Reality

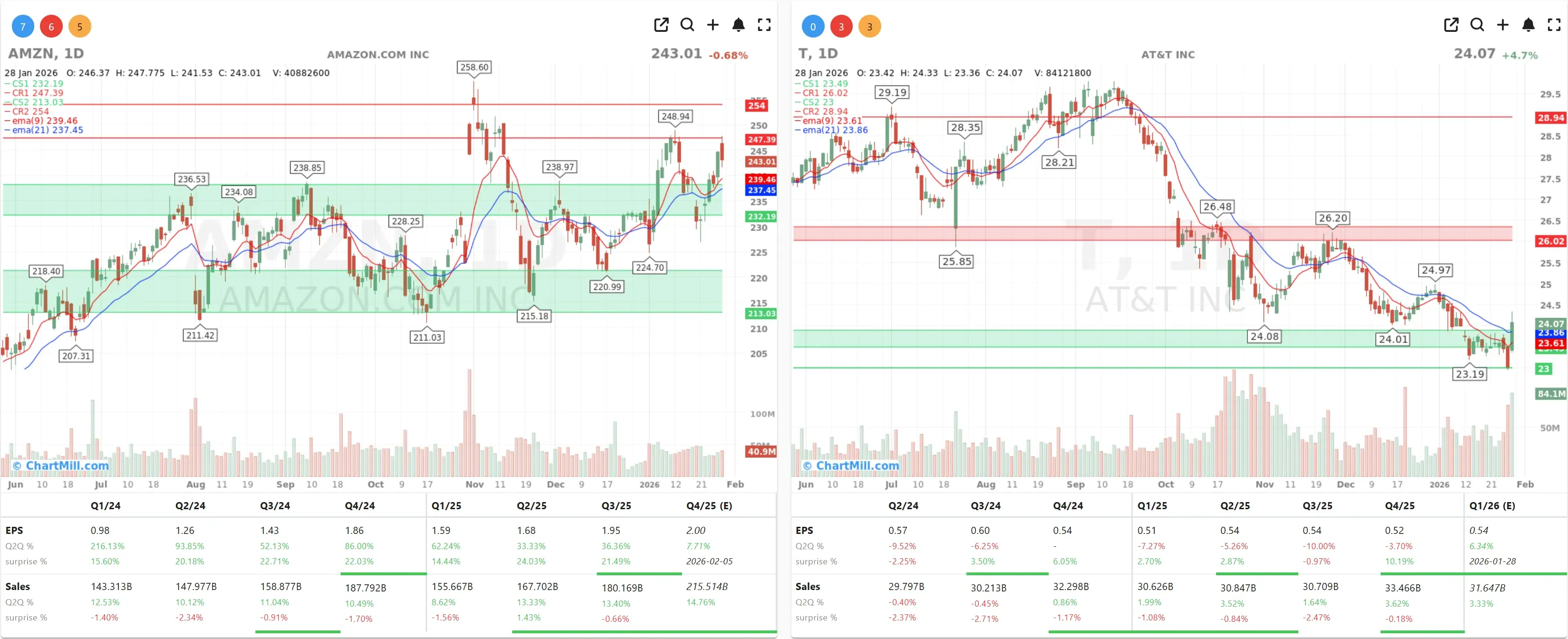

Amazon (AMZN | -0.68%) announced 16,000 more job cuts as it pushes to streamline layers of management and improve efficiency, another reminder that “AI adoption” often shows up first as headcount reduction.

AT&T (T | +4.65%) got a lift after results, with investors focusing on fiber momentum and deal-driven infrastructure expansion—including a move to buy Lumen’s consumer fiber business and a separate spectrum deal with EchoStar.

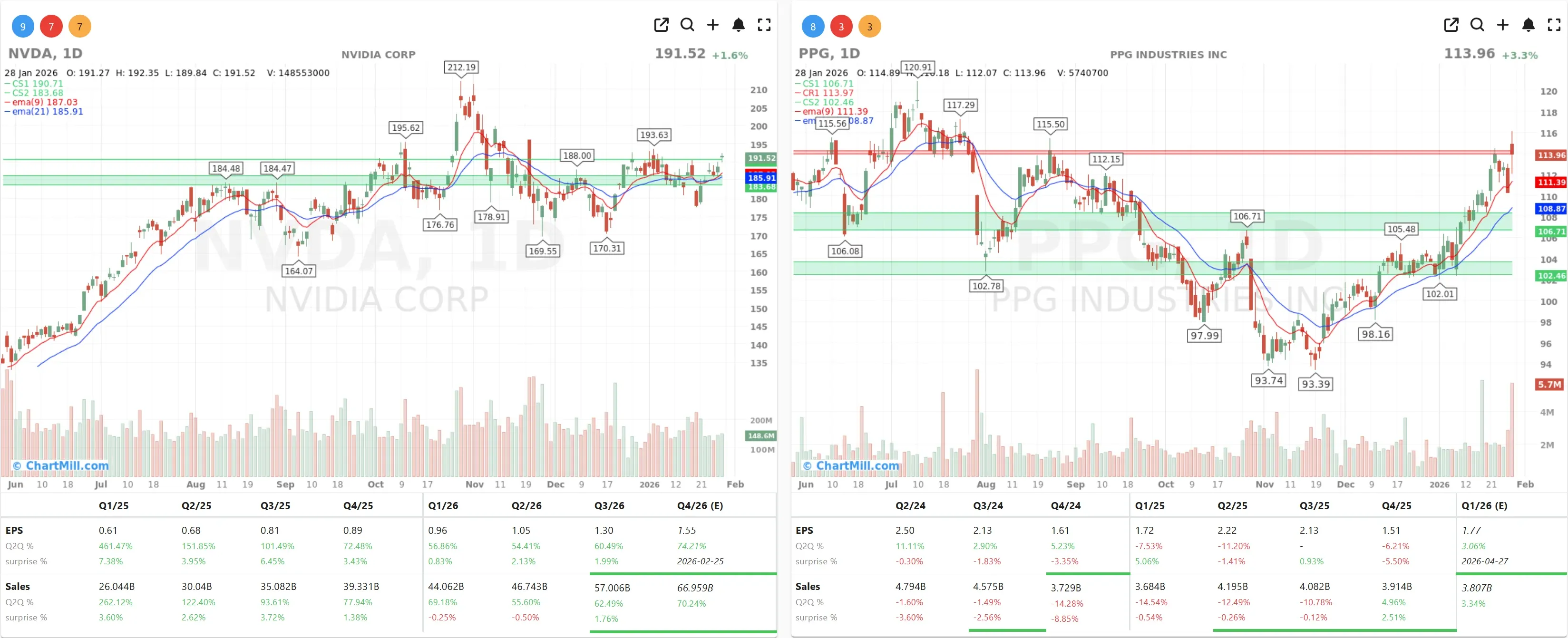

PPG Industries (PPG | +3.34%) managed to beat on revenue, but profits/outlook were more mixed, classic “good numbers, but not the kind you pay a premium for.”

And in the background, Nvidia (NVDA | +1.59%) caught a bid on reports tied to China sales approvals—another small reminder that geopolitics still gets a vote in semiconductor multiples.

What I’m Watching Next

The Fed may be on pause, but the market isn’t. The next few sessions are about whether investors keep rewarding the AI build-out, or start demanding tighter discipline and clearer monetization timelines.

If the tone stays the same, I expect the winners to be the companies that can answer one blunt question without flinching: “How soon does this capex turn into durable cash flow?”

Kristoff - ChartMill

Next to read: Breadth Takes a Breather While Large Caps Hold the Line