The investment philosophy of legendary fund manager Peter Lynch focuses on finding well-run, expanding companies available at sensible prices—a strategy often called Growth at a Reasonable Price (GARP). Lynch supported a long-term, buy-and-hold method, concentrating on firms with durable earnings expansion, sound financial condition, and prices that do not overvalue future potential. His system uses particular quantitative filters to sort for these traits, offering a beginning for more detailed fundamental analysis.

PulteGroup, Inc. (NYSE:PHM) recently appeared from such a filter. As one of the country's biggest homebuilders, the company works under a collection of brands like Pulte Homes, Centex, and Del Webb, serving different customer groups throughout the United States.

Fit with Lynch's Main Standards

The Peter Lynch filter uses a few important rules to find candidates. An examination of PulteGroup's financial numbers shows a good fit with these rules.

- Durable Earnings Expansion: Lynch looked for companies with steady, but not extreme, expansion. The filter demands a 5-year average yearly EPS growth between 15% and 30%. PulteGroup's EPS has expanded at an average yearly rate of 18.05% over this time, fitting within Lynch's desired range. This shows a record of increasing profitability without the unstable rapid expansion he warned about.

- Sensible Price (PEG Ratio): A central part of Lynch's system is the Price/Earnings to Growth (PEG) ratio, which tries to find stocks where the price is fair relative to the expansion rate. A PEG ratio at or under 1.0 is seen as appealing. PulteGroup's PEG ratio, calculated from its past five-year expansion, is 0.70. This implies the stock could be priced low compared to its historical earnings expansion path.

- Sound Financial Condition: Lynch stressed investing in companies with firm balance sheets to endure economic shifts. Two crucial filters are:

- Debt/Equity Ratio < 0.6: PulteGroup reports a very low Debt/Equity ratio of 0.17, well under the filter's limit and even below the tighter 0.25 ratio Lynch himself liked. This shows little dependence on debt financing.

- Current Ratio >= 1.0: The company's solid Current Ratio of 6.82 shows more than enough short-term cash availability, greatly surpassing the requirement and indicating a firm ability to meet near-term responsibilities.

- High Profitability (Return on Equity): To confirm efficient use of shareholder money, the filter requires a Return on Equity (ROE) above 15%. PulteGroup's ROE of 17.09% meets this standard, reflecting management's skill in creating profits from equity.

Fundamental Condition Review

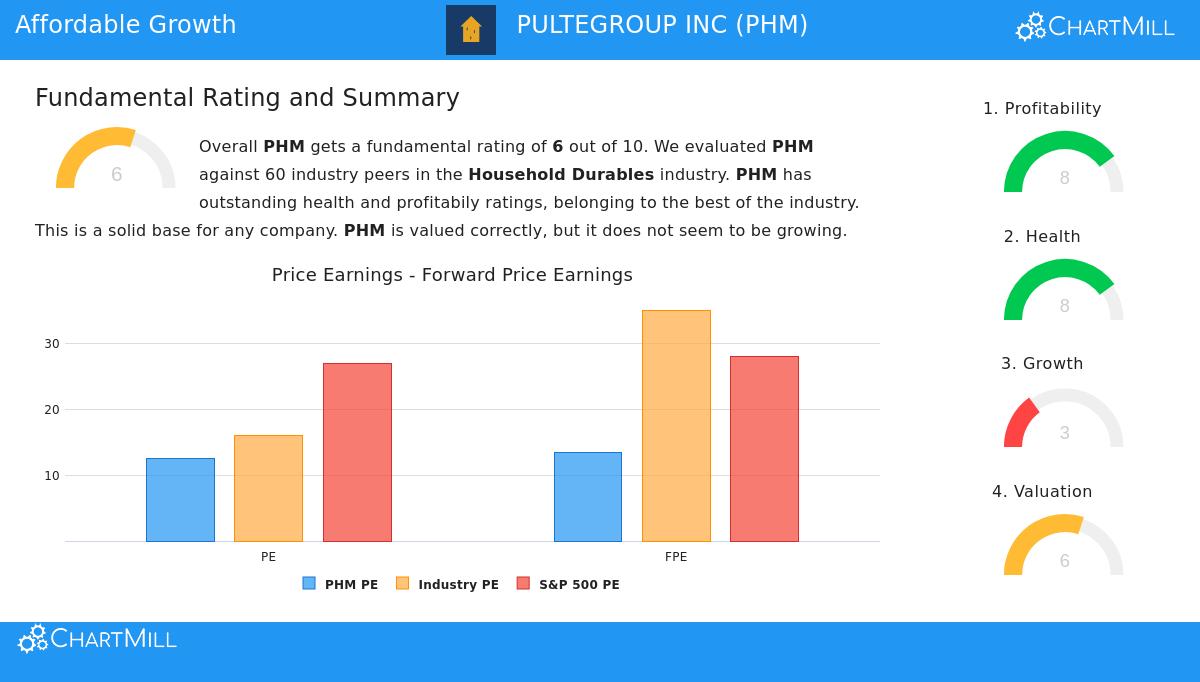

A wider view of PulteGroup's fundamental profile, as covered in its detailed analysis report, supports the image shown by the Lynch filter. The company receives an overall fundamental score of 6 out of 10, with specific high points in profitability and financial condition.

- Profitability & Efficiency: The company scores an 8 out of 10 for profitability. Important margins, like Operating Margin (17.27%) and Profit Margin (12.82%), are in the best group of the household durables industry. Its Return on Invested Capital (ROIC) of 14.00% also does better than most peers, indicating efficient capital use.

- Outstanding Financial Condition: With a score of 8 out of 10, the balance sheet is a definite positive. The very good Altman-Z score (6.29) and small debt levels highlight very low bankruptcy danger. The firm cash position, shown by the high Current Ratio, gives important operational room to maneuver.

- Price Context: The price score is a neutral 6. With a P/E ratio of 12.59, the stock sells at a lower price than both the wider S&P 500 and its industry average. This sensible price, when paired with the firm profitability numbers, fits the GARP investment idea.

- Expansion Points: The main area to note is expansion, which scores a 3. While the company has a firm record of multi-year expansion, recent quarters have shown a deceleration, with earnings and revenue falling year-over-year. This is a key point for investors to watch, as the Lynch system relies on the company's capacity to return to its durable expansion path over the long term.

A Candidate for More Study

For investors who agree with Peter Lynch's philosophy of locating expanding companies at reasonable prices, PulteGroup offers an interesting case for more detailed examination. It meets the quantitative checks of a Lynch-inspired filter, having a history of firm earnings expansion, a clean balance sheet, high profitability, and an appealing price as measured by the PEG ratio. The company's fundamental report verifies central positives in financial condition and operational efficiency.

As with any filter-based find, these numbers are a beginning. The next phase for a long-term investor, as Lynch would suggest, is to completely study the business—learning its competitive place in the housing market, its land buying plan, and its potential for handling interest rate changes—to decide if it meets the definition of a "story" you comprehend and trust for the next ten years.

You can review other companies that currently meet the Peter Lynch filter rules here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. The analysis is based on data and a defined investment strategy filter; it is not a substitute for independent research. Investors should conduct their own due diligence and consider their individual financial circumstances before making any investment decisions.