For investors aiming to create a portfolio centered on steady income, a methodical screening process is necessary. One useful method involves selecting for companies that provide an appealing dividend now and also have the fundamental financial soundness to maintain and raise those payments in the future. This method emphasizes quality, searching for stocks with a high total dividend rating—a combined score assessing yield, growth, history, and payout safety—while also demanding a minimum level of acceptable profitability and financial soundness. This confirms the dividend is not temporary but is supported by a solid and well-run company.

ILLINOIS TOOL WORKS (NYSE:ITW) appears as a result from this type of screen, deserving further examination by dividend-oriented investors. The company's varied activities in automotive, food equipment, welding, and construction products form a steady industrial base. An inspection of its fundamental report shows why it satisfies the strict requirements of a quality dividend method.

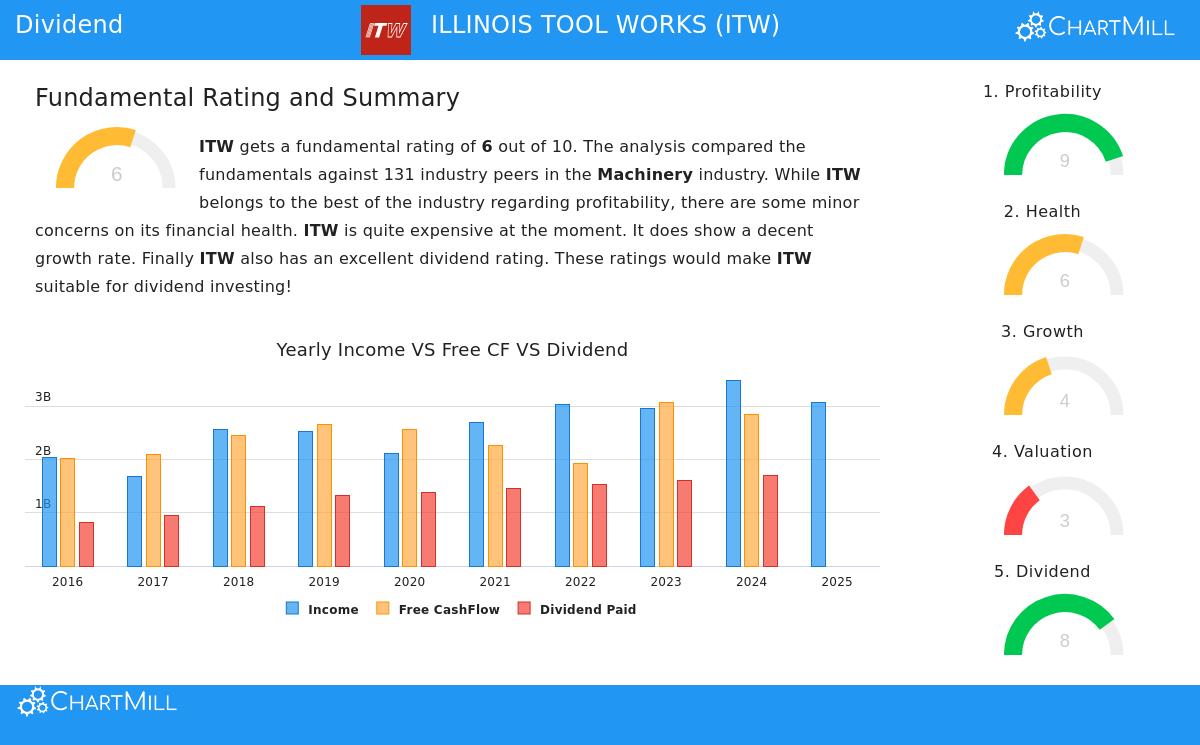

Dividend Dependability and Growth

The heart of any dividend investment case rests on the payment's dependability and possibility for growth. ITW’s dividend characteristics display multiple positive attributes that match a long-term income method.

- History: ITW has distributed a dividend for at least ten straight years and has not cut it in that time. This proven record is a vital sign of management’s dedication to giving capital back to shareholders.

- Steady Growth: The dividend has increased at a yearly rate of about 7% over the last five years. This persistent growth aids income investors in offsetting inflation and raising their cash flow over time.

- Maintainable Payout: The company’s payout ratio is near 58% of its earnings. Although somewhat elevated, this is usually seen as workable, particularly when considered with other factors. The report states that ITW’s earnings are rising quicker than its dividend, which helps the feasibility of future raises.

- Attractive Yield: With a yield of 2.22%, ITW gives a higher return than both the industry norm (1.15%) and the wider S&P 500 (about 1.80%). For investors filtering for income, this delivers a real cash return that is greater than many other options.

This mix—a lengthy, uninterrupted payment history, steady growth, a workable payout, and an attractive yield—is exactly what filters for a high "Dividend Rating" seek to find. It indicates a company that treats shareholder returns as a central part of its financial plan.

Supporting Profitability

A good dividend is only as reliable as the earnings that pay for it. ITW’s excellent profitability measurements supply the needed foundation for its dividend plan. The company receives a top-level Profitability Rating of 9, which is a fundamental part of the screening method. Important points consist of:

- High Returns: ITW produces a Return on Invested Capital (ROIC) of 24.43%, greatly exceeding over 97% of its machinery industry competitors. A high ROIC shows efficient use of capital to create earnings, which is the final origin of dividend payments.

- Strong Margins: The company keeps notable margins, with an operating margin of 26.2% and a profit margin of 19.05%, putting it in the top group of its industry. These good margins offer a buffer against economic slowdowns and guarantee sufficient cash is present for dividends and reinvestment.

This profitability is essential for a maintainable dividend method. A company with poor or unsteady earnings cannot dependably uphold a growing dividend, regardless of how appealing the present yield might seem.

Financial Soundness Factors

The screening process also calls for a minimum level of financial soundness (a rating of at least 5), which ITW fulfills with a score of 6. This aspect shows a varied but workable situation. On the good side, the company has a very strong Altman-Z score of 8.5, showing low short-term bankruptcy danger, and an acceptable debt-to-free-cash-flow ratio. Still, investors should be aware of the high Debt-to-Equity ratio, which points to a notable use of debt financing. While this is typical in industries that require large capital investment and is currently well-covered by strong cash flows, it is an element to watch over time, as high debt can reduce financial options during weak periods.

Valuation and Growth Perspective

From a strict valuation view, ITW does not seem inexpensive, trading at a P/E ratio similar to the market and its industry. Its growth outlook is moderate, with anticipated earnings growth in the low double-digits. This supports the notion that the investment argument here is not mainly about high capital gains, but instead about owning a high-quality, profitable industrial business that dependably distributes its results to shareholders through a growing dividend.

For investors using a methodical dividend screening method, ILLINOIS TOOL WORKS offers a strong profile. It joins a respectable and growing yield with a very strong profitability profile, all supported by a long history of shareholder returns. While its valuation is not low and its use of debt is significant, its central operational strength backs the case for a lasting income stream.

You can examine the complete fundamental analysis that formed this review here.

This review of ITW came from a systematic filter for quality dividend payers. If you want to see other companies that meet similar filters for high dividend ratings, good profitability, and acceptable financial soundness, you can see the full filter results using this link: Best Dividend Stocks Screen.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer or solicitation to purchase or sell any securities. The information shown is based on supplied data and should not be the only foundation for any investment choice. Investors should perform their own separate research and talk with a qualified financial advisor before making any investment decisions. Past results do not guarantee future outcomes.