For investors looking for a dependable source of passive income, a methodical screening process is needed to distinguish reliable dividend payers from possible value traps. One useful technique focuses on companies that provide a good dividend and also show the fundamental financial capacity to maintain and increase those payments. This method favors stocks with high dividend ratings, which assess yield, growth, and stability, while also demanding satisfactory scores for earnings power and financial condition. This multi-step process aids in finding companies where the dividend is backed by an earning business and a firm balance sheet, instead of being a temporary feature of a company in trouble.

ILLINOIS TOOL WORKS (NYSE:ITW) appears as a candidate from this type of screening process, deserving further examination by dividend-oriented investors. The company, a varied manufacturer of industrial products and equipment in seven areas such as Automotive OEM, Food Equipment, and Welding, shows a profile that matches the central principles of sustainable dividend investing.

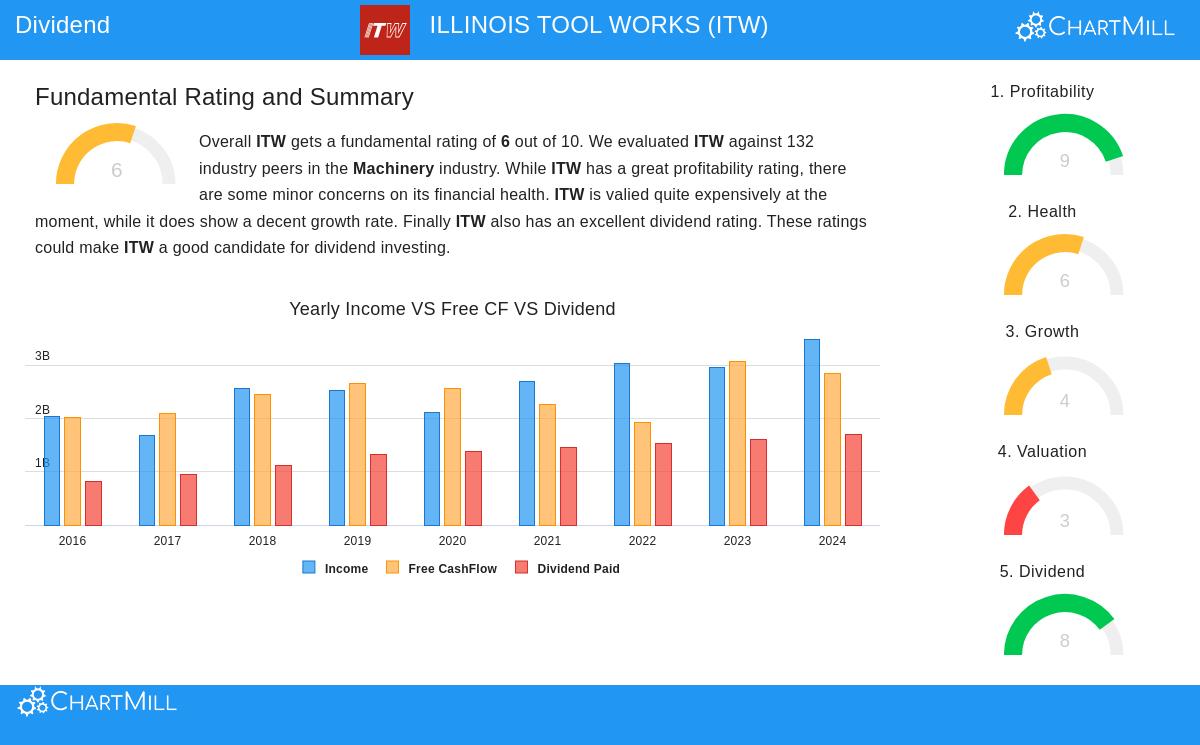

A Firm Dividend Profile

The foundation of ITW's attraction for income investors is its long-standing dividend, which receives a high rating due to a number of important elements:

- Dependable History and Growth: ITW has a history of paying dividends for at least ten years without a decrease. Furthermore, it has regularly increased its payout, with a yearly dividend growth rate near 7% over the last five years. This shows a management dedication to giving capital back to shareholders.

- Good and Maintainable Yield: The stock's present dividend yield of 2.46% is viewed as good. It exceeds the average yield of similar companies in its field and is also above the current S&P 500 average. While the payout ratio—the part of earnings given as dividends—is at a somewhat high 58%, review shows that the company's earnings are increasing quicker than its dividend. This relationship is important, as it implies the present payout level is maintainable and has potential for more growth, rather than being in danger of a reduction.

Backed by Notable Profitability

A high dividend is only as sound as the business financing it. This is where ITW's financial capacity becomes vital, as a profitable company creates the cash needed to maintain shareholder returns. ITW's profitability measures are excellent:

- High Returns: The company produces very good returns on its assets and invested capital, doing much better than most of its rivals in the machinery industry. A high Return on Invested Capital (ROIC) shows efficient use of capital to create earnings.

- Strong Margins: ITW keeps notable profit and operating margins that are near the best in its sector. These good margins have displayed positive growth in recent years, giving a cushion against economic slowdowns and strengthening the company's capability to finance its activities and its dividend.

Reviewing Financial Condition and Price

While the screening rules called for "satisfactory" condition, a more detailed view shows a varied situation. ITW's financial condition rating is acceptable, supported by a very firm Altman-Z score showing low bankruptcy risk and an acceptable debt-to-free-cash-flow ratio. However, investors should be aware of a comparatively high debt-to-equity ratio, which indicates a substantial use of debt financing. This is offset by the company's firm and steady cash production, but it stays a factor for thought.

On price, the stock seems fully valued, trading at a high level based on standard price-to-earnings measures. This is a typical trait of good, dividend-increasing industrial companies, and the high price can be partly explained by the company's very good profitability. For dividend investors concentrated on long-term income growth instead of low price, this may be an acceptable exchange for the quality available.

Conclusion

For investors using a screen for high-grade dividend payers, Illinois Tool Works offers a strong case. It fulfills the main goals by providing a dependable, increasing dividend backed by a basically profitable and operationally sound business. The company's long record of dividend payments and increases indicates a shareholder-friendly approach. While its price is not low and its balance sheet holds considerable debt, its high cash flow generation and market standing give assurance in its ability to continue its capital return program.

You can see the detailed fundamental analysis that backs these ratings here.

This review of ITW was obtained from a systematic screening process. For investors wishing to do their own study and find other companies that fit similar standards for dividend sustainability, profitability, and financial condition, you can see the full "Best Dividend Stocks" screen here.

,

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The information presented should not be the sole basis for any investment decision. Investors should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.