For investors looking for a dependable source of passive income, a methodical screening process is needed to distinguish truly lasting dividend payers from those with uncertain, high yields. A typical method focuses on finding companies that have not just a good dividend history but also show fundamental financial soundness and steady earnings. This method tries to find businesses able to keep and raise their payments through different economic conditions, instead of those only providing a high yield that could be unstable. Using tools like the ChartMill Dividend Rating with other ratings for earnings and financial soundness can effectively highlight these opportunities.

One stock that appears from this kind of filter is ILLINOIS TOOL WORKS (NYSE:ITW), a diversified maker of industrial goods and equipment. The company’s fundamental report shows a profile that matches the main ideas of careful dividend investing, combining an appealing income payment with a solid operational base.

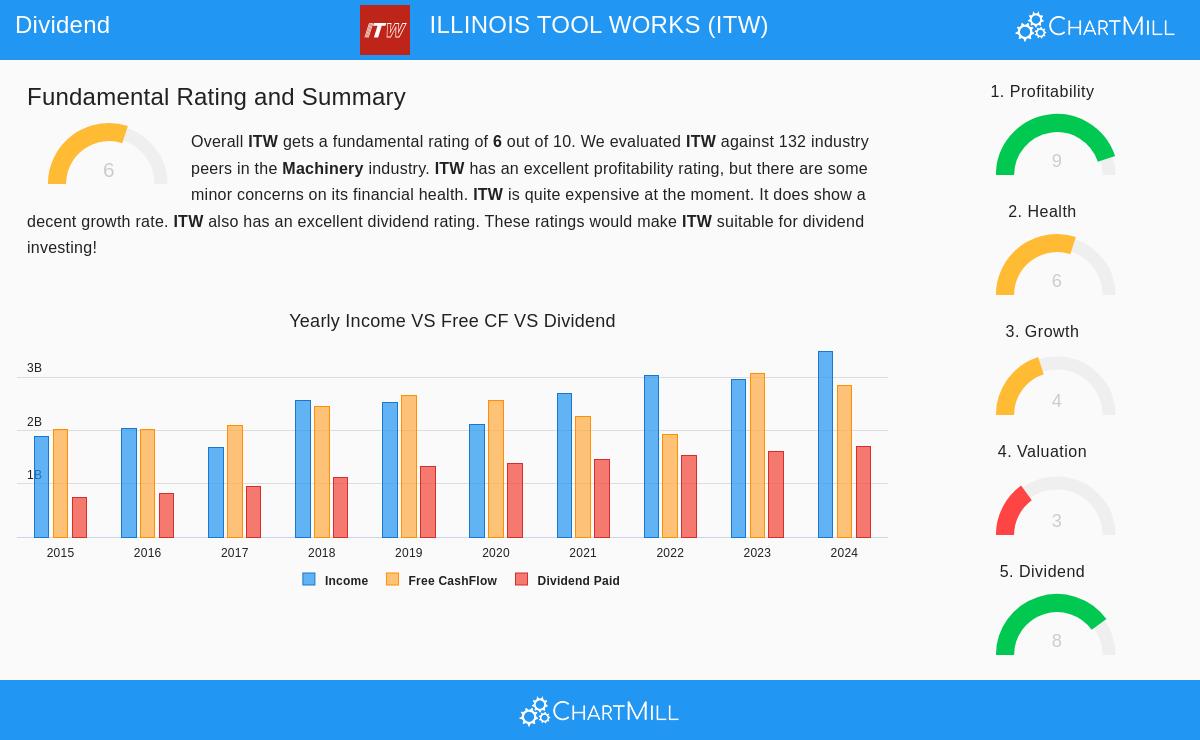

A High-Quality Dividend Profile

The main attraction of ITW for income-oriented investors is its long-running and increasing dividend. The company gets a good ChartMill Dividend Rating of 8 out of 10, showing high marks across several important measures dividend investors value.

- Dependable History and Increase: ITW has a history of dependability, having paid and raised its dividend for at least ten straight years. This steadiness is a key trait of dividend aristocrats and points to a management team dedicated to giving capital back to shareholders. Also, the dividend is increasing at a good yearly rate of about 7% over the last five years.

- Appealing and Maintainable Yield: The stock provides a current dividend yield of 2.56%, which is higher than the industry average and good compared to the wider S&P 500. More critically, the maintainability of this payment is backed by the company's profits. While the payout ratio is 58%, which is somewhat high, the report states that profits are increasing quicker than the dividend, meaning the increase is maintainable. A history of good positive cash flows further supports the company's capacity to finance these payments.

The Base: Earnings and Financial Soundness

A high dividend rating by itself is not enough; it needs to be supported by a stable base. This is where filtering for satisfactory earnings and soundness ratings is important, as they show the company's capacity to produce the profits required to maintain the dividend over time. ITW gets very high marks on earnings with a rating of 9.

- Outstanding Earnings Measures: The company's margins are a notable feature. Its operating margin of 26.2% and profit margin of 19.05% are in the top group of its industrial machinery peers. Even more notable are its returns on capital, with a Return on Invested Capital (ROIC) of 24.44% being much higher than its cost of capital. This shows ITW is very effective at using its resources to create profits, which is the fundamental source of dependable dividend payments.

- Satisfactory Financial Soundness with a Point to Watch: ITW receives a satisfactory Soundness rating of 6. The company shows good overall solvency, with an Altman-Z score that points to a very small chance of bankruptcy and an acceptable debt-to-free-cash-flow ratio. Still, investors should be aware of the higher Debt-to-Equity ratio of 2.80, which shows a greater use of debt financing than many industry peers. While currently workable given the good cash flow, this is a factor for continued observation, as high debt can strain financial options during weak periods.

Price and Expansion Factors

From a pure price perspective, ITW seems fully valued. Its Price-to-Earnings ratio is similar to both the S&P 500 and its industry, but the report describes it as "rather expensive." The high PEG ratio indicates the current price may not be completely supported by its expansion path alone. However, for a dividend investor, part of that higher price may be for the outstanding earnings and dependable income payment.

On expansion, the situation is varied but getting better. Recent sales expansion has been slow, but the company is predicted to see modest expansion in both sales and earnings per share in the next few years. Importantly, the expansion rate for EPS is forecast to rise, which is a good signal for future dividend raises.

Conclusion

ILLINOIS TOOL WORKS makes a strong case for dividend investors who value quality and dependability over seeking the absolute highest yield. The stock does very well in the areas a solid screening method aims for: a high and increasing dividend backed by top-tier earnings and satisfactory financial soundness. The strong ROIC and margins give assurance that the business can continue to finance its shareholder returns. While the price is not low and the debt level is above normal, the overall combination of reliable income, excellent operational performance, and a long record of dividend growth makes ITW a stock worth further study for a varied dividend portfolio.

For investors wanting to examine other companies that fit similar standards of good dividends, earnings, and financial soundness, you can see the complete list of outcomes from the "Best Dividend Stocks" screen here.

,

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The information presented is based on data provided and should not be the sole basis for any investment decision. Investors should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.