Just when it seemed markets had found their footing, a 4% spike in crude oil reminded everyone that inflation is far from a solved problem. Thursday's session felt like a gut-check for investors who'd grown comfortable pricing in a Fed pivot and the market's reaction was swift and unforgiving.

Macro: Oil, Rates & a Vanishing Rate-Cut Runway

The trigger was the Iran crisis, which drove oil sharply higher for the second consecutive session. That may sound like a geopolitical footnote, but its downstream effect on rate expectations is anything but.

The policy-sensitive 2-year Treasury yield surged on its way to its largest four-day climb since October 2024, a move that rattled equity markets more broadly.

What's particularly sobering here is the speed at which rate-cut expectations have been repriced. Investors were pricing in roughly 60 basis points of cuts for all of 2026 just last week. By Thursday, that number had dropped to fewer than 40 basis points.

For a market that has been leaning on the promise of easier monetary conditions, that's a meaningful shift and one that deserves close attention in the days ahead.

The Dow Jones Industrial Average DJIA | -1.6% plunged over 1,100 points at its intraday low before recovering somewhat, ultimately closing 785 points lower. The Nasdaq COMP | -0.3% fared better, trimming a 1.2% loss to just 0.3%, helped in part by a handful of resilient tech names.

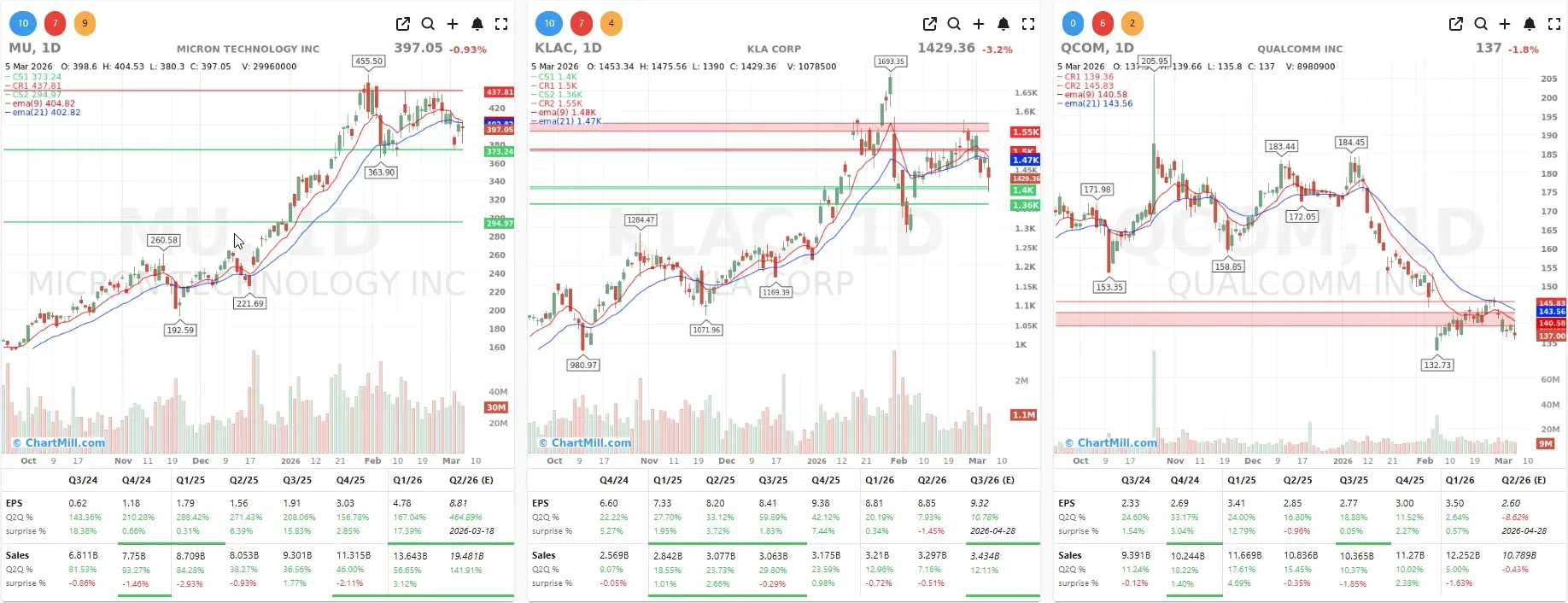

Semiconductors: A Mixed Picture Dominated by AI

The chip sector was on the defensive Thursday after Bloomberg reported the US government is mulling mandatory export licenses for AI semiconductors sold globally.

That's a significant potential headwind for companies that generate meaningful revenue from international AI hardware sales. KLA KLAC | -3.15%, Micron Technology MU | -0.93%, and Qualcomm QCOM | -1.8% all felt the pressure.

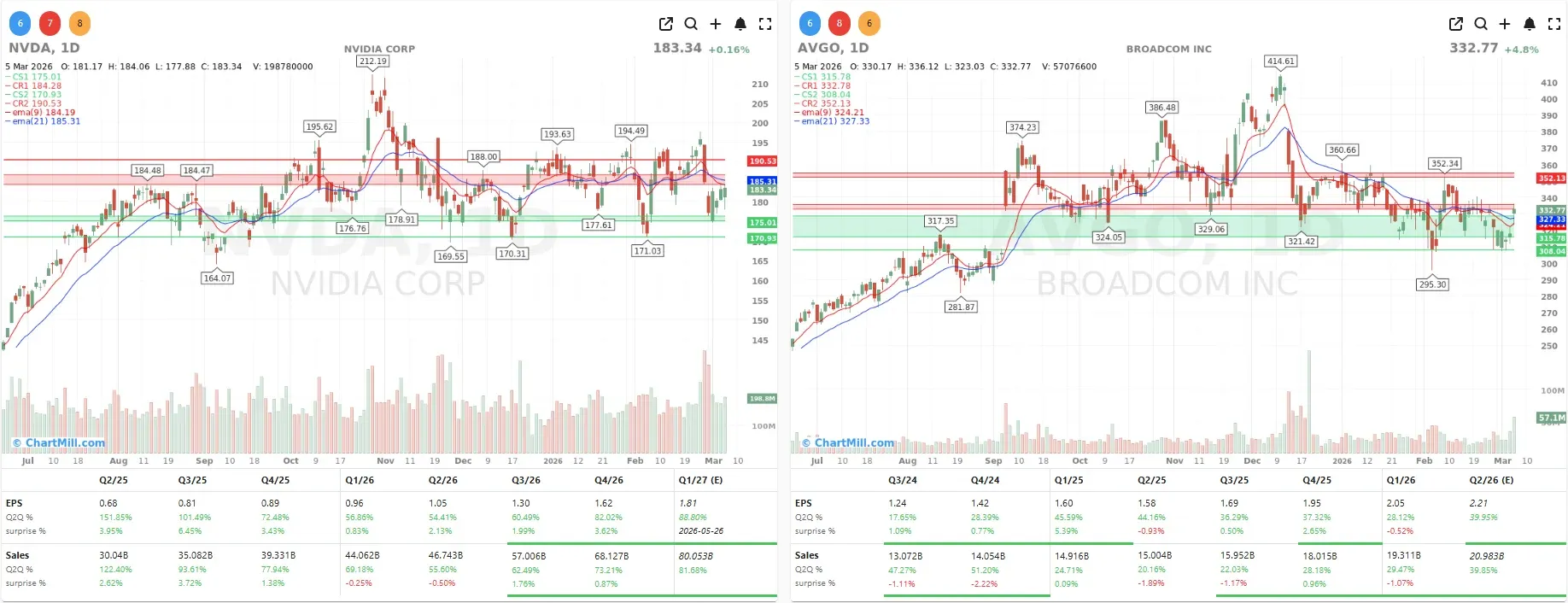

Nvidia NVDA | + 0.16% slight was an exception, bolstered by reports that companies are cutting headcount specifically because AI automation is enabling them to do more with less. There's something almost poetic about Nvidia catching a bid from news of AI-driven layoffs.

The real standout of the day, though, was Broadcom AVGO | +4.8%. The company's projection of $100 billion in annual AI revenue by 2027 is a staggering number, and Wall Street took notice. Multiple analysts raised their price targets:

- Baird lifted its target from $420 to $630 (Buy), calling the AI revenue forecast "solidly above consensus."

- Evercore bumped its target from $490 to $582 (Buy), highlighting growing visibility from Google's demand for TPU chips and accelerating orders from Anthropic and Meta Platforms META.

- Truist Securities moved from $510 to $545 (Buy), citing "yet another AI demand upgrade."

- Bloomberg Intelligence noted the forecast rests on accelerating ASIC shipments and AI networking products, with margins holding above expectations.

- Vital Knowledge added a note of caution, the AI hardware trends look strong, but software performance remains a weak spot that could raise questions among investors. Fair point, and worth watching.

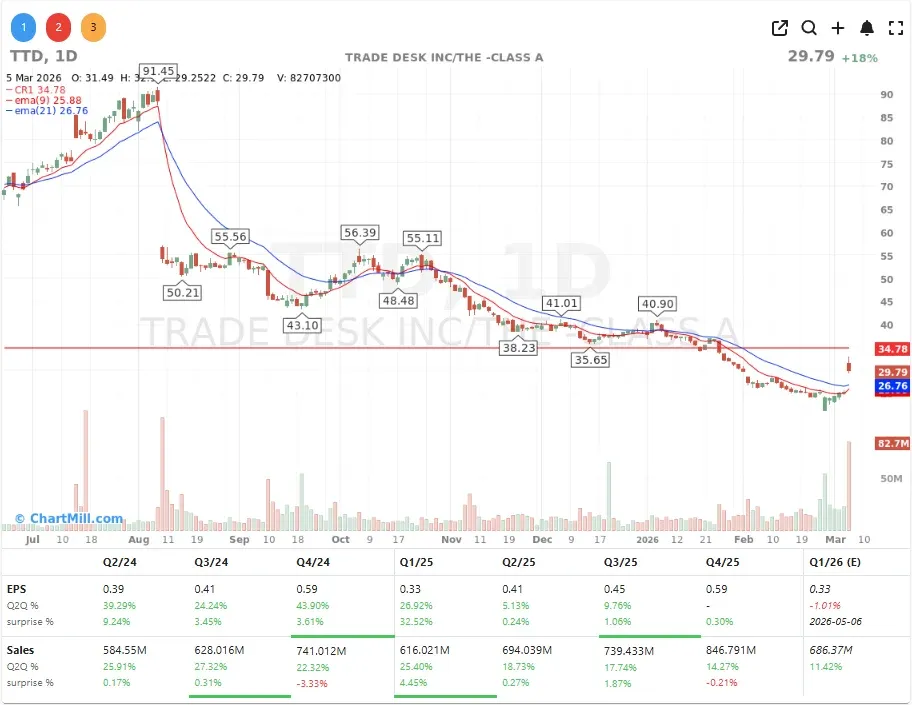

The Trade Desk: OpenAI Rumor Does Heavy Lifting

The session's most dramatic single-stock move belonged to The Trade Desk TTD | +18.36%, which rocketed higher on a report from The Information that OpenAI had approached the company about selling advertising inventory on its AI platforms.

If confirmed, this would signal that OpenAI is willing to partner externally to build out a monetization model rather than going it alone, a meaningful strategic signal for the ad-tech ecosystem.

Adding fuel to the fire: CEO Jeffrey Green didn't just talk the talk. He purchased 6 million shares at prices between $23.49 and $25.08, committing roughly $148 million of personal capital.

Corporate News: Cuts, Beats & Stumbles

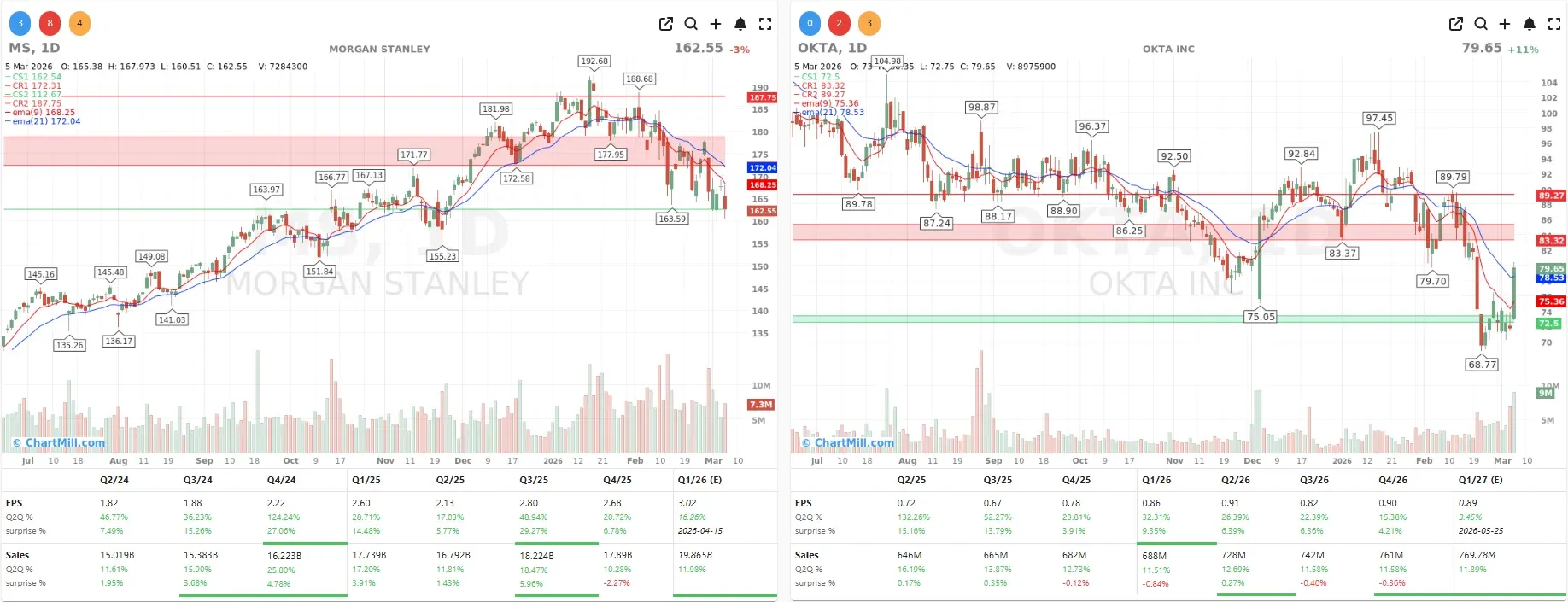

Morgan Stanley MS | -3% is laying off approximately 3% of its workforce, with cuts spanning all three of its main divisions, according to The Wall Street Journal. The broader bank sector had a rough day regardless, with rate uncertainty doing no favors for financial stocks.

Cybersecurity firm Okta OKTA | +11.03% delivered better-than-expected quarterly results, though its forward guidance disappointed. The market reaction was still positive, sometimes beating numbers is enough, even if the outlook underwhelms.

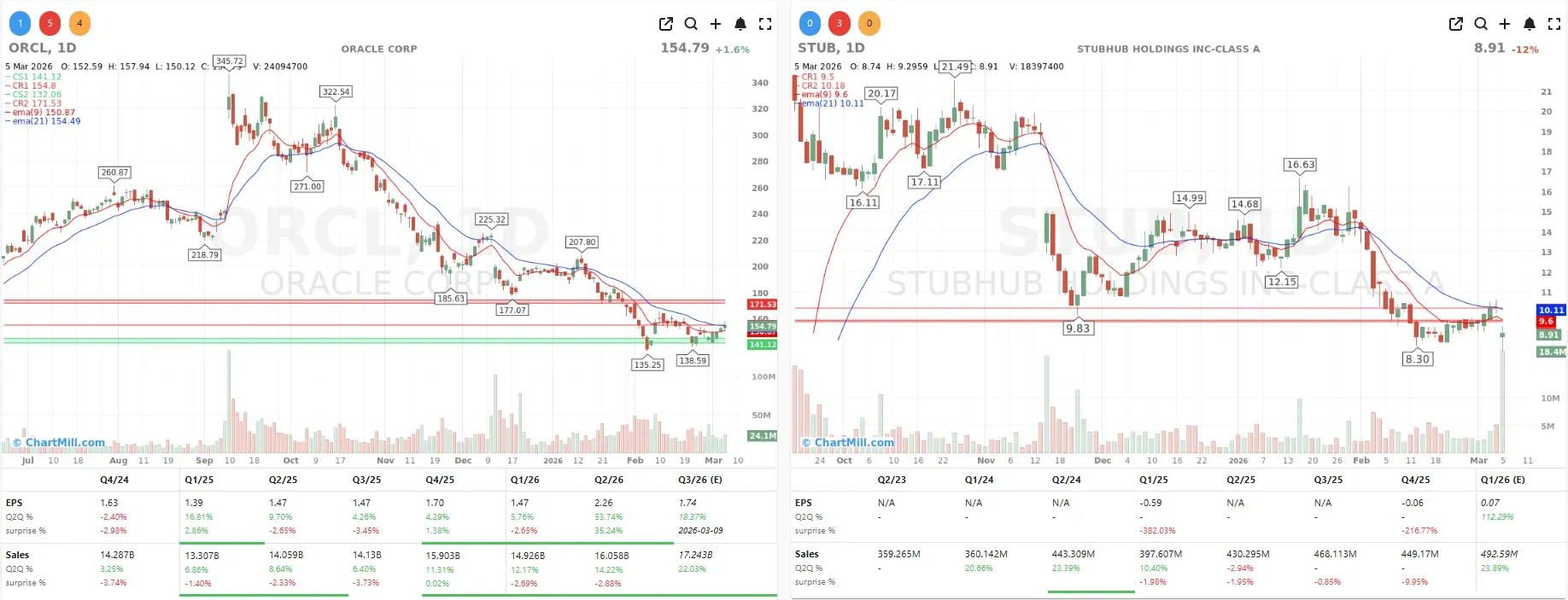

Ticketing platform StubHub STUB | -12.39% had a notably bad session, posting a quarterly loss accompanied by declining revenue. Difficult to spin that story in any positive direction.

Oracle ORCL | +1.59% is reportedly planning thousands of job cuts as it grapples with a liquidity crunch stemming from aggressive AI data center expansion. Bloomberg's sources indicate some of those reductions will target roles Oracle expects AI to replace. Despite the headline, the market responded positively, perhaps reading the restructuring as a necessary cost-rationalization move for long-term competitiveness.

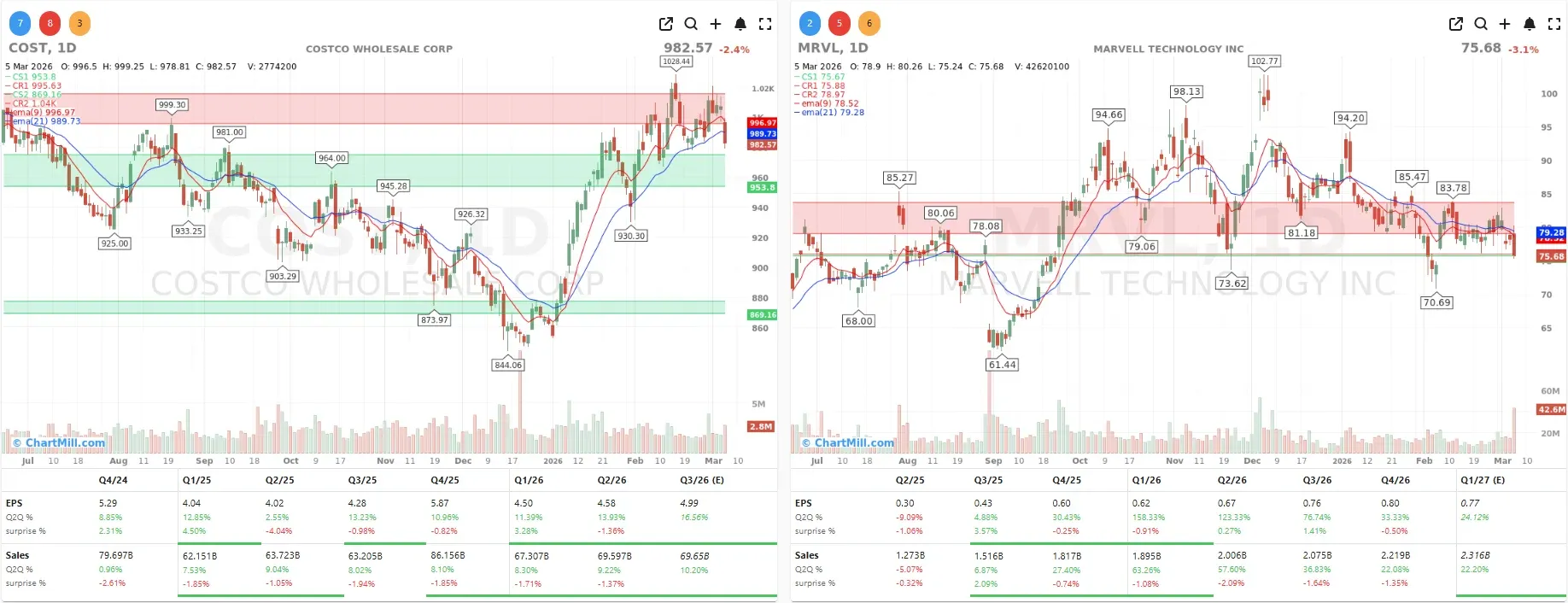

After the Bell: Marvell & Costco Deliver

Two names reported after Thursday's close with results worth noting heading into Friday.

Marvell Technology MRVL | -3.09% posted quarterly revenue and earnings in line with its own guidance, while its forward outlook comfortably exceeded analyst estimates.

CEO Matt Murphy pointed to "robust" AI demand and said revenue growth should accelerate each quarter throughout the current fiscal year, with bookings growing at a record pace.

Costco Wholesale COST | -2.4% reported Q2 net income of $2.04 billion, or $4.58 per share, beating the FactSet consensus of $4.52 per share.

Revenue climbed from $63.7 billion to $69.6 billion year-over-year, slightly ahead of the $69.3 billion forecast. Comparable store sales grew 6.7% versus the 6.3% estimate, and subscription fee revenue hit $1.36 billion against a $1.33 billion expectation.

Clean beat across the board.

My Take

The oil spike and the resulting rate-cut repricing are the kind of developments that should prompt a reassessment of positioning, particularly in rate-sensitive sectors.

Meanwhile, the AI trade continues to bifurcate: hardware names with direct exposure to hyperscaler capex (Broadcom, Marvell) are holding up well, while the broader semiconductor space faces growing regulatory headwinds.

The Trade Desk's 18% surge is intriguing, but I'd want confirmation on the OpenAI partnership before reading too much into it. For now, keep a close eye on oil prices and the 2-year yield, those two data points are driving more of the market's direction than anything else right now.

ChartMill Market Desk

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Breadth Breaks Down Again as the Bounce Fails