Yesterday I noted the S&P 500 was 0.2% away from its January all-time high. Wednesday, that gap closed and the market didn't need a dramatic catalyst to get there. Just a combination of diplomatic progress on Iran, two more strong bank earnings reports, and a tech sector that, quite frankly, has been running out of reasons to sell off.

The Rundown

- The S&P 500 and Nasdaq both closed at new all-time highs, completing a recovery that began the moment ceasefire talks between the US and Iran first showed traction

- Growing optimism around a peace deal, with Trump calling the conflict "very close to over", continued to draw money back into risk assets and helped stabilize oil prices near recent lows

- Bank of America and Morgan Stanley both delivered strong Q1 results, extending a pattern of financial sector strength that has been one of the more reliable stories of earnings season

- A wave of high-profile corporate announcements - Tesla's AI chip milestone, Uber's autonomous vehicle commitment, Robinhood's regulatory green light - added momentum across multiple sectors

A Record That Feels Earned

The S&P 500 closed at 7,022.95, up 0.8% on the day. The Nasdaq Composite added 1.6% to finish at 24,016.02, marking its 11th consecutive winning session. The Dow Jones Industrial Average slipped a marginal 0.15% to 48,463.72, a small enough divergence that it barely changes the broader read.

What makes this record feel different from past attempts is the breadth of participation. It wasn't just a handful of mega-cap names dragging the indices higher.

Technology led, with Microsoft (MSFT | ▲4.6%), Apple (AAPL | ▲2.9%), Meta Platforms (META | ▲1.4%), and Alphabet (GOOGL | ▲1.26%) all gaining meaningfully. But the financials moved too. So did consumer discretionary. So did, as I'll get into, a string of individual names across sectors that added their own bricks to the day's wall.

The S&P 500 has now fully recovered from the shock that gripped markets when the Iran conflict escalated in late February. That's a faster recovery than most people would have predicted at the peak of the uncertainty. Whether it's warranted is a separate question, one I'll return to at the bottom.

Iran: Trump Says It's "Very Close to Over"

The diplomatic backdrop continues to drive sentiment more than any single earnings print. On Wednesday, Trump told Fox Business that the war with Iran is "almost over."

He hinted in a separate interview with ABC News that a ceasefire extension - the current truce expires next week - may not even be necessary, implying a full deal could come before it runs out. A White House official also told CNBC that discussions about a second round of formal negotiations between Washington and Tehran are actively underway.

Trump has a history of getting ahead of the actual timeline on these things, so I wouldn't mark the calendar just yet. But the direction of travel is consistent: each week that passes without renewed fighting chips away at the war premium that was baked into asset prices starting in February.

The Strait of Hormuz remains largely closed, and about a fifth of global oil supply is still disrupted. That's not resolved. But the market has decided it's pricing in the resolution, not the current reality and short of a sharp reversal in the talks, that calculus is hard to challenge.

Oil itself barely moved on the day. WTI crude edged up 0.01% to $91.29 a barrel. Brent added a tenth of a percent to $94.93. The relative stillness in oil is actually part of the story: these levels represent a significant drop from the $145 peaks in early March, and the stabilization is helping inflation expectations settle.

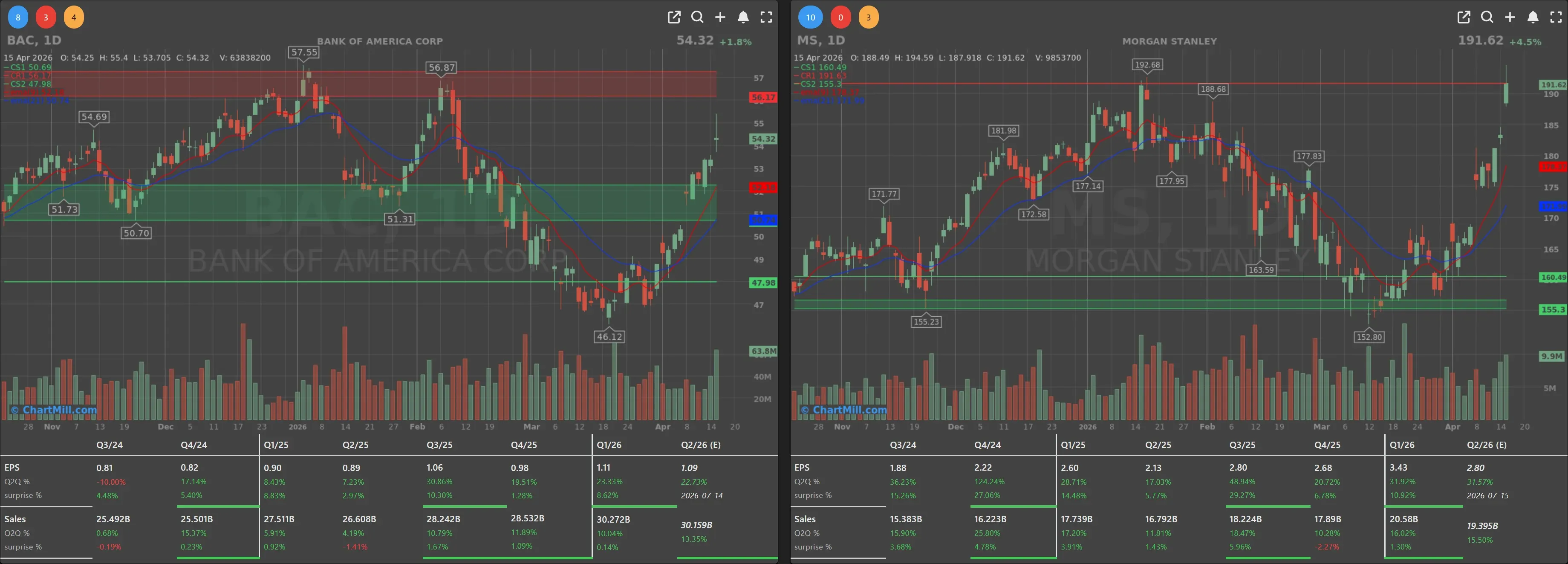

Banks Keep Delivering

Bank of America (BAC | ▲1.82%) and Morgan Stanley (MS | ▲4.52%) both reported Q1 results on Wednesday, and neither disappointed.

Bank of America's net profit rose 17% to $8.6 billion for the quarter.

- Revenue climbed 7% year-on-year to $30.3 billion, with earnings per share up 25% to $1.11.

- The wealth management division pulled in $20 billion in fresh client assets.

Solid across the board, with the investment banking and trading revenue lines doing the heavy lifting, same story we've been hearing across the major banks this season.

Morgan Stanley put up an even stronger set of numbers.

- Profit jumped 29% to $5.57 billion ($3.43 per share), while revenue rose 16% to $20.58 billion.

- Trading was a standout. So was investment banking.

The stock's 4.5% gain reflected the quality of the beat, it was a genuine outperformance across most divisions.

Together with JPMorgan's record $16.49 billion quarterly net income reported on Tuesday, and Citigroup's cleaner-than-expected results, the picture that's emerging from bank earnings season is one of a financial sector that is genuinely performing well, expanding margins while market volatility and the Iran-driven commodity disruption created trading opportunities that their competitors couldn't capitalize on as efficiently.

The nuance I'd add: these earnings reflect a world where the ceasefire has been holding for several weeks and volatility has provided fee income. A full peace settlement that drains the volatility premium could make Q2 a quieter story.

Tesla's AI5 Moment

Tesla (TSLA | ▲7.62%) extended its winning run to five consecutive sessions on Wednesday, and the fuel this time was a social media post from Elon Musk. He announced on X that Tesla's AI5 chip, the company's most powerful processor to date, also known as Hardware 5, has completed tape-out, meaning the final design has been sent to foundries for fabrication.

A single AI5 chip is benchmarked near Nvidia's Hopper architecture; a dual-chip configuration reportedly approaches Blackwell-level performance but at substantially lower cost and power consumption. The chip is designed to dramatically reduce latency in autonomous driving models, and Tesla says high-volume production is targeted for 2027. Musk also mentioned that AI6 and Dojo3 are progressing in parallel.

Five consecutive up days. A chip reveal that suggests the autonomous driving roadmap is real and moving. And a stock that, for all the turbulence of the past six months, has found a way to reconnect with a thesis that investors clearly still want to believe in.

Five Stories That Shaped the Session

Robinhood (HOOD | ▲10.41%) had a standout day after the SEC granted approval for its customers to borrow money to trade on margin. That's a meaningful regulatory unlock for Robinhood, margin trading is a higher-revenue product that its more established competitors have long offered. The market reacted accordingly.

Uber (UBER | ▲5.99%) rallied after the Financial Times reported the company plans to invest $10 billion in self-driving taxis. The ambition isn't new, but the scale of the commitment is a statement. It's also worth noting that Uber's CTO separately acknowledged the company's AI budget for 2026 has already been exhausted, which gives a sense of how aggressively the company is deploying capital into this race.

Snap (SNAP | ▲7.86%) jumped after the parent company of Snapchat announced it will cut 16% of its workforce and lean further into AI to manage the remaining workload. Cost cuts plus an AI productivity narrative, the kind of story markets are rewarding without much questioning right now.

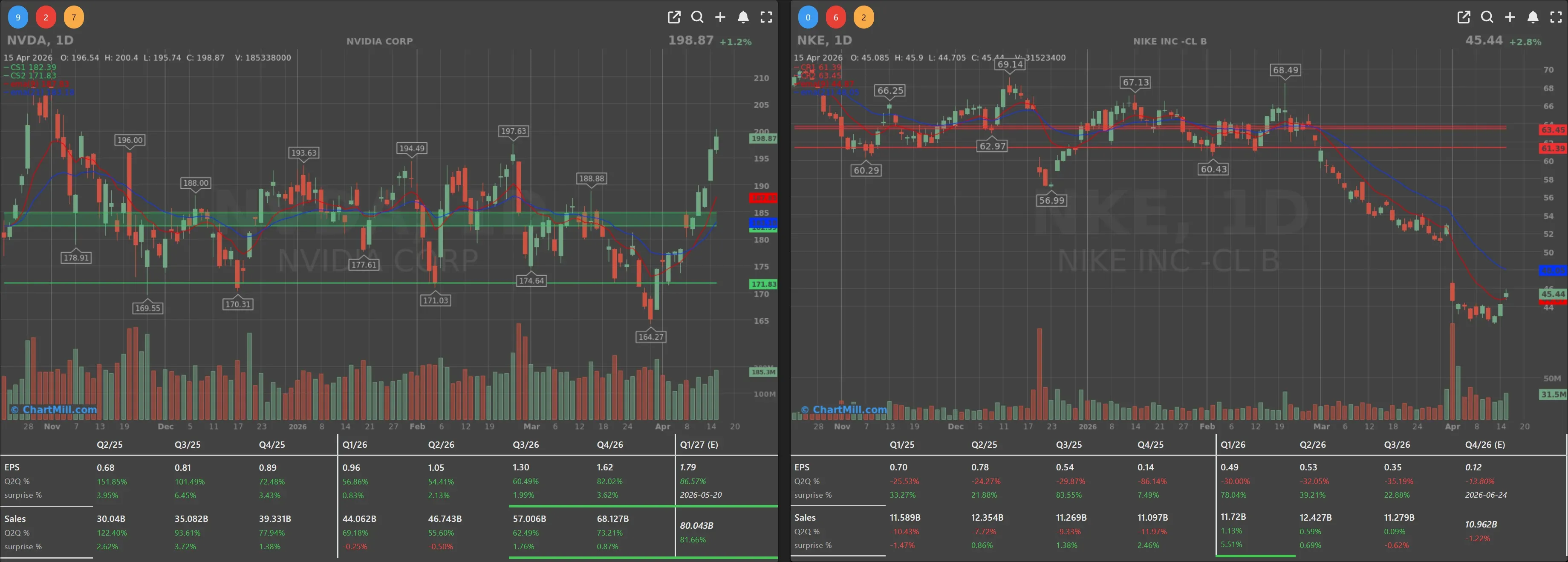

Nike (NKE | ▲2.81%) got a modest but notable lift after it emerged that both Apple CEO Tim Cook and Nike CEO Elliott Hill each purchased approximately $1 million worth of Nike shares recently. Insider buying at that level is a signal worth noting, especially in a stock that's down nearly 31% year-to-date.

It doesn't mean the bottom is in, but it tells you something about what the people closest to the company think about the current valuation.

Nvidia (NVDA | ▲1.20%) extended its own streak to ten consecutive positive sessions. No single catalyst, just a stock that keeps finding buyers.

The Macro Picture, and the One Story Markets Chose to Ignore

Two pieces of macro data came in on Wednesday that told different stories.

- The Empire State Manufacturing Index for New York showed a sharp improvement, swinging from -0.2 in March to +11.0 in April, a meaningful return to expansion in the region's industrial sector.

- U.S. oil inventories fell by 0.9 million barrels last week, against expectations of a modest build, the kind of tightness that, under normal circumstances, would push crude prices higher.

- On the softer side: U.S. homebuilder confidence fell again in April, and the Fed's Beige Book confirmed what a lot of executives are privately saying, businesses are delaying investment decisions and holding off on hiring, largely because of energy price uncertainty stemming from the Iran conflict. The conflict is creating a slow drag on corporate planning even as equity markets reach new highs. That divergence is worth keeping in mind.

- And then there was Trump's comment that he might fire Fed Chair Jerome Powell if Powell doesn't step down "in time." Markets essentially shrugged.

- The euro/dollar rate barely moved, closing at 1.1802. Either investors don't believe it will happen, or they've decided the Fed's independence is already sufficiently protected by institutional structure. Either way, the non-reaction was itself a signal, six months ago, that kind of threat would have rattled bond markets for a session at minimum.

Bottom Line

The record is in. The S&P 500 at 7,022.95 is not a fluke, it reflects a genuine shift in sentiment driven by Iran ceasefire progress, strong earnings from the financial sector, and a technology cohort that has rediscovered its footing. Wednesday had the kind of breadth that makes rallies feel more durable: banks, tech, consumer names, and individual stories across multiple sectors all contributing on the same day.

That said, I don't think the all-clear has been sounded. The Strait of Hormuz is still largely closed. The Fed Beige Book is telling a more cautious story than the equity markets are. Homebuilder sentiment is soft. Corporate investment is on hold. And a ceasefire is not a peace deal, the structural issues between Washington and Tehran on nuclear capability and Hormuz access are not resolved.

Records deserve to be noted. They don't always deserve to be trusted.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.