For investors looking for a dependable source of passive income, a methodical screening process is needed to distinguish truly lasting dividend payers from risky high-yield choices. A good approach requires looking past the stated dividend yield to evaluate the basic financial soundness of the company. This involves focusing on stocks that provide a good dividend and are also supported by firm profitability, confirming the money to pay it is available, and good financial condition, confirming the company can manage economic declines without threatening its payment. By selecting for high dividend ratings together with adequate profitability and condition scores, investors can create a portfolio made for income longevity.

HNI Corp. (NYSE:HNI), a designer and maker of workplace furniture and residential building products, appears as a prospect from this kind of screening method. The company’s basic profile indicates it could merit additional examination from investors concentrating on income.

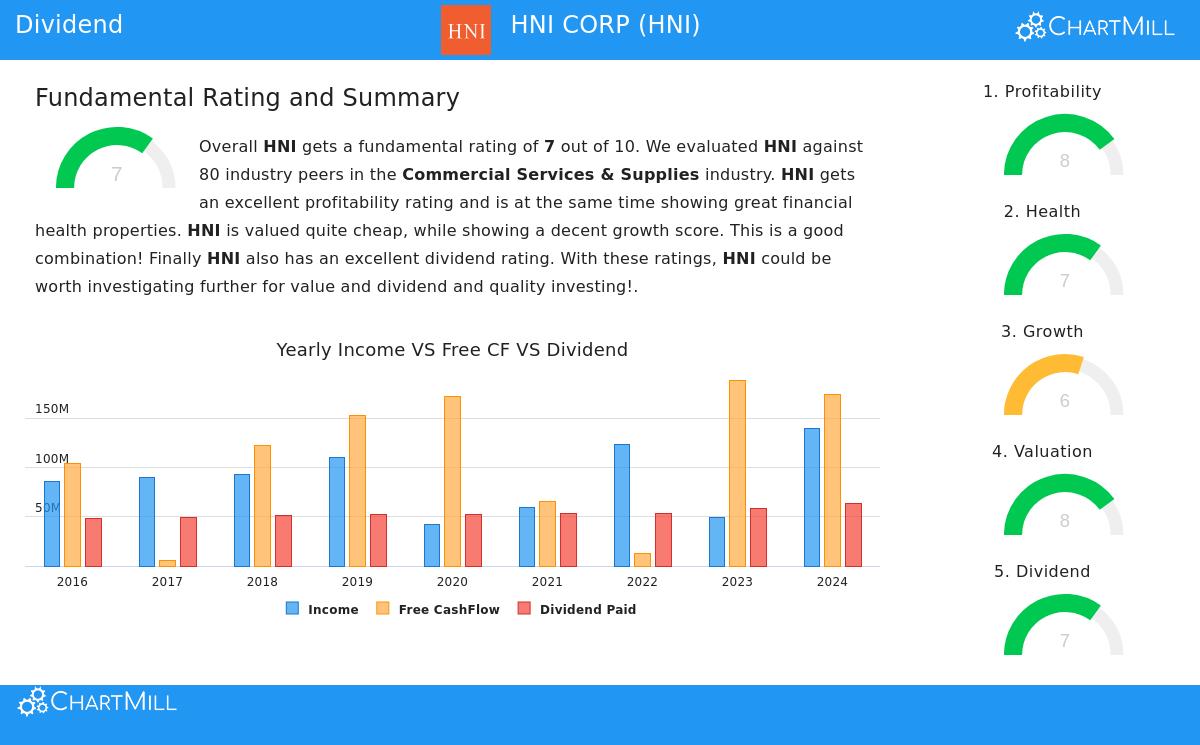

A Balanced Dividend Profile

The central attraction for dividend investors is found in HNI’s steady and trustworthy payment. The company’s dividend is not the largest available, but its traits match an approach centered on longevity and consistent increase over size alone.

- Acceptable Yield with Better Industry Results: HNI’s present dividend yield is 2.65%. This is an acceptable return that notably exceeds both its industry average (0.80%) and the wider S&P 500 (about 1.80%). This shows the company is a dedicated dividend payer in its field.

- A Dependable History: Steadiness is vital in dividend investing. HNI has built a reliable past, having paid and, notably, not reduced its dividend for a minimum of ten straight years. This history offers trust in management’s dedication to giving capital to shareholders.

- Lasting Payout and Increase: The longevity of a dividend is important. HNI’s payout ratio—the part of profits paid as dividends—is about 45%. This is a workable level that keeps sufficient space to put money back into the business and protect against profit changes. Also, while the dividend’s past yearly increase rate is a small 3.58%, analysts forecast better profit growth coming. This implies the current dividend is sufficiently supported and holds possibility for future raises without stressing finances.

Base of Profitability and Condition

A lasting dividend must be constructed on a firm business base. This is where the screening standards for adequate profitability and financial condition show their value, and HNI performs acceptably on both counts.

Profitability Soundness: HNI receives a solid ChartMill Profitability Rating of 8. The company is regularly profitable with positive profits and operating cash flow. Important efficiency measures are persuasive:

- Return on Equity (ROE) of 16.94% does better than 80% of industry counterparts.

- Return on Invested Capital (ROIC) of 12.16% is also higher than the industry standard.

- Margins have displayed good movements, with Gross, Operating, and Profit Margins all getting better lately and stacking up well against others.

This regular profitability is the source that creates the money required to finance the dividend, making the payment seem safe instead of uncertain.

Financial Stamina: HNI’s ChartMill Health Rating of 7 shows a mostly good balance sheet, which is key for a dividend stock’s endurance. Solvency measures are especially firm:

- An Altman-Z score of 3.81 shows a very small short-term chance of financial trouble.

- The Debt-to-Free Cash Flow ratio is a very good 1.80, meaning the company could pay off all its debt with under two years of cash flow.

- A careful Debt-to-Equity ratio of 0.40 displays limited dependence on debt funding.

While some liquidity ratios (like the Quick Ratio) are less strong, the report states that given the company’s firm solvency and profitability, these are less worrisome and normal for its business model. In total, the condition profile suggests HNI has the balance sheet soundness to continue its operations and its dividend during different economic periods.

Valuation Setting

For dividend investors mindful of value, the purchase price is important. HNI seems to be trading at a fair valuation, which can improve the total return possibility. The stock’s Price-to-Earnings (P/E) ratio of 14.7 and Forward P/E of 12.6 are priced lower than over 80% of its industry counterparts and rest notably under the wider market averages. When combined with its firm profitability, this valuation offers a view of a good company that is not expensive.

A Prospect for More Study

HNI Corp. offers an example of how screening for joint soundness in dividends, profitability, and condition can find possible prospects for a lasting income portfolio. It provides a respectable yield supported by ten years of dependable payments, a lasting payout ratio, and a business that is both profitable and financially sturdy. The fair valuation improves its attraction.

For investors using this methodical strategy, HNI stands as a beginning point for more detailed investigation. As with all investments, knowing the company’s particular market forces, competitive challenges, and growth factors in its Workplace Furnishings and Residential Building Products divisions is a necessary following step. You can see the complete basic analysis that shaped this summary in the full HNI Fundamental Report.

Want to find other companies that fit similar standards for dividend longevity? You can see the complete list of outcomes from the "Best Dividend Stocks" screen by clicking here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The information presented is based on data provided and should not be the sole basis for any investment decision. Investors should conduct their own independent research and consult with a qualified financial advisor before making any investment.