Wall Street found its footing as geopolitical tensions cooled and economic data surprised to the upside, though the celebration was dampened by a brutal after-hours crash for Intel and steep sell-offs in GE Aerospace and Abbott Laboratories.

While macro indicators suggest a resilient "Joe Sixpack," corporate earnings reveal a nuanced struggle between technological transitions and consumer pricing power.

It turns out that even when the geopolitical stage moves from "threats of annexation" to "mildly agreeable," the market still finds plenty to lose sleep over, usually involving whether we’re paying too much for airplane engines or if the chip giants can actually keep the lights on.

The Big Picture: A Cold War Thaw in Greenland

I’ve seen some strange catalysts in my time, but watching the Dow Jones (+0.6%) and Nasdaq (+0.9%) rally because the administration decided not to double down on buying a frozen island is certainly up there.

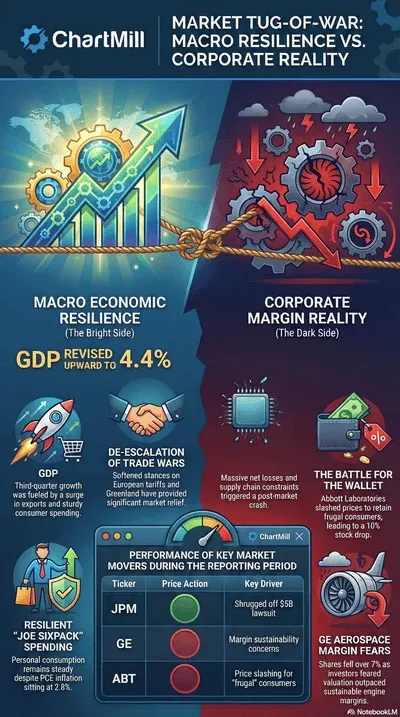

The relief was palpable on Thursday as President Trump softened his stance on Greenland and retracted threats of 10% to 25% tariff hikes against eight European nations. Following a meeting with NATO's Mark Rutte in Davos, a "framework" for a deal was established, allowing everyone to step back from the edge of a trade war.

On the home front, the economy is proving to be a tougher nut to crack than the bears anticipated. Third-quarter GDP growth was revised upward to a robust 4.4%, fueled by a surge in exports and a surprisingly sturdy American consumer.

It seems "Joe Sixpack" is still spending, with personal consumption remaining steady in November, even as the PCE inflation at 2.8% reminds us that the battle against rising costs isn't quite over.

Corporate Earnings: The Good, the Bad, and the Discounted

Despite the green screens, the individual stories were a bit more "horror show" for some heavyweights.

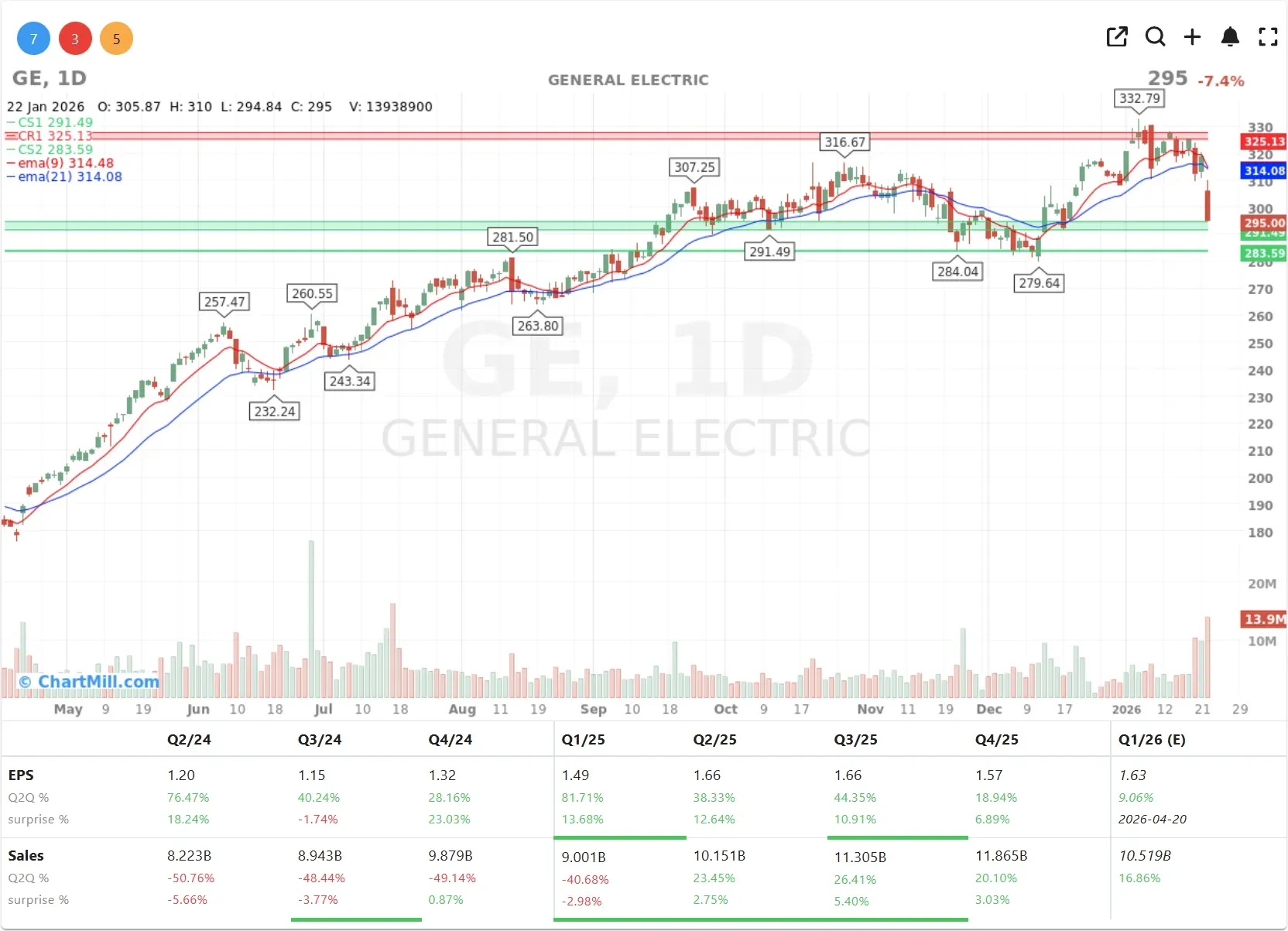

GE Aerospace (GE | -7.38%) found itself in a serious downdraft. Normally, a 20% revenue jump and raised guidance would be a ticket to the moon, but investors seem to have hit the "sell" button on the news, perhaps fearing that the valuation had finally outpaced the engines, especially with margin sustainability concerns casting a shadow.

Even more painful was the haircut taken by Abbott Laboratories (ABT | -10.06%). When a company admits it has to slash prices on nutritional products just to keep a "frugal" consumer through the door, Wall Street tends to run for the hills.

It’s a stark reminder that while the GDP looks great on paper, the battle for the consumer's wallet is getting bloody.

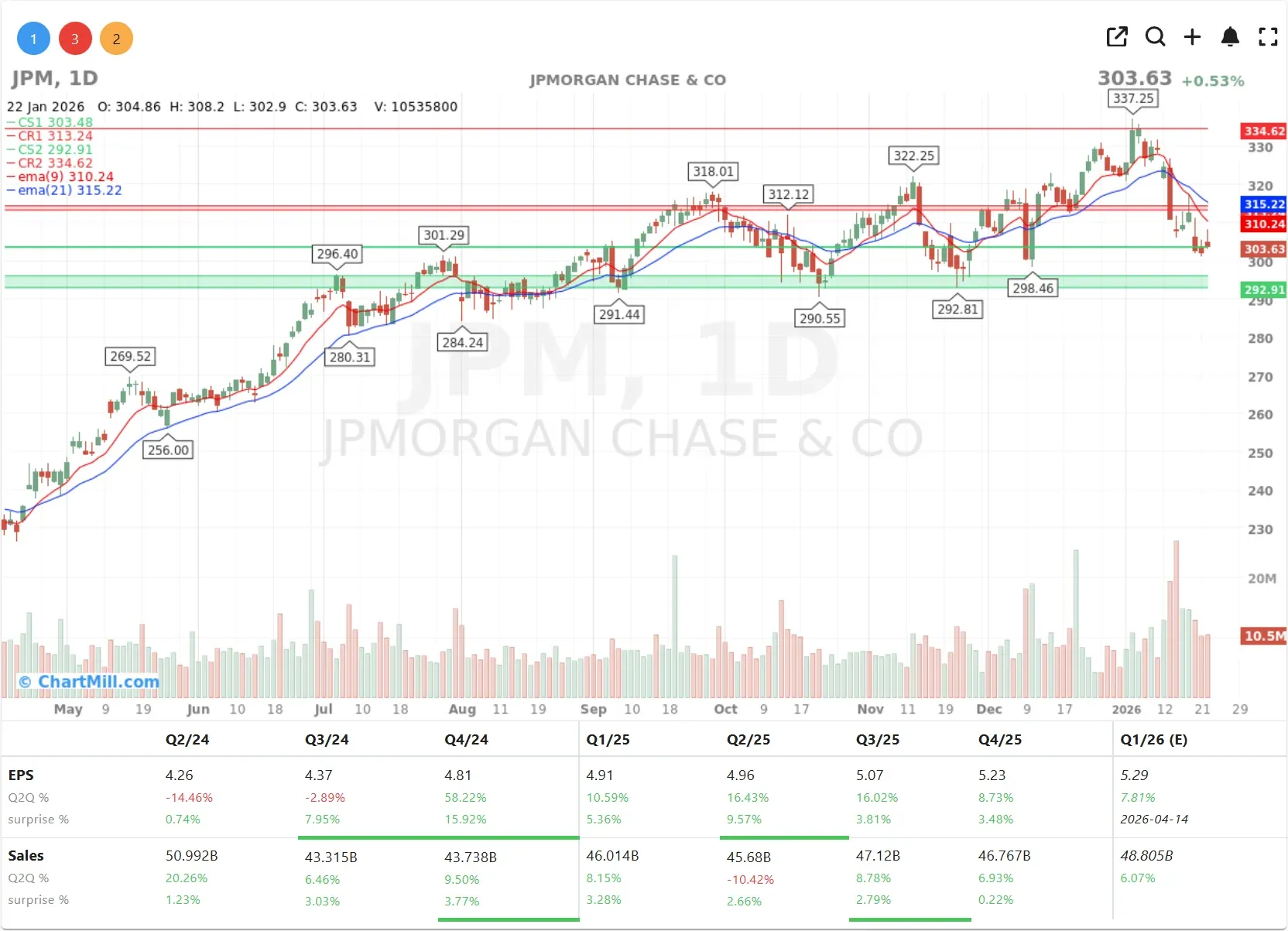

Meanwhile, JPMorgan Chase (JPM | +0.53%) shrugged off a $5 billion lawsuit from the President regarding alleged political discrimination, proving that for big banks, sometimes even a multi-billion dollar headache is just another Thursday.

The Late-Night Double Feature: Intel and Alcoa

The real drama, however, was saved for the after-market session.

Intel (INTC | +0.13%) saw its modest daily gain evaporate instantly after reporting a $333 million net loss for the fourth quarter. Despite beating revenue estimates at $13.7 billion, the market was horrified by a projected Q1 2026 loss of $0.21 per share and supply chain constraints that are expected to hit rock bottom in the coming months.

On the opposite end of the industrial spectrum, Alcoa (AA | -1.14%) also dropped its cards after the bell, revealing a much sunnier 2025 net income of $1.17 billion and record production levels at five of its smelters.

However, the aluminum giant did flag a $70 million EBITDA hit for the first quarter of 2026 due to the loss of certain alumina supply agreements and seasonal effects, leaving investors with a bittersweet taste.

In My View

The current market sentiment feels like a tug-of-war between strong macro data and the cold reality of corporate margins.

While the de-escalation in Davos is a massive win for global trade stability, the bloodbath at Intel and the "discount-driven" growth at Abbott suggest that the internal health of these companies is more fragile than the headline indices would suggest.

My take? Keep your eyes on the consumer, if they stop responding even to discounts, those "sturdy" GDP figures won't be enough to keep the bears at bay.

Kristoff - ChartMill

Next to read: Small-Caps Still Lead as Participation Broadens