Investors looking for expansion possibilities often meet the difficulty of finding companies with solid development potential that are not already valued for flawless results. The "Affordable Growth" or "Growth at a Reasonable Price" (GARP) method tries to close this divide. It concentrates on locating stocks that show strong growth paths but are still available at prices that do not completely account for that future possibility. This process usually includes searching for companies with high marks in development, along with good financial condition and earnings, while making sure the price score stays acceptable to prevent paying too much for anticipated results.

Language-learning service DUOLINGO INC (NASDAQ:DUOL) recently appeared from such a search process. The stock was found by sorting for companies with a ChartMill Growth Rating over 7, good Profitability and Health Ratings, and a Valuation Rating over 5 to remove overly costly choices. Based on its detailed fundamental analysis report, Duolingo displays an interesting profile that matches closely with the affordable growth idea.

A Notable Growth Picture

The center of the GARP method is, expectedly, development. Duolingo’s basic facts show a company in a strong development stage, giving it a high Growth Rating of 8. The company is effectively turning its popular freemium app into major financial progress.

- Rapid Earnings Development: Over the previous year, Duolingo’s Earnings Per Share (EPS) rose by a notable 330.6%, a clear sign of better bottom-line effectiveness.

- Solid and Steady Revenue Growth: Revenue increase is similarly strong, growing by 39.86% in the last year. More significantly, the company has shown a multi-year history, with revenue increasing at an average yearly speed of 60.26% over recent years.

- Positive Future Expectations: Analyst predictions indicate this growth story is not finished. EPS is forecast to develop at an average yearly speed of 43.48%, with revenue predicted to rise by 21.76% per year.

This mix of excellent past results and a solid forecast is exactly what development investors look for. It shows a business that is enlarging efficiently and is anticipated to keep gaining market position in the worldwide online education and language learning area.

Price Assessment: Acceptable Considering the Development

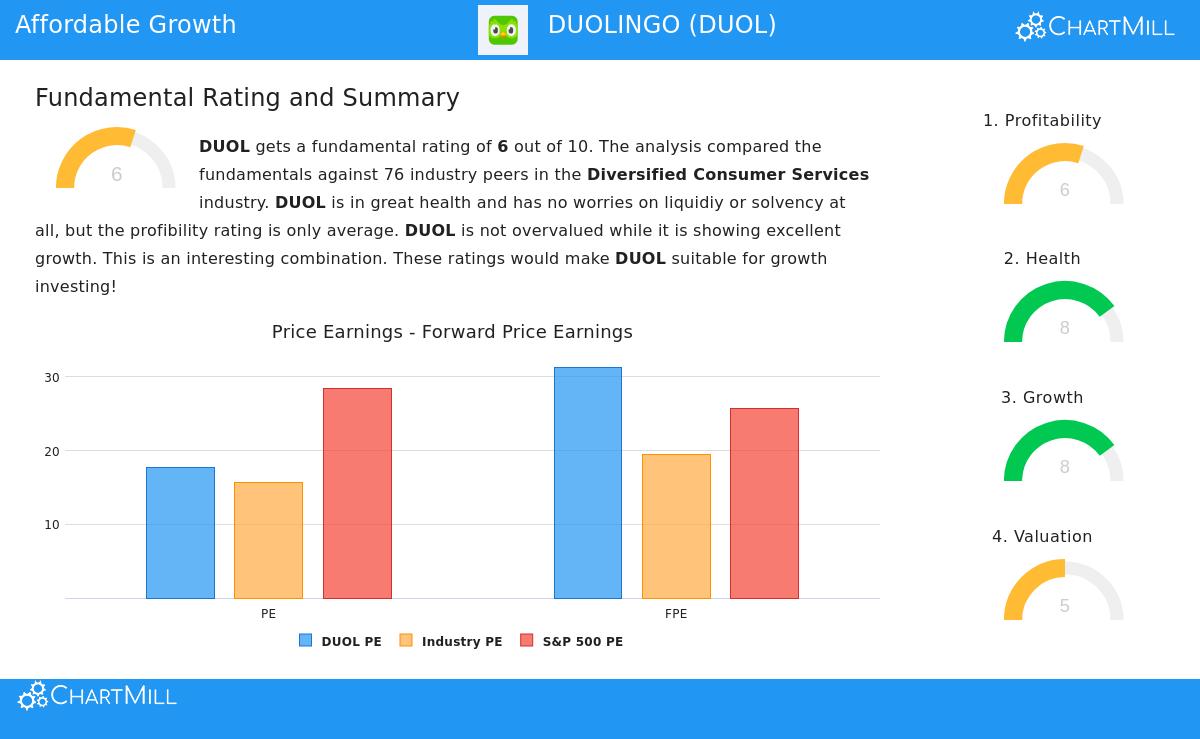

A high-development story is only a sound investment if the cost is suitable. This is where the price evaluation becomes important for the affordable growth method. Duolingo’s Valuation Rating of 5 indicates it is not inexpensive in simple terms, but the measures show a detailed view that supports its inclusion.

- Varied Traditional Measures: The company’s Price/Earnings (P/E) ratio of 17.70 is viewed as costly alone but is actually less expensive than 65.8% of similar companies in the Diversified Consumer Services field. Its forward P/E ratio is greater, matching the field average but above the wider S&P 500.

- The Important Development Adjustment: The most revealing measure for a GARP review is the PEG ratio, which modifies the P/E ratio for predicted earnings development. Duolingo’s low PEG ratio shows that when its high development speed is considered, the present price appears "rather inexpensive." The report directly states that a higher price may be acceptable given the 43.48% expected yearly EPS development.

This review highlights the method's idea: Duolingo’s stock price, while not a deep discount, appears to fairly repay investors for the outstanding development they are buying.

Supporting Basics: Condition and Earnings

For development to be lasting and low-danger, it must be built on a steady base. The affordable growth search requires satisfactory scores in Financial Condition and Earnings to filter out weak companies. Duolingo scores well here, with a Health Rating of 8 and a Profitability Rating of 6.

Financial Condition Points:

- The company has a clean balance sheet with no remaining debt, putting it with the top in its field for financial steadiness.

- Very good cash availability is shown by a Current Ratio and Quick Ratio of 2.82, indicating sufficient means to meet near-term needs and do better than most field peers.

Earnings Advantages and Points:

- Duolingo displays exceptional margins, with a Gross Margin of 72% and a Profit Margin of 40%, doing better than the great majority of its field.

- Returns are also solid, with a Return on Equity of 29.52%.

- The rating of 6 shows a small past issue: the company recorded negative net income in some of the past five years before making a profit lately. However, its present earnings measures are now very high, indicating a effective change to a lasting profitable model.

These parts are important for the method because they lower investment danger. A debt-free, cash-strong company with high margins is much better prepared to handle economic declines and put money into future development projects without needing outside funding.

Summary

Duolingo shows the kind of possibility the affordable growth search process tries to reveal. It is a company showing rapid, high-quality development in both earnings and revenue, supported by a very solid financial base and quickly getting better earnings. While its stock is not lowest-cost, main price measures, especially when development is included, indicate the market may not be completely accounting for its long-term possibility. For investors at ease with the dangers present in development investing, Duolingo presents a situation where solid basics meet a price that still gives an acceptable starting point.

Interested in reviewing other stocks that match this profile? You can perform the same "Affordable Growth" search to view the complete list of qualifying companies here.

,

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions.