I’ve just returned from a week on the slopes in the mountains of Austria, where the air was crisp and the world seemed relatively quiet.

Unfortunately, the same cannot be said for the financial markets. I come back to a desk covered in reports of military strikes, leadership vacuums in the Middle East, and a brewing credit crisis that has investors reaching for the "sell" button.

It’s been a week where a lot happened, and the "tranquility" of vacation feels like a distant memory.

Wall Street Closes in the Red as Credit Fears Resurface

Friday's session turned into a tale of two markets.

On one hand, you had DELL and its blowout, while the majority of the tape drifting lower on a combination of private credit anxiety and renewed Nvidia-related doubts. The Dow Jones shed 1.1% and the Nasdaq declined 0.9%, capping a difficult week for US equities.

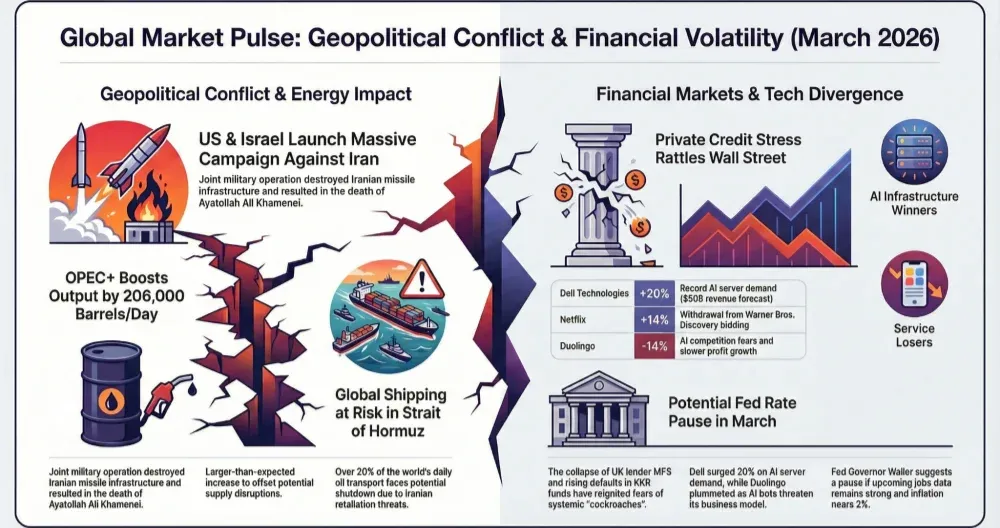

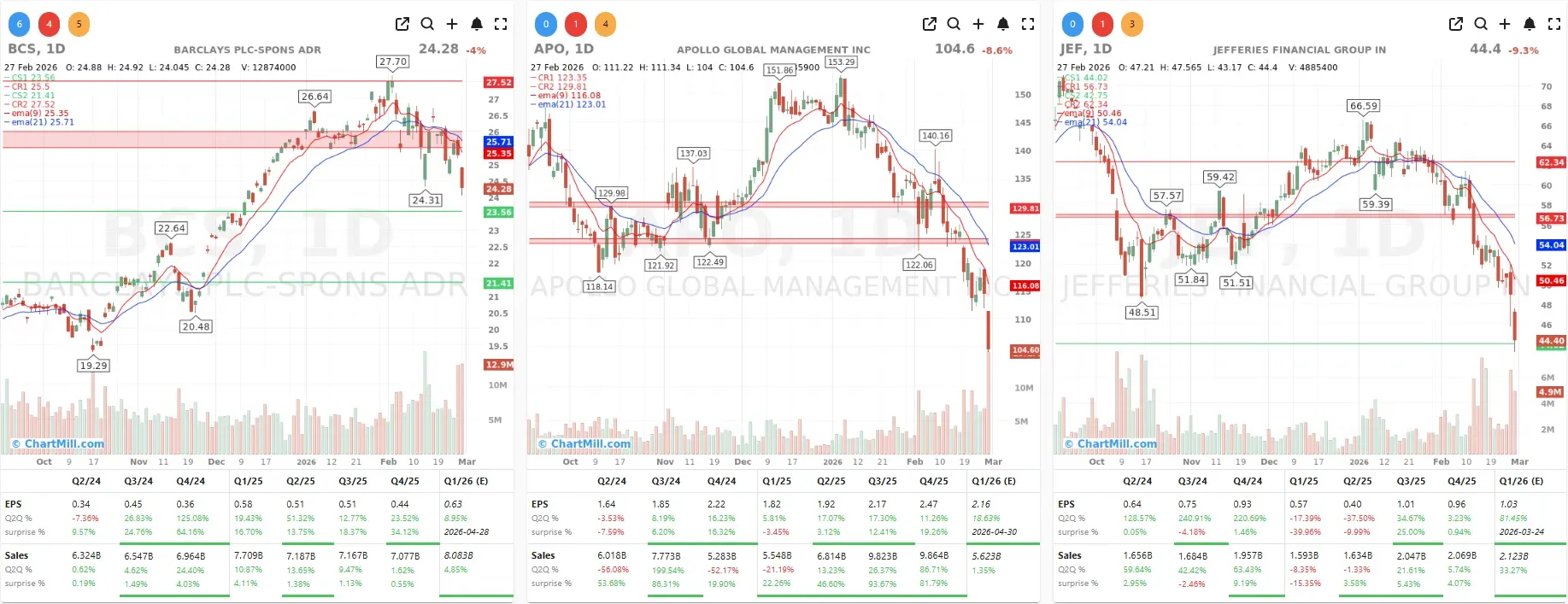

The catalyst for the financial sector selloff was the implosion of UK mortgage provider Market Financial Solutions (MFS), which unraveled earlier in the week amid allegations of fraud, echoing the collapse of auto-parts supplier First Brands just months before.

BCS –3.99% → $24.28 (Barclays, London), APO –8.57% → $104.60 (Apollo Global Management), and JEF –9.31% → ~$44.40 (Jefferies Financial) all took meaningful blows as Bloomberg reported their Atlas SP Partners and lending units were among MFS's creditors, totaling roughly £2 billion in exposure across the group.

The irony is hard to miss: Jefferies is also nursing wounds from the First Brands collapse last year, making this a second significant fraud-adjacent credit event for the firm in quick succession. That kind of pattern tends to leave a lasting mark on investor confidence, and it should.

Meanwhile, KKR –6.34% → $87.68 (KKR & Co.) came under pressure after news broke that one of its credit funds is reporting a sharp rise in non-performing loans. Private credit manager Invico Capital added to the noise by warning its largest clients that a wave of redemption requests could itself destroy value.

JPMorgan CEO Jamie Dimon, who had previously flagged "cockroaches" lurking in the private credit system, was this week making pointed remarks about other banks engaging in reckless behavior. Sometimes it pays to listen the first time someone says things like that.

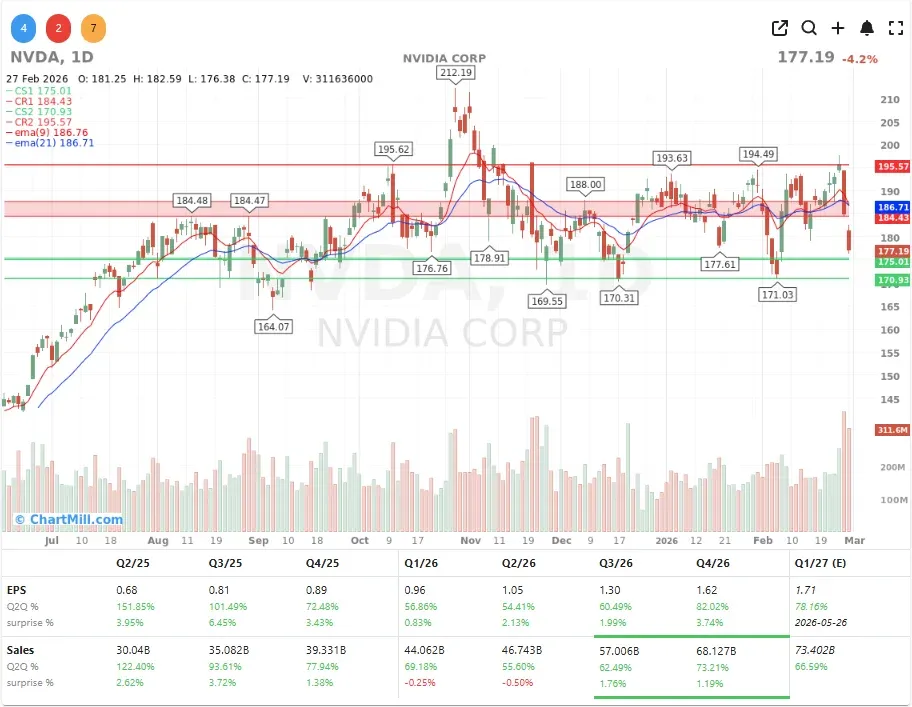

Nvidia: Expectations Met, Investors Unimpressed

NVDA –4.16% → $177.19 (Nvidia) extended its post-earnings slide on Friday, shedding a further 4% after already losing 5.5% on Thursday despite delivering what most analysts would call a spectacular quarterly beat.

The week as a whole was painful for the AI chip leader, and with competition from custom silicon and a broader sentiment shift around AI infrastructure spending efficiency, the near-term path for Nvidia looks less certain than it did even a month ago.

Dell Fires the Cannons and Gets Rewarded

In a session otherwise dominated by red, DELL +21.93% → $148.08 (Dell Technologies) was the standout winner of the day.

In its fourth quarter, revenue surged 39% to $33.4 billion, well ahead of consensus. The infrastructure division - home to the AI server business - posted a 73% revenue jump to $19.6 billion, with operating margins coming in at 14.8%, a figure that clearly surprised even the bulls. For the coming fiscal year ending January 2027, Dell guided for approximately $50 billion in AI server revenue, a number that sits well above what analysts had modeled.

Dell is rapidly transforming from a PC and storage company into one of the most credible AI infrastructure plays in the public market. The operating leverage in that infrastructure division is real, and $50 billion in AI server revenue - if they hit it - would represent a remarkable strategic pivot from where Dell stood just two years ago.

Netflix Steps Away from Warner Bros. and the Market Cheers

The most surprising positive move of the day came from NFLX +13.77% → $96.24 (Netflix).

After months of drama surrounding the attempted acquisition of Warner Bros. Discovery's studio and streaming assets, Netflix formally declined to match Paramount Skydance's improved $31-per-share, all-cash bid, a deal that values all of WBD at roughly $111 billion. PSKY +20.84% → $13.51 (Paramount Skydance) surged on the news.

The Netflix co-CEOs put it plainly: walking away from WBD was not about losing, it was about discipline. The company walked out of the room with a $2.8 billion breakup fee and its capital allocation strategy intact, while signaling a $20 billion content spend for 2026.

Markets seem to agree that this was the right call. Netflix stock, though still below its October 2025 highs when the WBD rumors first surfaced, bounced sharply. WBD -2.19% → $28.17 (Warner Bros. Discovery) edged slightly lower. The Paramount-WBD deal, which must still navigate antitrust review, is expected to close between September and December 2026.

CoreWeave Craters on Aggressive Spending Plans

CRWV –18.51% → $79.56 (CoreWeave) had a rough session after reporting a quarterly loss of $0.89 per share - meaningfully wider than the $0.72 consensus - alongside a capital expenditure blueprint that calls for $30 to $35 billion in AI infrastructure investment this year alone.

Revenue of $1.57 billion just barely edged past estimates, but with an $800 million Q1 guidance miss relative to some analyst models and a capex figure that leaves many questioning the path to free cash flow, the market hit the sell button hard. The company's $66.8 billion revenue backlog is genuinely impressive and suggests durable demand for its GPU-as-a-service platform, but profitability timelines matter to investors, and they remain hazy.

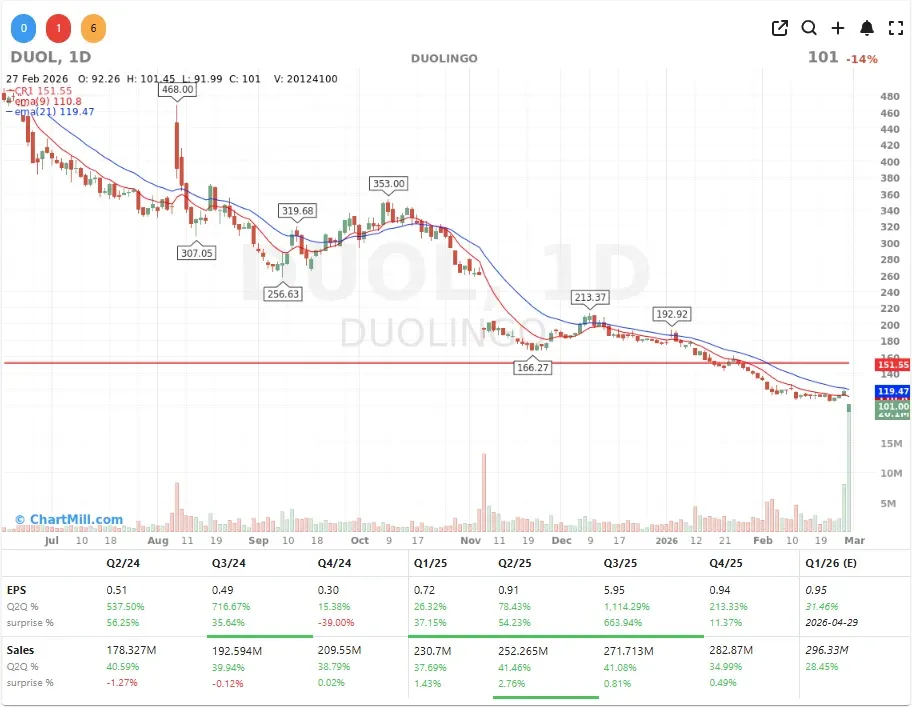

Duolingo: When AI Disruption Becomes a Valuation Reset

DUOL –14.01% → $101.00 (Duolingo) continued its spectacular decline, now off more than 80% from its May 2025 highs.

CEO Luis von Ahn acknowledged a deliberate decision to sacrifice near-term profitability in favor of user growth, investing heavily in AI-powered features to stay relevant as users discover language learning capabilities in tools like ChatGPT and Gemini. Morgan Stanley analyst Nathan Feather pulled the stock from his buy list and slashed his price target from $245 to $100. Citi and Evercore ISI also downgraded the stock.

"We misjudged Duolingo's ability to simultaneously grow its user base and monetize more aggressively per user." — Morgan Stanley analyst Nathan Feather

This is a sobering case study in what AI disruption looks like for a consumer tech company that isn't at the frontier. The business model isn't broken, but the competitive moat has clearly narrowed, and investors are repricing that reality with force.

The Weekend That Changed Everything: US & Israel Strike Iran

Whatever preoccupied traders on Friday feels somewhat secondary now.

On Saturday, February 28, President Trump confirmed in a video address that the United States military had launched a "massive and continuous operation" against Iran alongside Israel, with the explicit goal of dismantling its missile program and preventing nuclear weapons development.

Iranian supreme leader Ali Khamenei, who had not been seen publicly since the strikes began, was confirmed dead by Iranian state media on Sunday, March 1. Trump called him one of the most malevolent figures in modern history and framed the operation as a historic opportunity for the Iranian people to reclaim their own country.

Israel declared a national emergency at the outset of the joint campaign, with the IDF activating air defense systems to intercept incoming Iranian missiles. Prime Minister Netanyahu thanked Trump, characterizing the operation as a necessary step to prevent Iran from obtaining nuclear weapons.

The possibility of retaliatory strikes through Iran's proxy network - including disruptions to oil transport through the Strait of Hormuz, which handles over one-fifth of daily global oil volumes - has immediately become the central question for commodity markets this week.

OPEC+ Moves First and Bigger Than Expected

In a move that could be read as either preemptive management of supply expectations or a geopolitical signal in its own right, eight OPEC+ members - Saudi Arabia, Russia, Iraq, the UAE, Kuwait, Kazakhstan, Algeria, and Oman - voted on Sunday to raise combined output by 206,000 barrels per day from April 1. That figure is roughly 50% above the 137,000 barrel increase markets had anticipated.

The decision comes even as Iran threatens retaliation and the Strait of Hormuz faces real risk of disruption. Whether this output increase is enough to counterbalance a potential Hormuz closure is anyone's guess, but the oil market is bracing for significant volatility when it opens.

The Week Ahead: A Compressed Calendar in a High-Anxiety Environment

This coming week was already set to be dense with macro data.

Monday kicks off with US manufacturing PMI. Wednesday's double-header - US services PMI plus the Fed's Beige Book, will be closely watched for any early signs of economic stress. The week culminates Friday with the US non-farm payrolls report, which Fed governor Christopher Waller has indicated could influence his position on a March rate pause.

Earnings of note include Broadcom, Marvell Technology and retailer results from Best Buy and Target. Chip equipment maker ASMI open books Tuesday.

The geopolitical overlay, however, will dominate all of this. Oil prices, safe-haven flows into gold and Treasuries, and the broader trajectory of the Iran conflict will likely set the tone for every asset class this week. Volatility measures will almost certainly spike at the open.

The Bottom Line

Friday's session already carried the fingerprints of a market questioning its own narratives on AI profitability, private credit quality, and consumer tech valuations.

The weekend events have now added a geopolitical dimension that simply can't be dismissed. Elevated oil prices, safe-haven rotation, and risk-off pressure in equities are the most immediate knock-on effects to watch. Dell's AI server thesis looks stronger than ever; Netflix's financial discipline was rewarded.

But the broader picture heading into Monday is one of genuine uncertainty and that's a market condition that demands both vigilance and patience.

ChartMill Market Desk

Next to read: Breadth Falters Into Friday as Decliners Regain Control