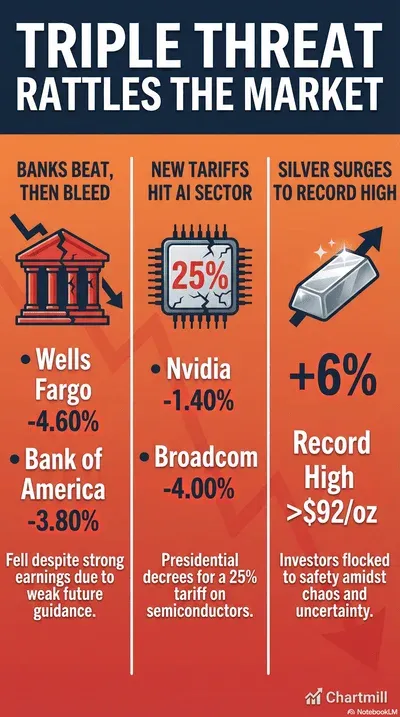

A sea of red washed over Wall Street as major banks beat earnings but failed to impress on guidance, sending the sector tumbling.

Meanwhile, the AI trade took a breather amid confusion over new chip tariffs and potential Chinese bans, while silver quietly rocketed to record highs.

If you logged into your brokerage account today hoping for a continuation of the "January Effect," you were likely met with a sea of red that would make a traffic light jealous.

Wednesday was one of those classic "sell the news" sessions where even good numbers weren't good enough.

I’ve been in this game long enough to know that when the market ignores earnings beats and focuses solely on the "what have you done for me lately" guidance, sentiment is shifting.

Between a banking sector that can’t seem to win and a sudden tariff headache for Big Tech, the path of least resistance today was decidedly lower.

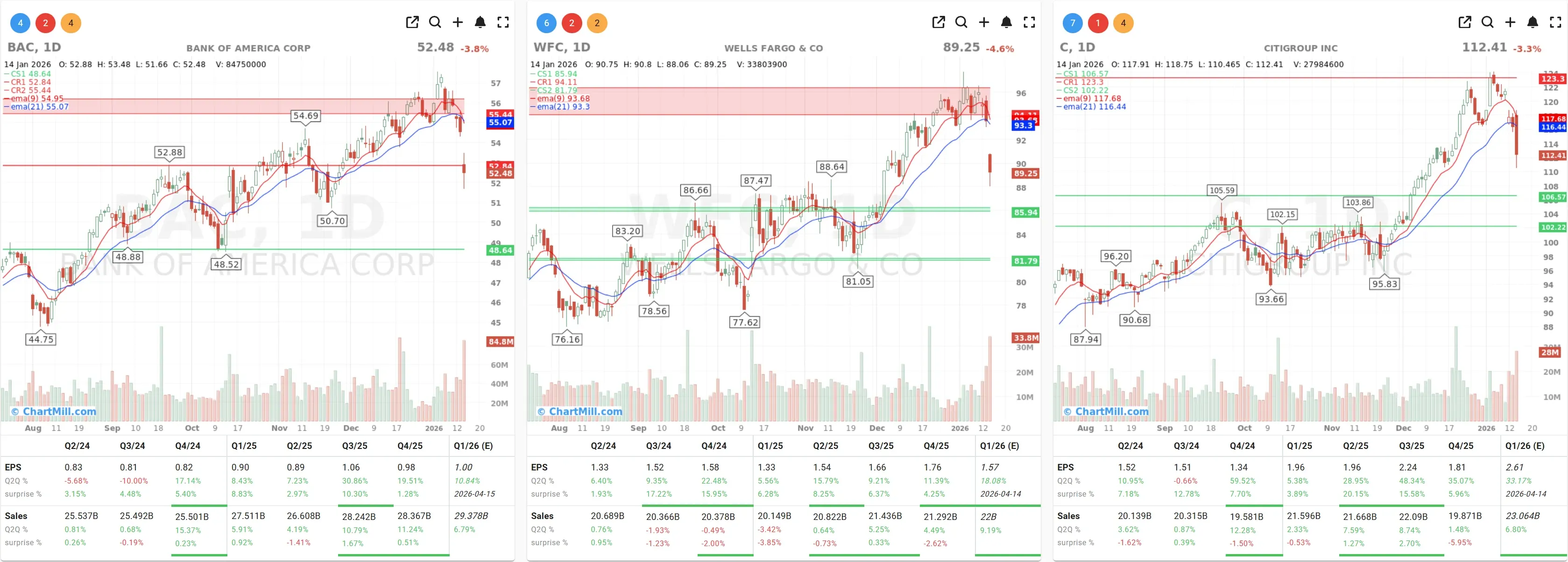

The Banking Blues: Beats Don't Pay the Bills

Let’s start with the big banks, because the reaction here was telling. You’d think billions in profit would cheer people up, but apparently, the bar for "perfection" was set a little too high.

Wells Fargo (WFC | -4.61%) led the race to the bottom. On the surface, things looked fine, they posted adjusted earnings of $1.76 per share, handily beating the $1.67 expected by the Street. But here’s the rub: investors are obsessed with Net Interest Income (NII), and Wells Fargo missed the mark.

Coming in at $12.33 billion against a forecast of $12.46 billion was enough to send traders for the exits. After the stock rallied over 30% in 2025, there was zero margin for error, and today, we found the error.

Then we have Bank of America (BAC | -3.78%). They actually crushed it in Sales and Trading - revenue there was up 10% - which usually saves the day. But management decided to drop a wet blanket on the party by forecasting a 4% jump in non-interest expenses for the current quarter. In this environment, "higher costs" is a dirty phrase.

Citigroup (C | -3.34%) arguably had the messiest quarter. A massive $1.1 billion hit from finally exiting their Russian consumer business dragged earnings down to $1.19 per share.

While some analysts like Herman Chan over at Bloomberg are optimistic about a rebound in net interest income for 2026, the market clearly isn't in a "wait and see" mood. The stock got punished, dragging the entire financial sector down with it.

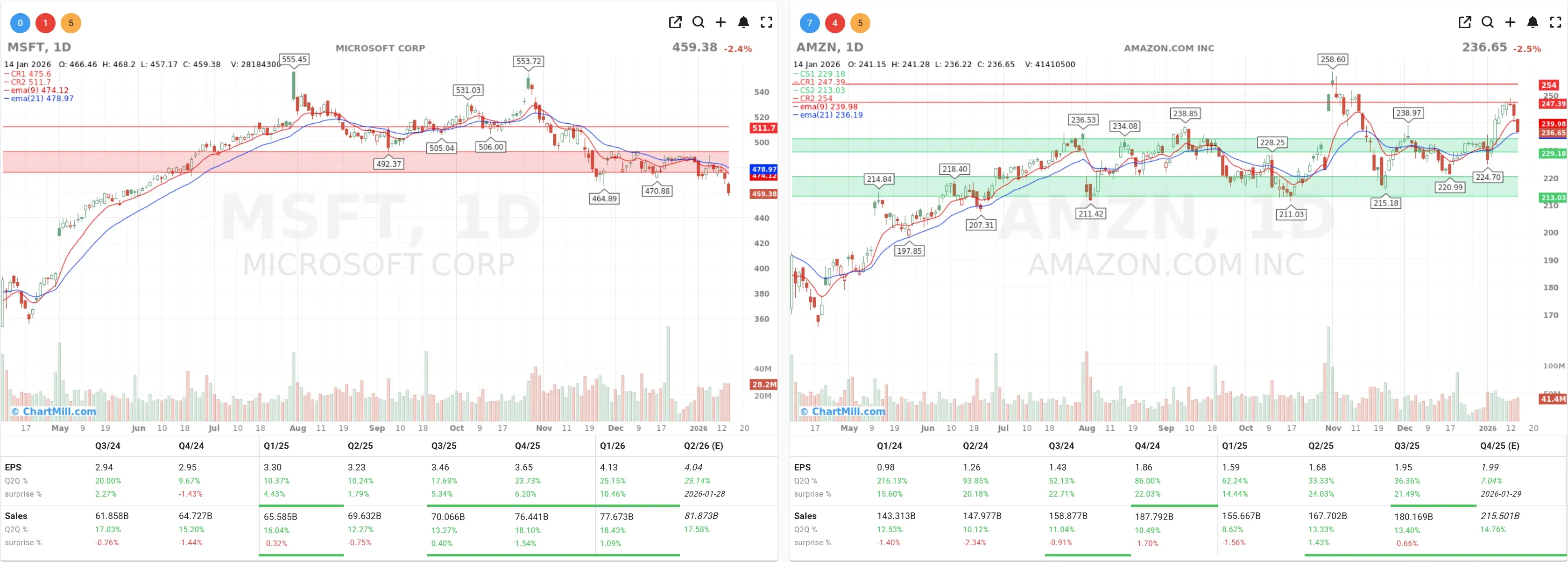

The Chip War: Tariffs, Bans, and Confusion

If the banks were the anchor, the tech sector was the sail that got shredded. The Nasdaq finished down 1%, but the pain in the AI darlings was much more acute.

We saw broad profit-taking in the usual suspects: Microsoft (MSFT | -2.40%), Amazon (AMZN | -2.45%), and Meta Platforms (META | -2.47%) all shed significant value. But the real story is the confusion swirling around Nvidia (NVDA | -1.44%).

Here is the situation: Reports from Reuters suggest Chinese authorities have essentially banned the import of Nvidia's H200 AI chips. Almost simultaneously, President Trump signed decrees under "Section 232" imposing tariffs on chips and rare earth metals.

While there are exceptions for domestic AI use, Trump explicitly stated he wants the U.S. government to "earn 25%" on chips sold to China.

It’s a geopolitical tug-of-war with Broadcom (AVGO | -4.15%) and Nvidia stuck in the middle. Is it a ban? Is it a tax? The market hates uncertainty, and right now, we have it in spades.

Macro & Geopolitics: The Weird Gets Weirder

Just when you think you’ve seen it all, 2026 throws a curveball. We have reports that the White House is initiating a criminal investigation into Federal Reserve Chair Jerome Powell. I cannot stress enough how much markets dislike threats to central bank independence. It adds a layer of risk premium to every asset class.

And yes, you read the headlines correctly: The "Greenland Purchase" is back. Vice President Vance is reportedly meeting with Danish officials to discuss a takeover. It sounds like fiction, but in a world where resource security is king, maybe it’s the new normal.

Amidst this chaos, the "fear trade" is alive and well. Silver prices surged 6% to a record high of over $92 per troy ounce. When tech wobbles and geopolitical heat rises, money flees to hard assets.

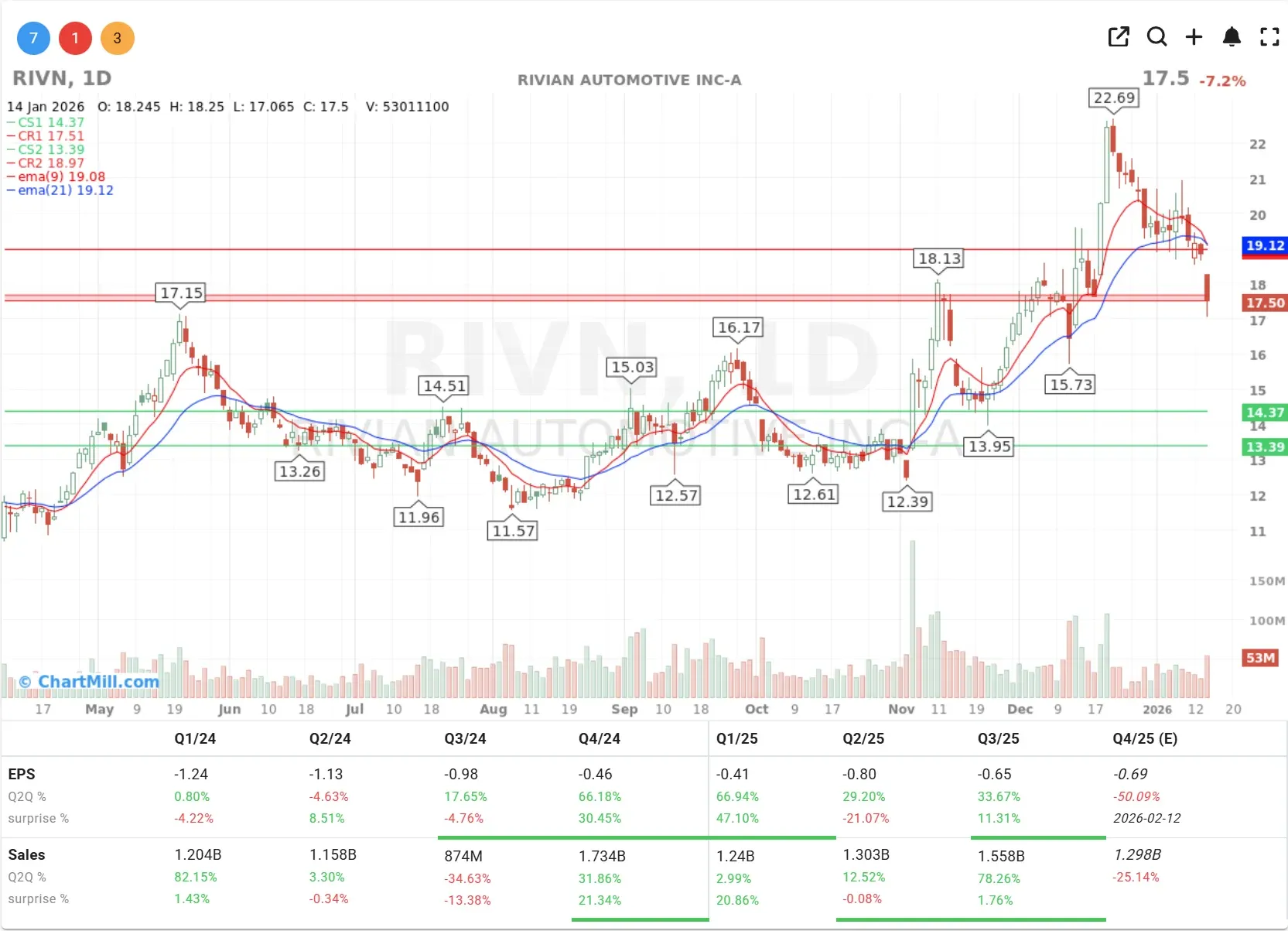

On the data front, we actually got some "Goldilocks" numbers. November PPI rose just 0.2%, and core inflation slowed, supporting the soft-landing narrative. Retail sales jumped 0.6%, proving the American consumer is still spending, unless you're selling electric trucks, apparently. Rivian (RIVN | -7.16%) got hammered after UBS slapped a "Sell" rating on the stock.

My Take:

The market is currently trying to digest too many conflicting signals. Strong retail data says "buy," but weak bank guidance and tariff wars say "sell."

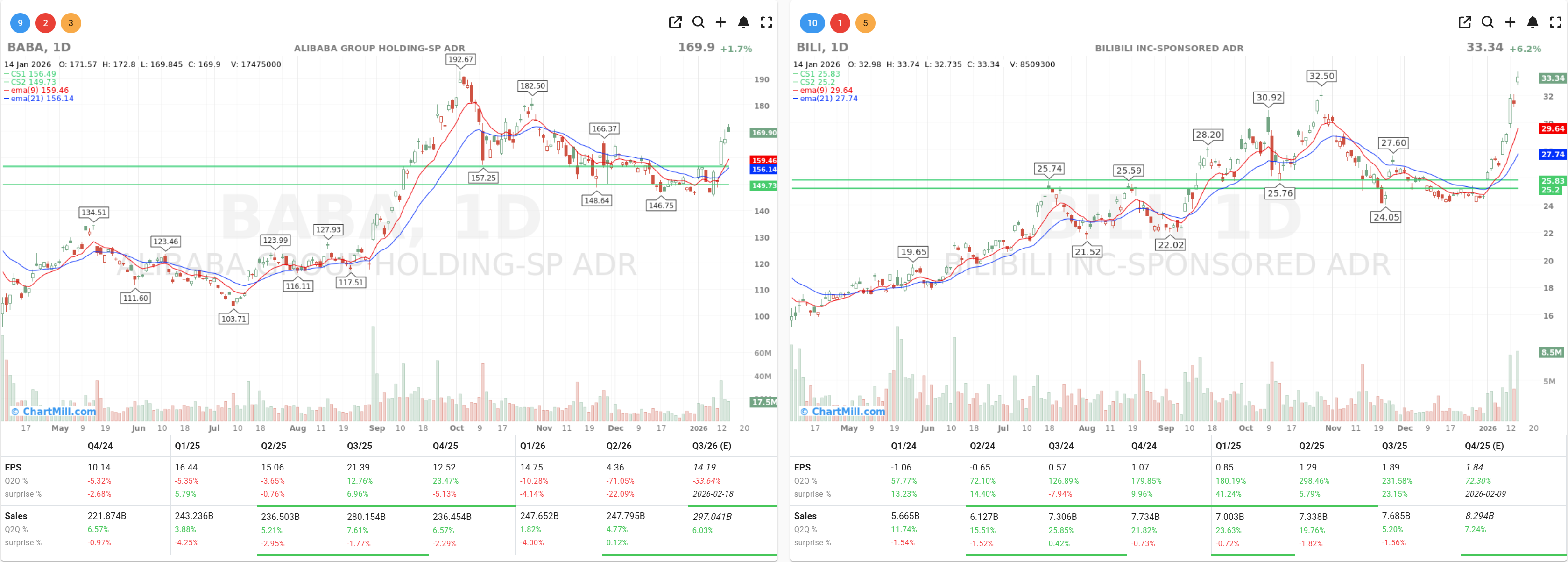

My advice? Watch the reaction in the Asian markets to the Nvidia news. If Chinese tech giants like Alibaba (BABA | +2.00%) and Bilibili (BILI | +6.00%) - which actually rallied today - start to buckle, this tech correction might have legs. Keep some powder dry; volatility is back on the menu.

Kristoff - ChartMill

Next to read: Small Caps Take the Lead While Mega-Caps Cool Off