Wednesday, April 1 was supposed to be the day investors got clarity. Instead, Nike handed them a gutting earnings miss while Trump delivered an Iran speech that confused as much as it comforted.

The Rundown

- Wall Street closed higher for the second consecutive session, continuing Tuesday's relief rally though the mood was more cautious as mixed geopolitical signals made for a volatile ride.

- Nike cratered 15.51% to $44.63 after guiding for continued revenue declines.

- Trump's speech on Operation Epic Fury said objectives were "almost achieved" while simultaneously promising two to three more weeks of escalation.

- Intel surged 8.8% on a $14.2 billion deal to buy back Apollo Global Management's 49% stake in its Fab 34 plant in Ireland.

- US macro data impressed.

- Commodities: Gold up, Brent crude flat; EUR/USD settled at 1.1582.

Wednesday was the kind of session that gives you whiplash.

Nike implodes. Trump speaks but leaves everyone more confused than before. Oil spikes.

And yet the market - that ever-stubborn discounting machine - went ahead and posted a second consecutive gain. It didn't panic. It didn't capitulate. It processed the noise and kept moving.

Whether that composure is earned confidence or willful optimism, I'll let you decide. But it was impressive to watch.

The Economy Sends a Clear Signal the Geopolitics Cannot

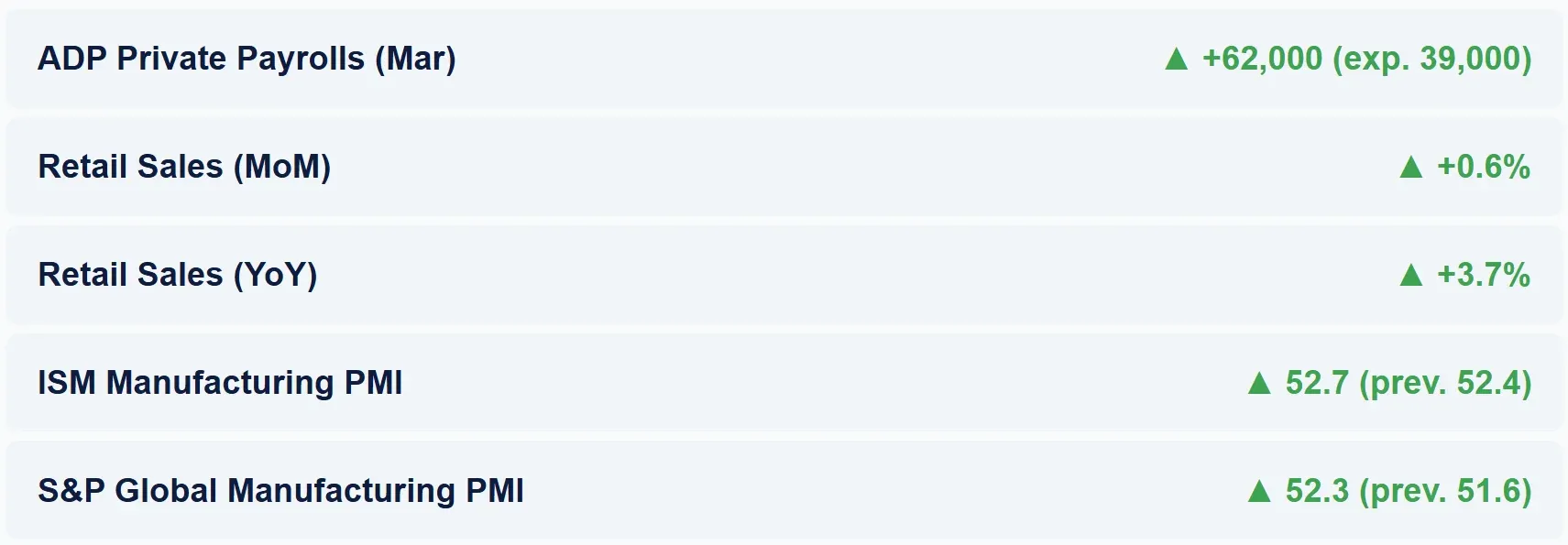

The one unambiguous bright spot of the session was the US macro picture, which came in better than expected across the board and gave bulls something concrete to hold onto.

The ADP private payrolls report showed the private sector added 62,000 jobs in March, well above the consensus estimate of 39,000, and a reassuring sign that the labor market remains resilient despite the energy price shock rippling through the economy.

Retail sales growth of 0.6% month-on-month and 3.7% year-on-year further underscored that the American consumer, though undoubtedly squeezed by $4-a-gallon gasoline, is not yet throwing in the towel.

Manufacturing data added another layer of encouragement.

The ISM Purchasing Managers' Index climbed from 52.4 to 52.7 in March, remaining comfortably in expansion territory, a fact that matters, given how sensitive industrial output is to energy costs and supply chain disruption.

Nike: Three Downgrades and a Stock That Doesn't Know Where the Floor Is

If the macro story was the rally's foundation, Nike (NKE | ▼15.51%) was its unwelcome reminder that not every company gets to share in the mood.

The sportswear giant's fiscal Q3 2026 report - released late Tuesday - turned Wednesday's pre-market session into a bloodbath for holders. The stock closed down 15.51% at $44.63, its worst single-session loss in years, as the market reacted to guidance that was nothing short of sobering: management guided for continued revenue declines not just through the current quarter but extending deep into fiscal year 2027.

China sales, which were supposed to be a pillar of any recovery story, are now expected to fall 20%.

Three major brokerages moved simultaneously to strip Nike of their buy recommendations and it is the unison of the action, more than any single cut, that tells you how far analyst patience has worn thin.

- Goldman Sachs (GS) analyst Brooke Roach downgraded from Buy to Hold, slashing her price target from $76 to $52, citing a recovery timeline that keeps stretching further into the future as the economic environment deteriorates.

- Bank of America (BAC) analyst Lorraine Hutchinson made the same move, cutting from Buy to Hold and lowering her target from $73 to $55, she had been modeling revenue growth for the current quarter, only to see management guide for yet another decline.

- And JPMorgan (JPM) analyst Matthew Boss rounded out the trio, dropping from Buy to Hold with a target reduction from $86 to $52, now penciling in flat EPS growth for the next nine months and not expecting operating margins to recover to 10% until fiscal year 2029, a year later than he previously projected.

I find myself thinking that the market was not punishing Nike purely for one bad quarter. The real anxiety is philosophical: is the brand's turnaround story intact, or has the timeline simply become impossible to defend?

When three of the Street's sharpest pencils all reach the same conclusion on the same morning, the answer tends to be the latter.

At $44.63, Nike now trades at levels not seen in years. The question is whether that represents a value opportunity for patient investors or the beginning of a longer re-rating lower. I lean cautious until management can show actual growth, not just the promise of it.

Zero Clarity: Trump's Iran Address Leaves Markets Guessing

In a speech that lasted less than twenty minutes, President Trump said that the key strategic objectives of Operation Epic Fury were "almost achieved", words that, on their own, would have provided genuine relief.

But within the same address, he promised two to three more weeks of "extreme" strikes against the Iranian regime, vowing to "bring them back to the Stone Age."

The oil market rendered its verdict instantly. Brent crude, which had spent much of the session trading just above $100/barrel on residual peace optimism, spiked $7 during the speech to approximately $106/barrel, now sitting 73% above where it started the year.

That is not the price action of a market that heard a coherent exit strategy. The contradictions in the speech were hard to ignore: on one hand, success is near; on the other, escalation is coming. Iran, for its part, called Trump's recent posturing "absurd" via Bloomberg, and showed no signs of willingness to open the Strait of Hormuz, the precondition Trump himself set for any ceasefire consideration.

Meanwhile, the New York Times reported that the Pentagon is doubling its A-10 attack aircraft fleet in the Middle East, a detail that does not quite square with the "almost done" narrative.

Also worth watching: the Financial Times reported that Trump has privately threatened to halt weapons deliveries to Ukraine in order to pressure European allies into joining a coalition to reopen the Strait of Hormuz.

That is a significant geopolitical lever that, if pulled, has implications well beyond oil markets. European defence and energy names could see renewed volatility if that threat materialises into policy.

Equity markets largely absorbed the speech without flinching. The indices held their gains. That resilience is either a sign of deep underlying confidence in the US economic engine - backed by today's solid macro numbers - or a sign that investors have simply stopped trying to trade every headline out of Washington. Perhaps both.

Intel Reclaims Its Irish Kingdom and Drags the Entire Chip Sector Higher

The deal of the day belonged to Intel (INTC | ▲8.84%).

The chipmaker announced it would pay $14.2 billion to repurchase the 49% stake that Apollo Global Management (APO | ▼1.05%) held in a joint venture tied to its Fab 34 facility in Leixlip, Ireland.

The original transaction, completed in 2024, had seen Apollo-managed funds inject $11.2 billion into the JV, giving Intel equity-like capital at a time when it desperately needed balance sheet breathing room.

Now, with the financing environment apparently more manageable, Intel is buying that stake back, funding the transaction through a combination of existing cash and approximately $6.5 billion in newly issued debt.

Fab 34 is not just any factory. It is Intel's high-volume production facility for its most advanced process nodes - Intel 4 and Intel 3 - and the plant where products like Core Ultra processors and Xeon 6 data-centre chips roll off the line.

By consolidating full ownership, Intel removes an intermediary and positions itself to capture more of the economics from what is increasingly looking like a strategically vital asset in the AI era. The market agreed: the stock jumped 8.8%, its best day in months.

The enthusiasm spread through the semiconductor sector with notable conviction.

-

Western Digital (WDC | ▲10.1%) and SanDisk (SNDK | ▲9.0%) were among the session's biggest winners.

-

Micron Technology (MU | ▲8.9%) and Seagate Technology (STX | ▲8.0%) also had standout sessions.

There was no single catalyst behind this sector-wide move beyond the general sense that Intel's strategic conviction was contagious, and that semiconductor demand in an AI-driven world is not going away regardless of what happens in the Strait of Hormuz.

Energy Stocks Pay the Price of Peace Optimism

On the other side of the ledger, the integrated oil majors continued to feel the weight of ceasefire speculation.

Chevron (CVX | ▼4.6%) and Exxon Mobil (XOM | ▼5.2%) both retreated meaningfully as investors priced in the possibility that a resolution to the Iran conflict could eventually take oil prices lower.

It is worth noting the irony here: the actual oil price remained stubbornly above $100/barrel, and in fact crept toward $106 after Trump's address. The gap between where oil stocks were trading and where oil itself was trading reflects the market's forward-looking habit of pricing the outcome, not the present reality.

If a genuine ceasefire materialises and Hormuz reopens, energy costs would fall sharply and both companies' earnings would compress accordingly. Investors are getting ahead of that, even if the war itself has not ended.

Earnings Spotlight: nCino and Cal-Maine Deliver, RH Does Not

nCino, Banking Software That Beats With Ease

Banking software developer nCino (NCNO | ▲10.6%) delivered the kind of earnings beat that reminds you not all technology is struggling.

The company reported Q4 fiscal 2026 adjusted EPS of $0.37 against an analyst consensus of $0.21 - a 76% beat - while revenue of $149.7 million edged past expectations.

Full-year subscription revenue grew 12% to $523.1 million. The strong results, combined with robust forward guidance, pushed the stock up sharply and underscored the demand for AI-integrated financial software platforms. ACV (annual contract value) rose 17% year-over-year to $602.4 million, a sign that customer acquisition and expansion are both working.

Cal-Maine Foods, Eggs Still Printing Money

Egg producer Cal-Maine Foods (CALM | ▲5.3%) posted fiscal Q3 2026 results that beat on the earnings line, with EPS of $1.06 clearing the $0.89 consensus.

Revenue came in at $667 million against analyst expectations around $642.5 million. What continues to impress about Cal-Maine is its product mix evolution: specialty eggs now account for more than 50% of total shell egg sales, a diversification that insulates margins and reflects a deliberate and successful upmarket shift.

The stock gained 5.3%, a solid move for a company that tends to be overlooked outside of commodity-focused circles.

RH, A Furniture Company That Has Run Out of Excuses

There was less to celebrate at RH (RH | ▼19.5%).

The luxury home furnishings retailer posted fiscal Q4 2026 results that missed on both revenue and earnings, with adjusted EPS of $1.53 falling well short of the $2.22 Wall Street had expected.

Revenue of $842.6 million missed consensus by roughly $30 million. Management pointed to approximately $30 million in impact from tariff-related supply chain resourcing and a further $10 million from adverse weather as the main culprits.

The problem is that investors have heard variations of these explanations before. Forward guidance was equally uninspiring, with Q1 2026 revenue expected to decline 2–4% year-over-year.

The stock dropped 19.5% to a new 52-week low.

Commodities and Currencies: Gold Gleams, Oil Grips

Gold continued its ascent, gaining 2.5% to approximately $4,750 per troy ounce.

The combination of geopolitical uncertainty, a still-elevated inflationary backdrop, and persistent questions about the dollar's trajectory has created a near-ideal environment for the precious metal. It is becoming harder to argue against gold as a portfolio component at the moment, even for those who historically view it as an unproductive asset.

The oil market, as noted, settled above $100/barrel despite the peace narrative that has been lifting equity markets.

Brent crude briefly touched $106 during Trump's speech before pulling back slightly. The stubborn persistence of triple-digit oil prices is worth keeping front of mind: every additional week that the Strait of Hormuz remains disrupted is another week that energy inflation embeds deeper into corporate cost structures and consumer budgets.

The average US gasoline price has now risen by a third in a single month to more than $4 per gallon, a politically explosive figure in any year, let alone one this close to midterm positioning.

On the currency side, the euro continued to firm against the dollar, settling at 1.1582. US interest rates ended the session close to unchanged, suggesting the bond market is not yet reading the macro data as a reason to revise rate expectations. That steadiness in rates is arguably one of the less-discussed props under equity valuations right now.

Conclusion

Wednesday April 1 was a session that tested investor conviction on multiple fronts simultaneously and, for the most part, conviction held.

The macro data was genuinely strong and deserves credit: a jobs market, a consumer, and a manufacturing sector all moving in the right direction despite being subjected to a severe oil-price shock is not a trivial achievement. That is the kind of fundamental resilience that makes bear cases harder to sustain.

But the risks are equally real and should not be papered over by a second consecutive green close.

Nike's collapse is a company-specific story, yes, but it is also a warning about the dangers of turnaround narratives that keep pushing the finishing line further away.

Trump's Iran speech did nothing to establish a credible timeline for the war's end and as long as the Strait of Hormuz remains closed, the oil shock will keep compressing margins across industries and household budgets alike. At $106/barrel and a gasoline price above $4, the clock is ticking.

Intel's bold Fab 34 move is a genuine positive for the chip sector and a vote of confidence in the long-term demand picture, but it also adds leverage to a balance sheet that remains work in progress.

I will be watching Thursday's session closely for signs of whether the market can sustain this resilience, or whether the contradictions of the past 48 hours finally start to add up.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Market Breadth Recovery Continues, but the Bigger Trend Still Needs Work