For investors looking for opportunities where the market price of a company may not fully show its basic financial condition, a careful value method can be a helpful beginning. One frequent plan involves filtering for companies that seem basically priced low by common measures while still showing good operational soundness, earnings, and possibilities for expansion. This technique seeks to spot possible deals, stocks selling for less not because of bad business quality, but maybe due to market shortsightedness or temporary feeling. The aim is to find businesses where a good base indicates the present price difference may narrow in the future.

Using this view, Vertex Pharmaceuticals Inc. (NASDAQ:VRTX) appears as a candidate deserving more examination. The biotechnology company, recognized for its life-changing treatments for cystic fibrosis and an increasing set of projects in other severe illnesses, shows an interesting mix of traits that fit a "good value" investment idea.

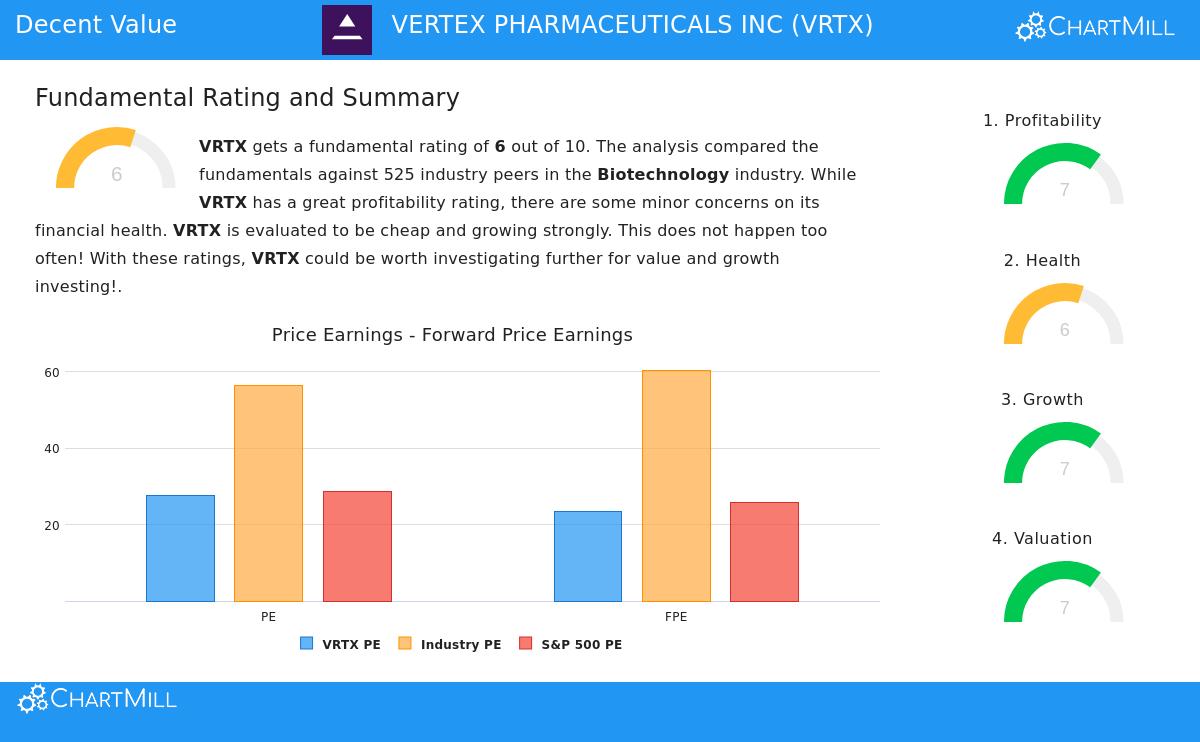

Valuation: A Relative Discount in a High-Priced Field

The center of any value hunt is spotting a difference between price and value. Vertex's valuation measures indicate such a difference may be present, especially within its own field. The company's basic analysis report gives it a Valuation Score of 7 out of 10, meaning it is priced more appealingly than many similar companies.

- Price-to-Earnings (P/E) Ratio: At 27.53, Vertex's P/E ratio is similar to the wider S&P 500 average. However, compared to the biotechnology field's average P/E of about 56.6, Vertex sells at a notable discount, ranking lower in price than over 93% of its field peers.

- Forward-Looking Multiples: The situation is alike for forward-looking measures. Its Price/Forward Earnings ratio of 23.48 is also close to the S&P 500 average but sits much lower than the field average, putting it in the least expensive 7% of its industry.

- Cash Flow & EBITDA: The valuation argument gets stronger when examining cash creation. Based on both its Enterprise Value/EBITDA and Price/Free Cash Flow ratios, over 93% of biotechnology companies are priced higher than Vertex.

For a value investor, these measures are key. They suggest the market is not using the usual high-growth biotech extra price to Vertex, possibly because of worries about its dependence on cystic fibrosis treatments or project progress. This creates the "margin of safety" that value founders like Benjamin Graham stressed, buying a good asset at a price much below its peer group average.

Financial Health: A Strong Balance Sheet

A low price is only appealing if the company is financially stable enough to survive market changes and put money into its future. Vertex does very well here, getting a Health Score of 6. Its most notable trait is a balance sheet with almost no debt, putting it in the top group in its capital-heavy industry. A structure with no debt gives great room for strategic buys, research and development spending, and surviving possible clinical or regulatory problems.

While its current and quick liquidity ratios are seen as being in the lower part of the industry, they stay at good levels (2.36 and 2.00, in order), showing no near-term payment worries. Also, the company has been steadily lowering its share count over recent years, a sign of management's belief and a move good for shareholders that raises the ownership part of remaining investors.

Profitability: Outstanding Earnings Ability

Value investing is not about buying poor companies inexpensively, it's about buying good companies at a fair price. Vertex's earnings ability is outstanding, scoring a 7. The company works with field-leading margins that are admired by its peers.

- Its Operating Margin of 38.70% is better than 98% of the biotechnology industry.

- It has a strong Profit Margin of 31.35% and an excellent Gross Margin of 86.28%.

- Returns on capital are very good, with a Return on Invested Capital (ROIC) of 17.58%, doing better than 97% of the industry.

This high level of earnings ability is basic to the value argument. It shows that Vertex is not just a risky story but a very efficient business operation creating large cash flows from its sold products. This earnings ability provides the profit base that makes its relatively low valuation multiples especially worth noting.

Growth: A Good Past and a Speeding Future

Lastly, an interesting value candidate should have a growth path that can drive a new price level for its stock. Vertex's Growth Score of 7 shows a changing profile. While past Earnings Per Share (EPS) growth has been uneven due to single events, the basic business shows forceful increase.

Revenue has grown at an average yearly rate of 21.5% over recent years and rose 10.33% in the last year. Most importantly, the future appears positive. Experts expect EPS to grow at a notable 150.5% yearly in the coming years, with revenue growth predicted at a good 9.75%. The report states that the EPS growth rate is speeding up, a positive sign that the company's investments beyond its main cystic fibrosis work may be starting to show results.

For an investor, this mix of good past revenue growth, speeding future earnings expectations, and a fair valuation is a strong combination. It suggests the market may be pricing the company too low in its change into a multi-franchise biotech leader.

Conclusion

Vertex Pharmaceuticals shows a detailed case for investors using a careful value plan. It is not a deeply troubled asset but a financially sound, very profitable company selling at a price discount related to both its excellent financial results and its high-growth field. Its balance sheet with no debt provides a buffer, while its speeding earnings growth offers a possible trigger. This match of good valuation, very good health, high earnings ability, and strong growth makes VRTX a stock that deserves more basic study.

You can see the full basic analysis for Vertex Pharmaceuticals here.

Find More Possible Value Chances The hunt for low-priced companies with good basics is a continuous process. If you are interested in filtering for other stocks that fit similar "good value" rules, you can look further using this pre-set stock filter.

,

Disclaimer: This article is for information only and does not make financial advice, a suggestion, or an offer to buy or sell any securities. The analysis uses data and scores from ChartMill as of the date written. Investors should do their own complete study and think about their personal money situation and risk comfort before making any investment choices.