For investors looking to balance the search for high-growth companies with a careful view on price, the "Growth at a Reasonable Price" (GARP) method provides a practical middle path. This approach seeks to find companies that are increasing their earnings and revenues faster than average, but whose stock prices are not excessively high. The aim is to sidestep the speculation that can accompany the most aggressive growth stocks while still gaining from solid business progress. One method for applying this strategy is an "Affordable Growth" screen, which selects stocks with high growth scores, good profitability and financial strength, and a price that seems fair. A present example from this screen is VERTEX PHARMACEUTICALS INC (NASDAQ:VRTX).

Growth Profile: A Strong Engine

The central idea of any GARP strategy is, of course, growth. Vertex Pharmaceuticals shows a strong growth story, receiving a ChartMill Growth Rating of 7 out of 10. This score indicates good performance in both recent results and future estimates, which is important for lasting investment gains.

- Past Revenue Growth: The company has built a very good history, with Revenue increasing at an average yearly rate of 21.50% over recent years. In the last year, Revenue rose by 10.33%.

- Earnings Acceleration: While past Earnings Per Share (EPS) growth has been uneven, the most recent year showed a large increase of over 3,300%. Also, analysts predict a notable speed-up, with EPS estimated to grow by about 150% each year in the near future.

- Future Outlook: The company is also predicted to continue good expansion of its top line, with expected Revenue growth of 9.70% per year.

This mix of a confirmed revenue base and an anticipated rise in profitability forms the basic "growth" part that makes VRTX a fit for this strategy.

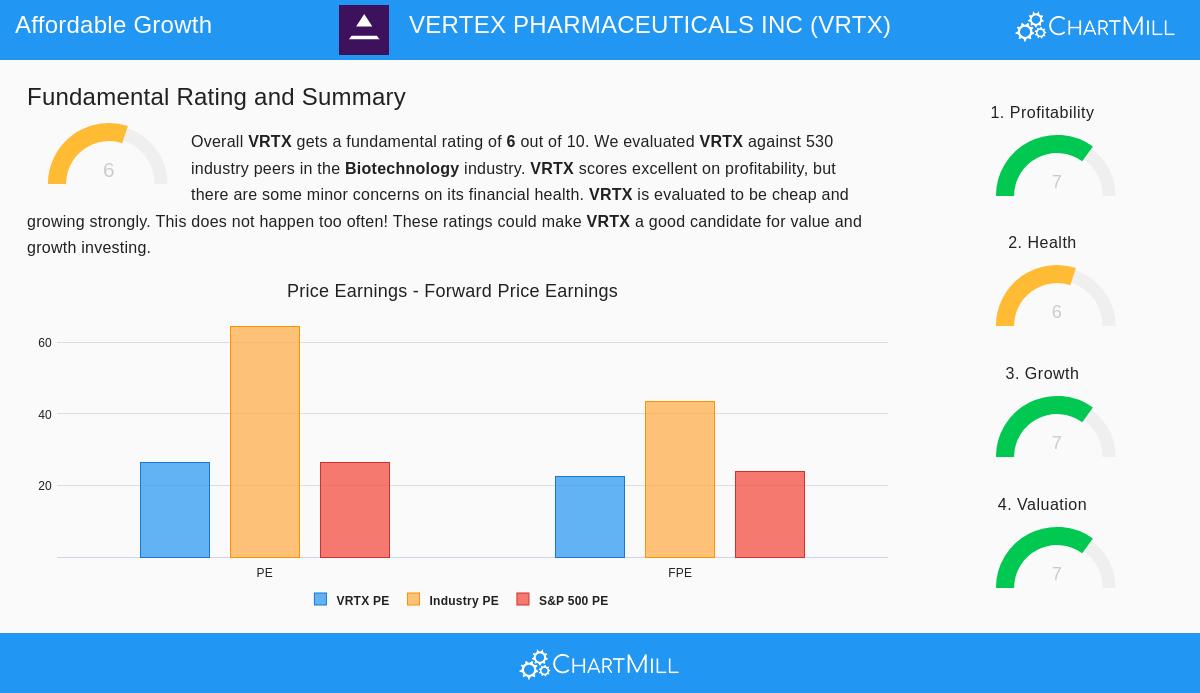

Valuation: The "Reasonable Price" Test

Finding growth is only part of the process, making sure you do not pay too much for it is what shapes the GARP method. Vertex’s ChartMill Valuation Rating of 7 implies the market may be pricing this growth at an appealing level, particularly compared to its industry.

- Sector-Relative Value: Compared to other biotechnology companies, VRTX seems noticeably low in price. Its Price/Earnings (P/E) ratio is lower than 93% of the industry, and similar benefits are visible in its Price/Forward Earnings and Enterprise Value/EBITDA ratios.

- Growth Adjustment: The Price/Earnings to Growth (PEG) ratio, which modifies the P/E for predicted growth rates, shows a fairly low price. This measure is key to GARP investing, as it directly connects what you pay to the growth you anticipate getting.

- Market Comparison: On a general level, VRTX’s P/E ratio of 26.28 is approximately equal to the wider S&P 500 average. Considering its better growth profile and industry standing, this similarity to the market multiple could be viewed as a sign of value.

For a strategy based on affordable growth, these valuation measures are positive. They suggest investors are not required to pay a high price common to very speculative biotech companies, but instead are getting high growth at a multiple similar to the overall market.

Supporting Fundamentals: Health and Profitability

A growth story based on weak finances is risky. The Affordable Growth screen needs acceptable scores in Financial Health and Profitability to confirm the company has the stability and operational quality to maintain its growth. Vertex scores well here, with ratings of 6 and 7, in order.

Financial Health (Rating: 6): The company’s balance sheet is a clear advantage. It has no debt, putting it in a strong position within its industry for financial soundness. This lack of debt gives great flexibility to fund research, manage development phases, or seek strategic options without financial pressure. A small point is that its liquidity ratios (Current and Quick Ratio), while sufficient, are not as high as many industry competitors.

Profitability (Rating: 7): Vertex runs with very high efficiency. Its margins are some of the best in the biotechnology sector:

- An Operating Margin of 38.70% is higher than almost 98% of its peers.

- A Profit Margin of 31.35% and a Return on Invested Capital (ROIC) of 17.58% also sit in the top group of the industry.

These strong profitability numbers are important. They show that the company’s growth is turning into real, high-margin earnings, which supports the valuation and supplies money to fund future growth, a positive cycle for any business.

Conclusion

Vertex Pharmaceuticals displays a profile that matches the goals of a Growth at a Reasonable Price strategy. It is a company with a clear record of revenue growth and a predicted large rise in earnings, meeting the basic "growth" need. Significantly, this growth is offered at a price that is attractive compared to its own industry and similar to the broader market, meeting the "reasonable price" condition. This possibility is supported by a very strong, debt-free balance sheet and top-tier profitability margins, which lower fundamental risk and confirm the quality of the earnings.

For investors wanting to review other companies that match this Affordable Growth model, more results from this screening method can be seen via this link.

A complete look at the fundamental analysis for Vertex Pharmaceuticals is provided in its full fundamental report.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation to buy or sell any security, or an endorsement of any investment strategy. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions.