In the hunt for investment chances, many experienced investors look to the ideas of value investing. This method, made famous by Benjamin Graham and Warren Buffett, centers on finding companies selling for less than their true worth. The aim is to locate good businesses that the market has incorrectly priced for now, providing a possible "margin of safety" for the patient investor. One useful way to use this thinking is by searching for stocks that show good fundamental condition and earnings but are offered at a lower price, hinting they could be priced too low. This method removes risky guesses and concentrates on financially stable companies whose present share price may not show their real business quality.

Universal Health Services, Inc. (NYSE:UHS) recently appeared from such a search process. As a top operator of acute care and behavioral health facilities in the United States and the U.K., the company is a major participant in the necessary healthcare services field. For value investors, the important question is if the market is correctly valuing its consistent cash flows and operational size.

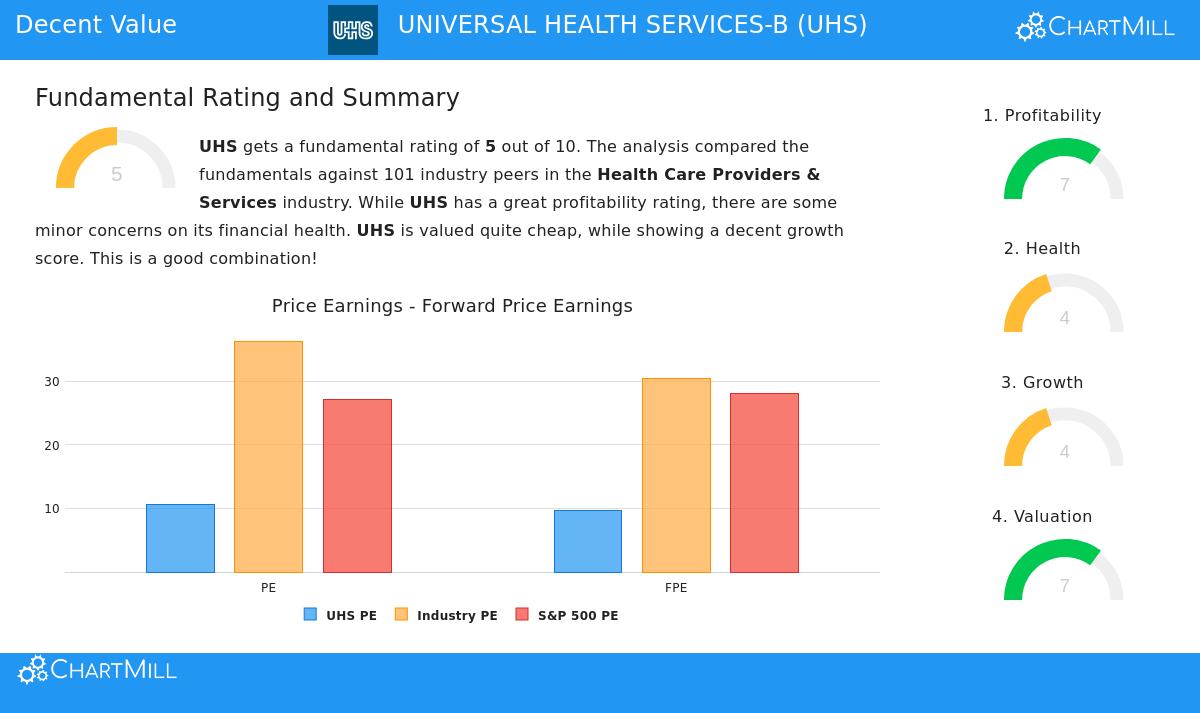

Valuation Measures: The Heart of the Value Case

The strongest point for UHS as a possible value stock is found in its valuation measures. A value investor's main job is to find a notable difference between price and estimated value, and UHS's present trading multiples hint this difference could be present.

- Price-to-Earnings (P/E): UHS trades at a P/E ratio of 10.60, which is seen as very moderate. This is much lower than the S&P 500 average of about 27.05.

- Industry Comparison: The valuation seems even more appealing next to its competitors. UHS is less expensive than 90% of the companies in the Health Care Providers & Services industry based on its P/E ratio.

- Forward-Looking Measures: The view stays the same when looking forward. The company's Price/Forward Earnings ratio of 9.71 is also below both the industry and wider market averages, showing the lower price isn't based only on past results.

For an investor using a value method, these ratios are the first step. They show the market is paying a fairly small price for each dollar of UHS's earnings compared to both the whole market and its direct rivals, meeting the basic value investing rule of looking for a low price.

Financial Condition and Earnings: Checking for a Solid Base

A low stock price is only a chance if the company is fundamentally healthy. A deep value discount can sometimes be a "value trap" if the business is declining. So, checking financial condition and earnings is essential. UHS's report shows a strong, profitable business.

Earnings are a clear positive, with a ChartMill rating of 7 out of 10. The company shows very good returns on its assets and invested money, doing better than most of its industry peers. Its profit margin of 8.09% is near the best in the field. This steady earnings record is key for value investors, as it hints the business has a lasting competitive edge and can increase its true worth over years.

Financial Condition gets a middle rating of 5, pointing to a steady but not outstanding position. The company has a workable debt level, with a Debt-to-Equity ratio that is higher than 61% of its industry. Its Altman-Z score suggests a low short-term chance of financial trouble. Still, investors should see the company's liquidity ratios (Current and Quick Ratio) are weaker compared to peers, a small concern that needs watching. For a value investor, a sufficient condition score confirms the company is not in immediate trouble, allowing time for the market to see its true worth.

Growth Outlook: The Driver for Future Worth

While strict value investing often looks at present assets and earnings, current views also think about a company's ability to expand. Lasting growth can be the reason that narrows the difference between market price and true value. UHS shows a varied but acceptable growth report, with a ChartMill Growth rating of 4.

The company has shown good past growth in Earnings Per Share (EPS), with a 30.77% rise over the last year. Looking forward, analysts predict a solid EPS growth rate of about 10.25% each year. Revenue growth predictions are more humble, forecast near 3.5% per year. This mix of good earnings with steady, expected growth in a necessary field fits well with a value-focused method that looks for reliable increase instead of risky fast growth.

Final Thoughts and Next Steps

Universal Health Services shows an example of a possible value investment. It trades at a notable discount to the market and its industry based on normal earnings multiples, the first test for a value filter. This discount is given to a company that shows good earnings and acceptable financial condition, lowering the chance of a value trap. Its steady, though not amazing, growth view in the durable healthcare field offers a believable way for the market to revalue the stock with time.

A complete look at these fundamental ratings is in the full ChartMill Fundamental Analysis Report for UHS.

For investors wanting to use this "reasonable value" way to find similar chances, the filter that found UHS can be a helpful beginning. You can find more stocks that fit these needs of good valuation with acceptable fundamentals by looking at this set filter.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. The study uses current information and has inherent unknowns. Investors should do their own complete research and think about their personal money situation and risk comfort before making any investment choices.