For investors looking for a systematic, long-term way to build wealth, few strategies are as respected as Peter Lynch’s method. As the famous manager of the Fidelity Magellan Fund, Lynch supported a philosophy of putting money into familiar companies, concentrating on businesses with durable growth, good financial condition, and fair prices. His method, often called Growth at a Reasonable Price (GARP), stays away from speculative trends for basic soundness. It includes looking for businesses with steady, not extreme, earnings increases, good profit levels, acceptable debt, and a stock price that is not too high for future potential. This systematic process tries to find companies set for lasting achievement, not temporary market changes.

One company that recently appeared from such a process is Trip.com Group Ltd.,ADR (NASDAQ:TCOM), a top global travel service platform. The company, which runs brands including Ctrip, Qunar, Trip.com, and Skyscanner, links travelers with a full set of booking services. Let's review how TCOM matches the main parts of a Lynch-type investment.

Match with Peter Lynch Standards

The center of Lynch's strategy involves particular, measurable filters to find good growth at a fair price. Trip.com Group seems to fit a number of these important measures:

- Durable Earnings Growth: Lynch wanted companies with a confirmed history of growth, but he was cautious of rates that were too high to continue. The process needs a 5-year average EPS growth between 15% and 30%. TCOM's EPS has increased at an average yearly rate of 21.05% over the last five years, well inside this range. This shows a firm, regular rise in profit without entering the area of extreme growth that is hard to keep.

- Fair Valuation (PEG Ratio): Maybe the most important Lynch measure is the Price/Earnings to Growth (PEG) ratio, which tries to find stocks that might be priced low compared to their growth rate. A PEG ratio at or under 1.0 is seen as good. TCOM does well here, with a PEG ratio of 0.50. This low number implies the market may not completely account for the company's past growth path, a clear sign Lynch searched for.

- Good Profit Level (ROE): Lynch liked companies that effectively create profits from shareholder equity. A Return on Equity (ROE) above 15% is a key process filter. TCOM's ROE is 18.53%, showing its capacity to give acceptable returns on the money put into the business.

- Financial Condition (Debt & Liquidity): A careful balance sheet is essential for getting through economic changes. Lynch chose companies with a Debt/Equity ratio below 0.6 (and preferably below 0.25). TCOM is very sound here, with an extremely low D/E ratio of 0.07, showing very little dependence on debt funding. Also, its Current Ratio of 1.48 indicates sufficient cash to meet near-term needs, passing another of Lynch's basic condition tests.

Basic Condition Review

A wider view of Trip.com Group's basic profile, as described in its detailed analysis report, gives a detailed view that mainly agrees with the process findings.

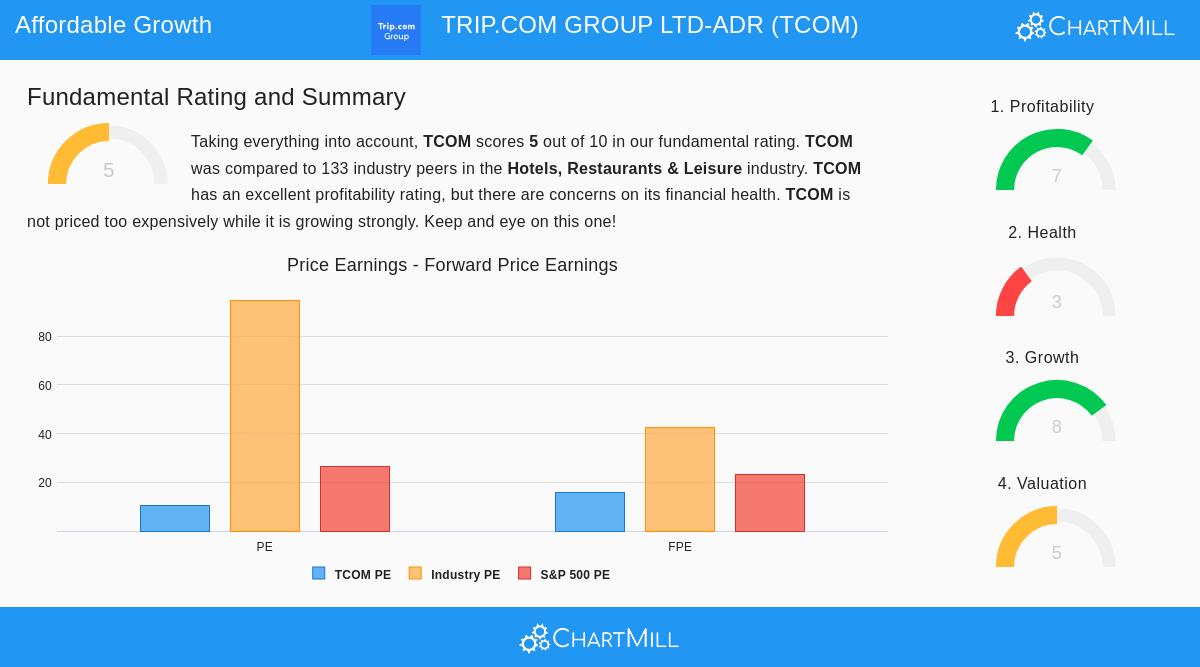

The company gets high scores for profit and growth. Its profit margin above 52% is outstanding within the competitive travel field, and both sales and earnings have shown firm past growth, with good forecasts for coming years. From a valuation angle, its standard P/E ratio of 10.5 is viewed as fair and stacks up well against both industry competitors and the wider S&P 500.

However, the report does note some items for review. While the balance sheet is firm on debt level (very low debt), the overall financial condition score is moderated by comments on share count increase over recent years and a Return on Invested Capital (ROIC) that, while getting better, has in the past been below the industry average. The dividend payment is also very small, which is common for a company probably putting much money back into growth.

Investment Case for the Long-Term Investor

For an investor using a Peter Lynch view, Trip.com Group offers a strong argument. It works in the large, lasting travel industry—a "simple" need instead of a passing trend. The company has used its size in important markets like China to create a strong platform, a standard example of a business one might see and know in daily life. The numerical process results meet the main areas Lynch highlighted: durable past growth, high profit, excellent debt control, and a price that seems to undervalue that growth.

The basic analysis indicates this is not a perfect company, with some effectiveness measures and share handling practices deserving continued attention. Still, the central investment idea—a profitable, expanding leader in a necessary worldwide industry, available at a fair price—matches closely with the ideas of searching for long-term growth at a reasonable price.

Interested in locating other companies that fit this systematic method? You can view the active Peter Lynch strategy process here.

Disclaimer: This article is for information only and is not financial guidance, a suggestion, or an offer to purchase or sell any security. The review is based on data and a particular investment strategy model; individual investors should do their own complete study and think about their private financial position before making any investment choices.