The search for quality companies trading at reasonable prices is a central part of many long-term investment methods. One well-regarded method is the strategy made famous by Peter Lynch, who found great results by concentrating on expanding, profitable businesses with sound finances and clear operations, all bought at a fair price. This "growth at a reasonable price" (GARP) thinking steers clear of the limits of pursuing high-risk growth or deeply discounted troubled companies, looking instead for businesses with lasting compounding potential. A recent filter using Lynch's main requirements has identified one such possibility in the travel industry: Trip.com Group Ltd-ADR (NASDAQ:TCOM).

Fit with Peter Lynch's Main Ideas

Lynch's system focuses on a number of numerical filters to find candidates that deserve more study. Trip.com seems to satisfy these basic checks, which are made to locate sound companies with lasting growth trading at a appealing price compared to that growth.

- Lasting Earnings Expansion: Lynch preferred companies with a solid but not extreme growth path, usually looking for an EPS growth rate between 15% and 30% over five years. Trip.com's five-year EPS growth rate of 21.05% falls within this desired range, pointing to a solid and possibly sustainable speed of increase.

- Appealing Price via PEG Ratio: A key part of the strategy is the Price/Earnings to Growth (PEG) ratio, which tries to find stocks where the price is not exceeding the growth rate. A PEG ratio at or under 1 is seen as appealing. Trip.com's PEG ratio, calculated from its past five-year growth, is about 0.49, suggesting the market may be pricing it below its historical growth record.

- Sound Profitability (ROE): Return on Equity (ROE) shows how well a company creates profits from shareholder equity. Lynch wanted an ROE above 15%. Trip.com's ROE of 18.53% is above this level, indicating efficient management and a profitable operation.

- Cautious Financial Condition: To steer clear of companies with too much debt, Lynch stressed a low Debt-to-Equity ratio, with a liking for numbers below 0.25. Trip.com's ratio of 0.07 shows a very cautious balance sheet, financed almost completely by equity instead of debt. This gives notable strength in unpredictable economic times.

- Sufficient Short-Term Cash Flow: The Current Ratio, which measures a company's capacity to pay short-term debts, must be at least 1. Trip.com's ratio of 1.48 indicates it has more than enough short-term assets to cover its short-term debts, a sign of steady operations.

Basic Condition and Growth Picture

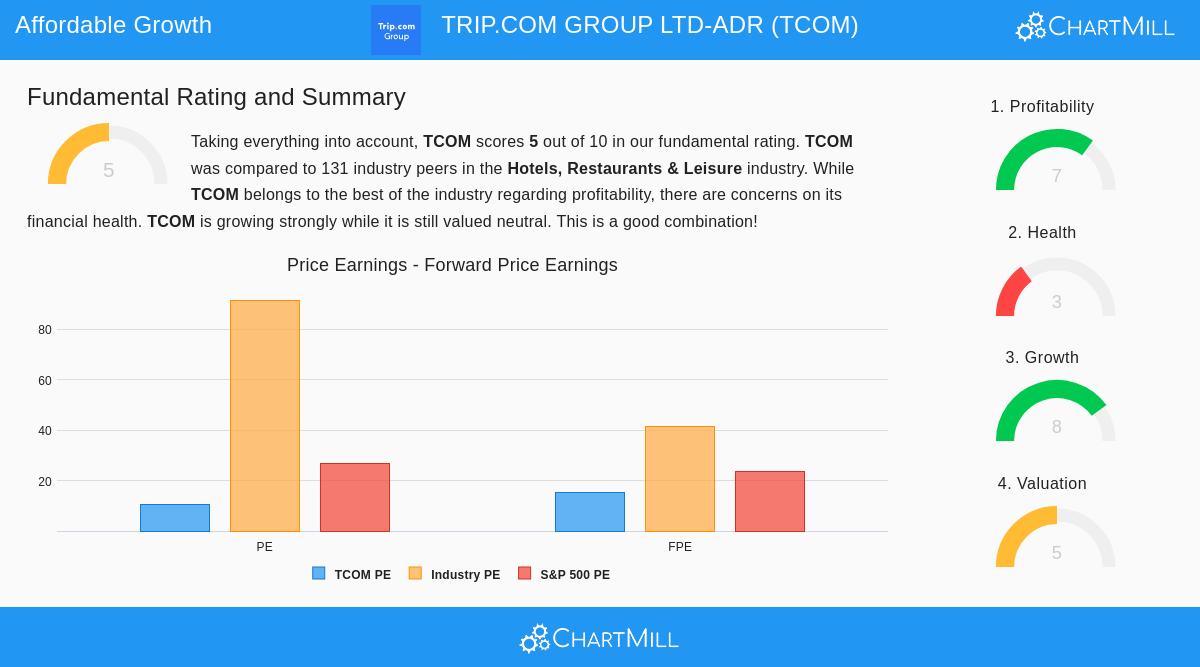

A wider view of Trip.com's basic report shows a varied but mostly favorable image that fits a GARP investment idea. The company receives an overall basic rating of 5 out of 10, showing a middle position within its field, but the parts underneath present a more detailed story.

Positive Points:

- Excellent Profitability Margins: The company has exceptional margin measures, including a Profit Margin over 52% and an Operating Margin of 26%, placing it close to the highest in the Hotels, Restaurants & Leisure industry.

- Solid Growth Path: Both past and predicted future growth are strong. Revenue has increased at an average of 8.36% per year over recent years and is forecast to rise to over 13% in the next few years. EPS growth has been even more notable.

- Fair Pricing: In spite of its growth, the stock sells at a P/E ratio of 10.40, which is viewed as fair in general and is less expensive than almost 90% of similar companies in its industry.

Points to Note:

- Basic Condition Questions: The overall condition score is a middle 3. While the balance sheet is cautiously leveraged (a good point), the report mentions points like a recent rise in shares outstanding and a Return on Invested Capital (ROIC) that has in the past been below its cost of capital.

- Small Dividend: The company is not a major source of income, with a dividend yield of 0.42%.

For a complete look at these measures, you can see the full basic examination report for TCOM.

Investment Case for the Long-Term Holder

For an investor using a Peter Lynch-type GARP method, Trip.com makes a strong argument. It works in the large and lasting travel industry, a field most customers grasp easily. The company has shown it can increase earnings at a good, double-digit rate while keeping top-level profitability margins. Importantly, this growth is not being bought at a high price; the low PEG and P/E ratios imply the market is valuing the stock cautiously. The very strong balance sheet with little debt offers a notable buffer, a main factor for long-term owners who must endure industry ups and downs.

The questions noted, especially about capital efficiency (ROIC), are relevant for more detailed study. A long-term investor would need to evaluate if the company's spending is starting to produce better returns, as hinted by the upward move in its most recent ROIC number.

Looking for More Possibilities

Trip.com is one of a few companies that currently meet the filter based on Peter Lynch's strict requirements. Investors curious about finding other possible "growth at a reasonable price" choices can view the full list of results using the Peter Lynch Strategy stock filter.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. The examination uses public data and a particular investment strategy filter. Investors should do their own complete research and think about their personal financial situation and risk comfort before making any investment choices.