In the search for long-term investment opportunities, many investors turn to the principles of legendary fund manager Peter Lynch. His strategy, often categorized as Growth at a Reasonable Price (GARP), focuses on finding profitable companies with sustainable growth paths that are trading at appealing valuations. The central idea is to avoid overpaying for excitement while still capturing the compounding returns of a good business. A key tool for using this method is a stock screener that filters for specific financial health, profitability, and valuation measures.

One name that recently appeared from such a Peter Lynch-inspired screen is QFIN Holdings Inc-ADR (NASDAQ:QFIN), a Chinese company providing credit technology services. This financial technology firm works by connecting borrowers with financial institutions and offering a group of platform-based services, placing itself within the developing digital finance environment in China.

Alignment with Peter Lynch's Core Criteria

A Peter Lynch screen usually looks for a balanced mix of growth, value, and financial strength. Based on the provided data, QFIN seems to meet several of these important points.

- Sustainable Earnings Growth: Lynch preferred companies increasing steadily, not suddenly. QFIN's five-year average earnings per share (EPS) growth of 19.96% sits comfortably within the often-cited Lynch range of 15% to 30%. This shows a history of strong, yet possibly sustainable, expansion without the warning sign of very fast growth that can be hard to continue.

- Appealing Valuation Relative to Growth: Maybe the most important Lynch measure is the Price/Earnings to Growth (PEG) ratio, which tries to find value by including a company's growth rate. A PEG ratio at or below 1.0 is seen as appealing. QFIN's PEG ratio, based on its past five-year growth, is very low at about 0.10. This implies the market is pricing the company's shares at a large discount to its historical growth record, a key sign for value-aware growth investors.

- Strong Profitability: Lynch searched for companies that are good at creating profits from shareholder equity. QFIN's Return on Equity (ROE) of 30.15% is unusually high, much better than a typical Lynch limit of 15%. This shows management is very good at using invested money to produce earnings.

- Good Financial Health: To make sure of lasting power, Lynch stressed companies with strong balance sheets. QFIN shows strength here with a Debt-to-Equity ratio of 0.26, which is well under a conservative goal of 0.6 and even matches Lynch's stricter liking for a ratio under 0.25. Also, its Current Ratio of 3.48 shows enough cash to cover near-term bills, giving a cushion against economic shifts.

Fundamental Health Overview

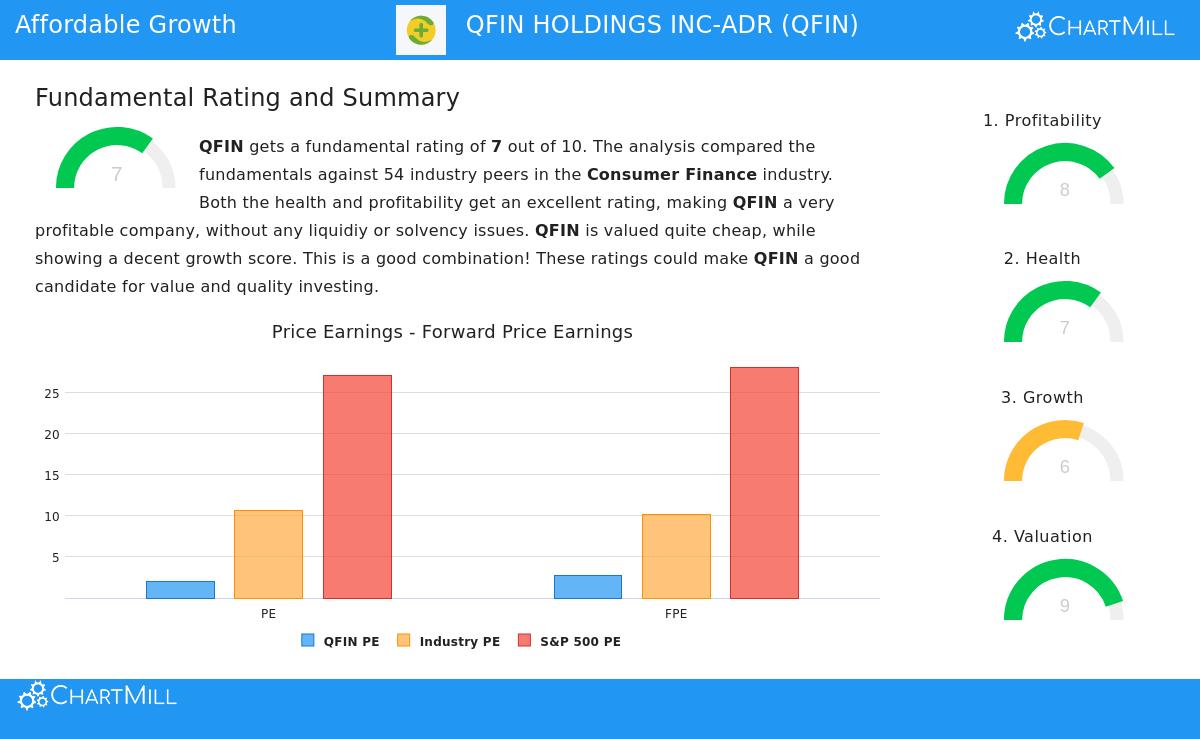

A wider look at QFIN's fundamental profile supports the picture shown by the specific Lynch points. The company gets a good overall fundamental rating, with specific strong points in profitability and valuation. Its profit margins are some of the best in its field, and it creates large returns on both assets and invested money. From a valuation view, its standard Price-to-Earnings (P/E) ratio is also very low compared to both industry peers and the wider S&P 500, suggesting the stock is priced carefully.

However, investors should note areas marked for more study. While past growth has been good, analyst forecasts for near-term EPS growth have slowed noticeably. Also, the company's high dividend yield, while appealing, has been affected by a recent drop in share price and a recent dividend reduction, needing a closer examination of dividend continuity. A full breakdown of these strong points and factors can be seen in the full fundamental analysis report.

Conclusion

For investors using a GARP or Peter Lynch-style strategy, QFIN offers an interesting case study. It shows the signs of a possibly fitting candidate: a history of good, steady earnings growth, first-rate profitability measures, a very strong balance sheet with little debt, and a valuation that seems deeply reduced relative to its historical record. The low PEG ratio is a notable feature, directly speaking to Lynch's rule of looking for growth at a sensible price.

Of course, no screen replaces complete individual research. The company's connection to the Chinese consumer finance field and the noted reduction in expected earnings growth are important factors for any investor to study carefully before making a choice. The Lynch method finally depends on knowing the business behind the numbers.

Interested in finding other companies that match this disciplined investment method? You can run the same Peter Lynch strategy screen here to look at more possible opportunities.

,

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. The analysis is based on data provided and certain investment methodologies, which carry inherent limitations. Investors should conduct their own independent research and consider their individual financial circumstances and risk tolerance before making any investment decisions.