The investment philosophy of legendary fund manager Peter Lynch, as detailed in his book One Up on Wall Street, focuses on finding well-run, growing companies trading at reasonable prices. Often called a Growth at a Reasonable Price (GARP) method, Lynch’s strategy does not favor speculative high-flyers but instead looks for businesses with sustainable, understandable growth, strong financial health, and attractive valuations. Investors using this approach usually look for companies with consistent earnings growth, high profitability, manageable debt, and a price that does not overstate future prospects. One stock that recently appeared from such a search is QFIN Holdings Inc-ADR (NASDAQ:QFIN).

A Closer Look at the Business

Headquartered in Shanghai, QFIN Holdings Inc operates in the consumer finance sector, providing credit technology services in China. The company’s business is split into credit-driven services, where it connects borrowers with financial institutions, and capital-light platform services, which include loan assistance, marketing, and risk management software. This place in China's large fintech field allows it to use technology to enable credit, a basic and repeating need in any big economy.

Alignment with Peter Lynch's Core Criteria

A Peter Lynch-inspired search looks for companies that show a specific mix of growth, value, and financial strength. QFIN seems to meet several of these important measures, which are made to find sustainable compounders for a long-term portfolio.

- Sustainable Earnings Growth: Lynch preferred companies growing earnings per share (EPS) between 15% and 30% each year, seeing this range as sustainable. QFIN’s five-year average EPS growth rate of 19.96% fits directly within this target area, showing a history of solid, but not excessive, expansion.

- Attractive Valuation Relative to Growth: Maybe the most important Lynch measure is the Price/Earnings to Growth (PEG) ratio, which tries to find stocks where the price fairly shows the growth rate. A PEG ratio at or below 1.0 is usually seen as attractive. QFIN’s PEG ratio, based on its past five-year growth, is very low at about 0.13, implying the market is pricing its shares at a large discount to its historical growth path.

- Strong Profitability: Lynch searched for companies that efficiently create profits from shareholder equity. A Return on Equity (ROE) above 15% is a common limit. QFIN’s ROE of 30.15% is excellent, showing better profitability and efficient use of capital than most industry peers.

- Conservative Financial Health: To make sure of resilience, Lynch liked companies with strong balance sheets. His searches often use a Debt-to-Equity ratio below 0.6, with a personal liking for numbers under 0.25. QFIN’s ratio of 0.26 shows a conservative capital structure, depending more on equity than debt. Also, its Current Ratio of 3.48 indicates more than enough liquidity to cover short-term obligations, well above the minimum need of 1.0.

Fundamental Health Check: Beyond the Search

While a search gives an efficient starting point, Lynch stressed the need for deeper study. A review of QFIN’s detailed fundamental analysis report shows a profile that mostly supports the search results.

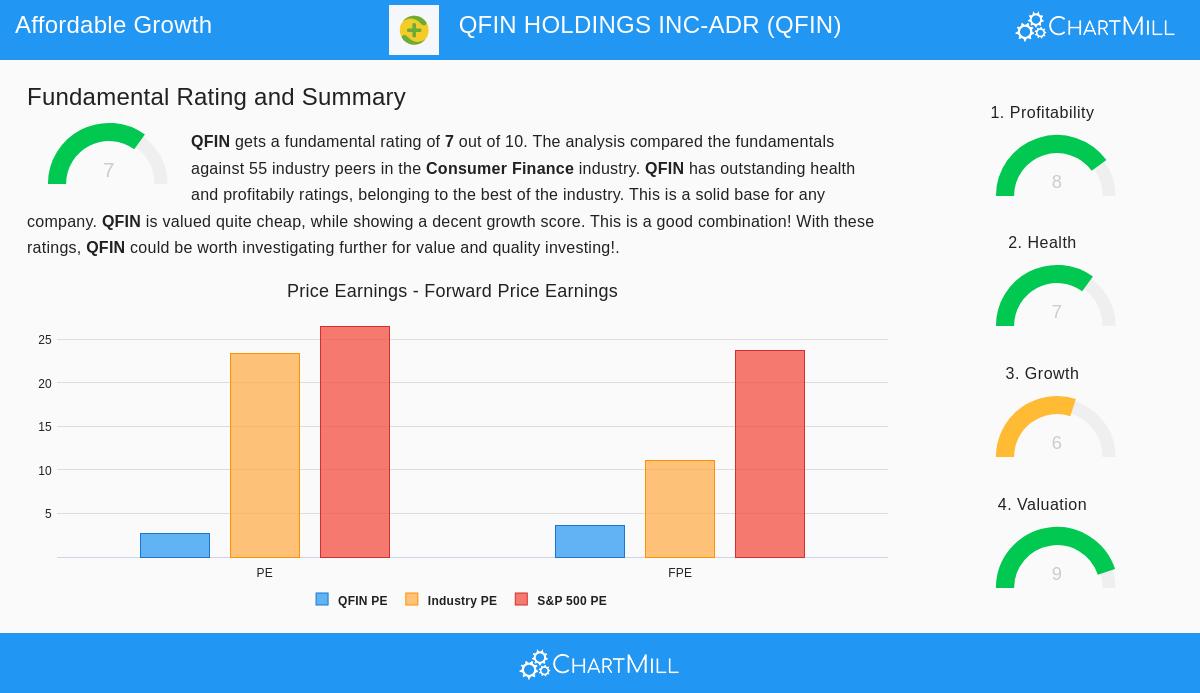

The company gets a high overall fundamental score of 7 out of 10. Its notable features are excellent profitability and very low valuation. Margins are industry-leading, with a Profit Margin of 38.67% and an Operating Margin of 44.19%. On valuation, its standard Price-to-Earnings (P/E) ratio of 2.65 and forward P/E of 3.58 are not only far below the S&P 500 average but also lower than over 90% of its consumer finance industry peers.

The financial health picture is also strong, backed by the low debt levels and high liquidity seen in the search. It should be noted, however, that growth expectations have slowed. While past revenue and EPS growth have been notable, analyst forecasts point to a more moderate growth path ahead, which is an important factor for investors to study more.

Is QFIN a Lynch-Style Opportunity?

For investors following a GARP or Peter Lynch method, QFIN makes a strong case for more study. It meets the main points of the strategy: a history of solid earnings growth within a sustainable range, an exceptionally low valuation when growth is considered, high profitability, and a very strong balance sheet. The company works in the essential area of credit technology, a business model that, while facing regulatory cycles, is fundamentally understandable.

The large discount in its valuation measures, together with its high profitability, implies the market may be missing its quality or using a heavy discount because of its Chinese location or sector-specific worries. This possible gap between business performance and market price is exactly the kind of situation long-term, fundamentals-focused investors look for.

Finding More Candidates

QFIN is just one example of a company that passes a strict set of investment filters. Investors searching for other possible ideas based on the Peter Lynch strategy can review the full search and its current results here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. Readers should conduct their own thorough research and consider their individual financial circumstances and risk tolerance before making any investment decisions.