A fundamental investment approach made famous by legendary investor Peter Lynch focuses on finding companies with lasting growth paths trading at sensible prices. This strategy, often called Growth at a Reasonable Price (GARP), aims to avoid both overpriced growth stocks and stagnant value investments by focusing on businesses with good profitability, sound financial condition, and earnings growth that is faster than their valuation multiples. The method highlights companies expanding at a maintainable speed rather than very fast but possibly unreliable growth rates.

Financial Health and Profitability

QFIN HOLDINGS INC-ADR (NASDAQ:QFIN) shows very good financial traits that match Lynch's focus on company strength and operational effectiveness. The Chinese consumer finance technology company displays strong profitability measures and balance sheet soundness that position it with the leading performers in its field.

- Return on Equity of 30.15% is much higher than Lynch's 15% target

- Current Ratio of 3.48 shows good short-term liquidity

- Debt-to-Equity ratio of 0.26 is much lower than Lynch's preferred maximum of 0.6

- Operating Margin of 44.19% is in the top 5% of industry peers

These measures reflect Lynch's focus on companies with solid competitive positions and effective capital use. The high ROE indicates management is using shareholder capital well, while the low debt levels and good liquidity offer financial steadiness during economic slowdowns.

Sustainable Growth Profile

The company's growth path matches Lynch's liking for maintainable rather than very fast expansion. QFIN has shown steady earnings growth while keeping sensible valuation multiples.

- 5-year EPS growth rate of 19.96% is within Lynch's target range of 15-30%

- Revenue has increased at an average yearly rate of 13.24% over recent years

- Forward EPS growth expectations of 16.80% point to continued momentum

- PEG ratio of 0.18 shows significant growth compensation in the current price

Lynch specifically looked for companies expanding at maintainable rates, stating that extremely high growth often does not last. QFIN's steady mid-teens growth, paired with its solid market position in Chinese consumer finance, indicates the company can continue this path without the operational pressures that often come with very fast growth.

Notable Valuation Metrics

Maybe the most noticeable part of QFIN's investment case is its price relative to growth and profitability. The company trades at multiples that seem separated from its fundamental performance.

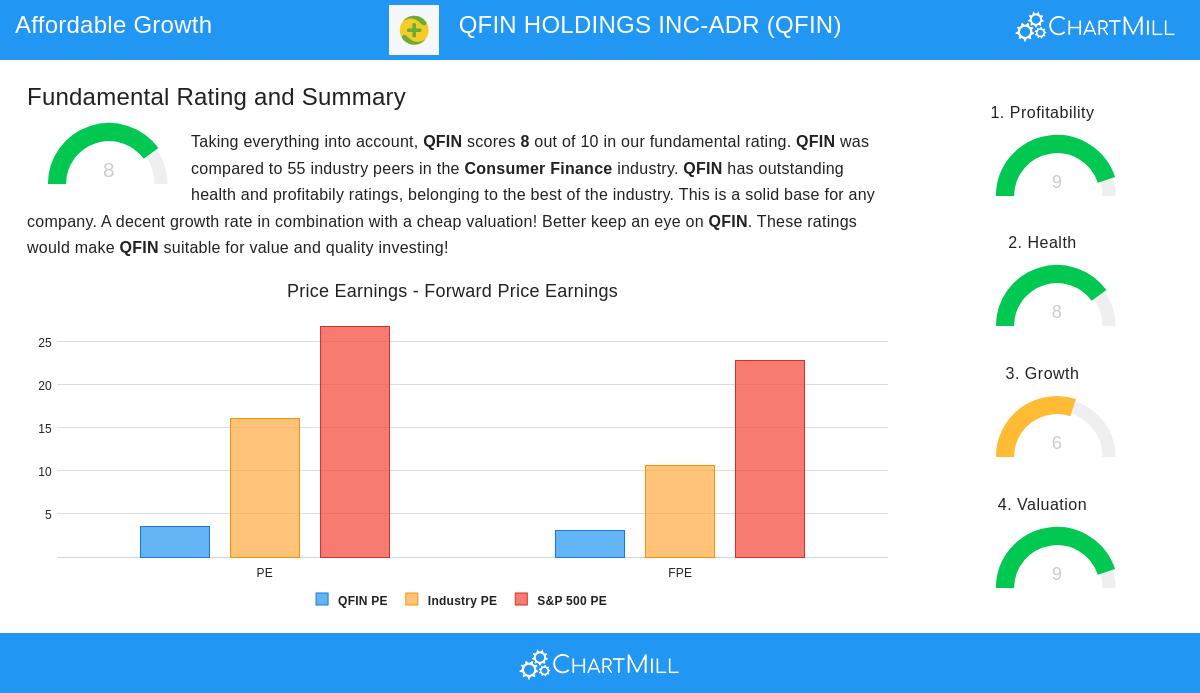

- P/E ratio of 3.55 represents a large discount to industry and market averages

- Price/Forward Earnings ratio of 3.14 suggests continued low valuation

- Enterprise Value/EBITDA multiple is lower than 87% of industry peers

- Dividend yield of 5.69% provides income while waiting for price recognition

Lynch's strategy heavily highlighted the PEG ratio as a key valuation tool, with values under 1.0 pointing to possible low valuation. QFIN's very low PEG ratio of 0.18 indicates the market is pricing in little future growth despite the company's shown expansion abilities.

Fundamental Analysis Overview

According to Chartmill's detailed fundamental analysis report, QFIN gets an overall rating of 8 out of 10, with especially high scores in profitability (9/10) and valuation (9/10). The report points out that the company "has outstanding health and profitability ratings, belonging to the best of the industry" while being "valued quite cheap." This mix of quality operations and low price creates what Lynch often described as the ideal investment situation - a sound company available at a good price.

The analysis mentions QFIN's very good performance across several profitability measures, with ROE, ROIC, and profit margins all in the top group of the consumer finance industry. At the same time, the valuation metrics suggest the market has greatly underappreciated these operational strengths, possibly because of wider worries about Chinese stocks rather than company-specific issues.

Investment Considerations

While QFIN appears to meet many of Lynch's standards for long-term investment, potential investors should think about several factors. The company works in China's regulated financial sector, which brings geopolitical and regulatory considerations. Also, the recent 25% price drop, while making valuation measures better, may reflect shifting market feeling toward Chinese stocks broadly.

The company's share buyback program and reasonable institutional ownership match additional factors Lynch viewed as positive. However, as with any international investment, currency risk and different accounting standards need careful thought.

For investors interested in looking at other companies that meet Peter Lynch's investment standards, more screening results are available through our Peter Lynch Strategy Screener.

,

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any securities. Investors should conduct their own research and consult with a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.