The search for undervalued stocks is a foundation of value investing, a method that aims to find companies priced below their real worth. This method, established by Benjamin Graham and notably used by Warren Buffett, depends on fundamental analysis to find differences between a company's market price and its actual business value. One organized way to locate these chances is by filtering for stocks that show good valuation numbers, indicating they may be inexpensive, while still holding acceptable scores in other important areas like financial condition, earnings, and expansion. This mix is key; a low price by itself can be a "value trap" if the core business is declining. A stock that is inexpensive but also fundamentally good in several ways offers a stronger reason for more review.

PayPal Holdings Inc. (NASDAQ:PYPL), a top company in digital payments, recently appeared from such a filtering process. The company's fundamental report, which you can examine in detail here, shows a picture that matches the main ideas of a value-focused search: a very inexpensive valuation combined with acceptable scores in other fundamental groups.

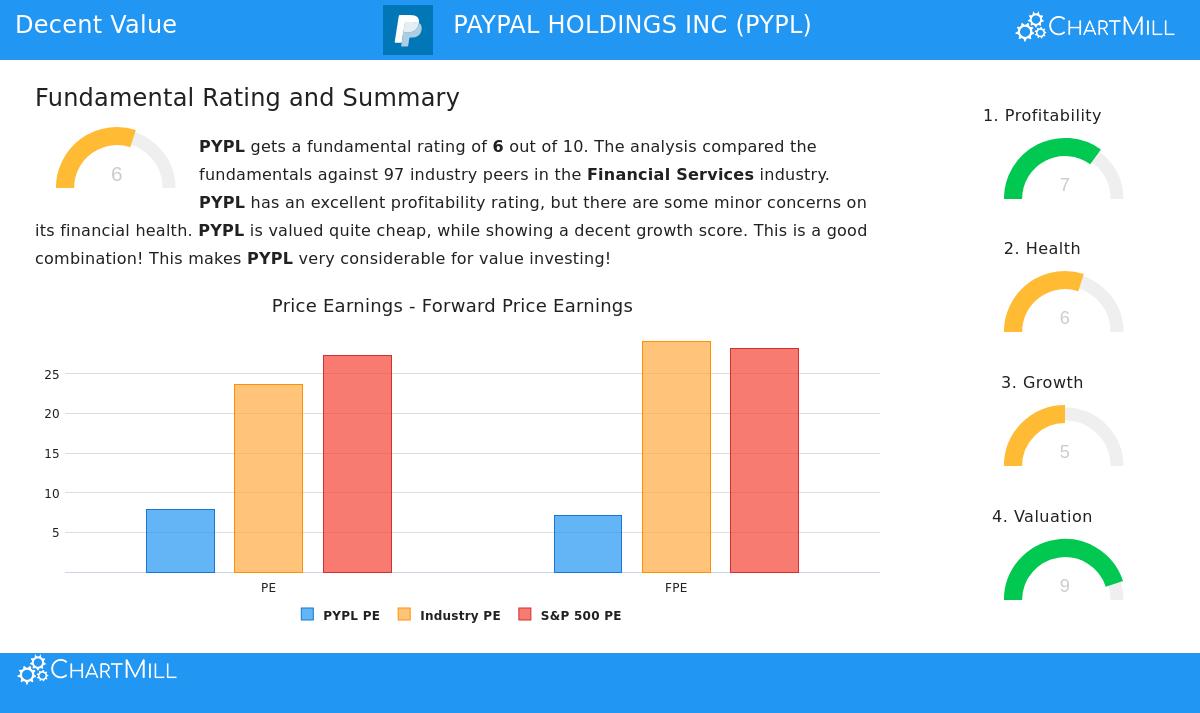

A Notable Valuation Picture

The most noticeable part of PayPal's current fundamental view is its valuation. In value investing, a low valuation is the main sign that a stock could be priced below its real value, offering a possible "margin of safety." PayPal's ChartMill Valuation Rating is a strong 9 out of 10, putting it with the most inexpensive stocks in its filtered group.

- Price-to-Earnings (P/E) Ratio: At 7.82, PayPal's P/E ratio is called "very cheap" in its report. This is much lower than both the industry average of about 23.6 and the wider S&P 500 average of 27.3.

- Forward P/E Ratio: Looking forward, the valuation stays attractive with a forward P/E of 7.06, which is more inexpensive than almost 80% of its industry group.

- Other Metrics: The good valuation is supported by other measures. The company's Enterprise Value to EBITDA and Price/Free Cash Flow ratios show it is more inexpensive than over 90% and 87% of industry rivals, in order.

For a value investor, these numbers imply the market may be using a large discount to PayPal's earnings and cash flow, possibly because of recent worries instead of a sign of its lasting business value.

Mixing Inexpensive Price with Fundamental Soundness

An inexpensive stock is only a good investment if the company is financially stable. A poor balance sheet or low earnings can change an apparent deal into a value trap. PayPal's report shows it keeps sufficient scores in these areas, which helps reduce that risk.

Financial Condition (Rating: 6/10) Financial condition is important for a value investment because it makes sure the company can survive economic drops and keep operating without trouble. PayPal's condition rating shows a steady, though not perfect, situation.

- Solvency: The company has a workable Debt/Equity ratio of 0.49 and a good Debt to Free Cash Flow ratio of 2.05, meaning it could pay off all debt with just over two years of cash flow. Its Altman-Z score, while in a "grey zone," is still higher than 74% of its group.

- Liquidity: Its Current and Quick Ratios (both 1.29) are enough to cover near-term debts and are higher than many industry rivals.

Earnings (Rating: 7/10) Steady earnings is a sign of a good business and supports the idea that current profits, which are the base of the inexpensive valuation, can continue.

- PayPal has been profitable with positive operating cash flow for the last five straight years.

- Its Return on Equity (25.83%) and Return on Invested Capital (15.26%) are especially good, doing better than over 90% of the industry. High returns on capital are a main sign of a company's competitive edge and efficient use of investor money.

Expansion as a Driver

While pure value stocks sometimes miss expansion, PayPal shows a steady but positive expansion path. This is significant because it offers a possible driver for the market to re-price the stock upward. Flat earnings in an inexpensive company might support the low price forever, but expansion can narrow the space between price and value.

- Past Expansion: Revenue has expanded at an average rate of 9.11% over the past five years, which the report calls "quite good."

- Future Predictions: Analysts estimate EPS to expand by an average of 12.78% each year in the coming years, pointing to a quickening from recent patterns.

Conclusion

PayPal offers a situation that fits a careful value investing structure. It is not only a numerically inexpensive stock; it is a financially stable and profitable market leader trading at a valuation that seems to lower its future chances greatly. The mix of a very low P/E ratio, good returns on capital, a firm balance sheet, and predicted earnings expansion creates a picture deserving of closer study for investors looking for undervalued chances. The market's current recent positive direction may offer a good setting, but the value idea depends on these lasting fundamentals.

This review of PayPal was found using a filtering method centered on valuation and fundamental soundness. If you want to look at other stocks that fit similar "acceptable value" rules, you can find more outcomes through this pre-set stock filter.

Disclaimer: This article is for information only and does not make up financial advice, a suggestion to buy or sell any security, or a support of any investment method. Investors should do their own study and think about their personal financial situation before making any investment choices.