For investors looking to balance the search for growth with fiscal care, the "Growth At a Reasonable Price" (GARP) method offers a practical middle path. This method looks for companies with good and lasting growth paths, but whose shares are not priced too high. It tries to avoid the high chance of paying too much for extreme growth while still taking part in a company's increase. One way to find these candidates is through a set search for "Affordable Growth," which selects for stocks with good growth scores, firm basic profit and money condition, and a price that does not seem too high.

Pinterest Inc - Class A (NYSE:PINS) recently came up from such a search, indicating its outline may fit this investment thinking. The company, a visual idea engine with over 550 million monthly active users, lets people find ideas and shop for goods. Its basic study report shows a combined score of 7 out of 10, showing force in several main areas important for a GARP review.

Growth Path: The Main Force

The base of any affordable growth idea is, expectedly, growth. Pinterest’s basics show a company in a good increase phase, getting a Growth score of 7. The company has shown an ability to grow its top line well while turning that into bottom-line gain.

- Good Revenue Increase: Revenue grew by 16.79% over the past year, and the longer-term yearly growth rate is a notable 26.12%. This shows a strong and kept upward path in its main business.

- Earnings Growth in Line: While past year Earnings Per Share (EPS) growth was a more moderate 5.63%, the longer-term yearly EPS growth rate is a firm 8.67%. More significantly, experts think this will speed up, with forward EPS growth planned at 10.58% each year.

- Positive Movement: The study notes that the EPS growth rate is speeding up when comparing past results to future guesses, a good sign for movement investors within the GARP structure.

This mix of good past revenue growth and expected speed-up in earnings growth is exactly what searches for "good growth" try to catch, as it suggests a business that is growing with profit.

Price: The "Reasonable Price" Test

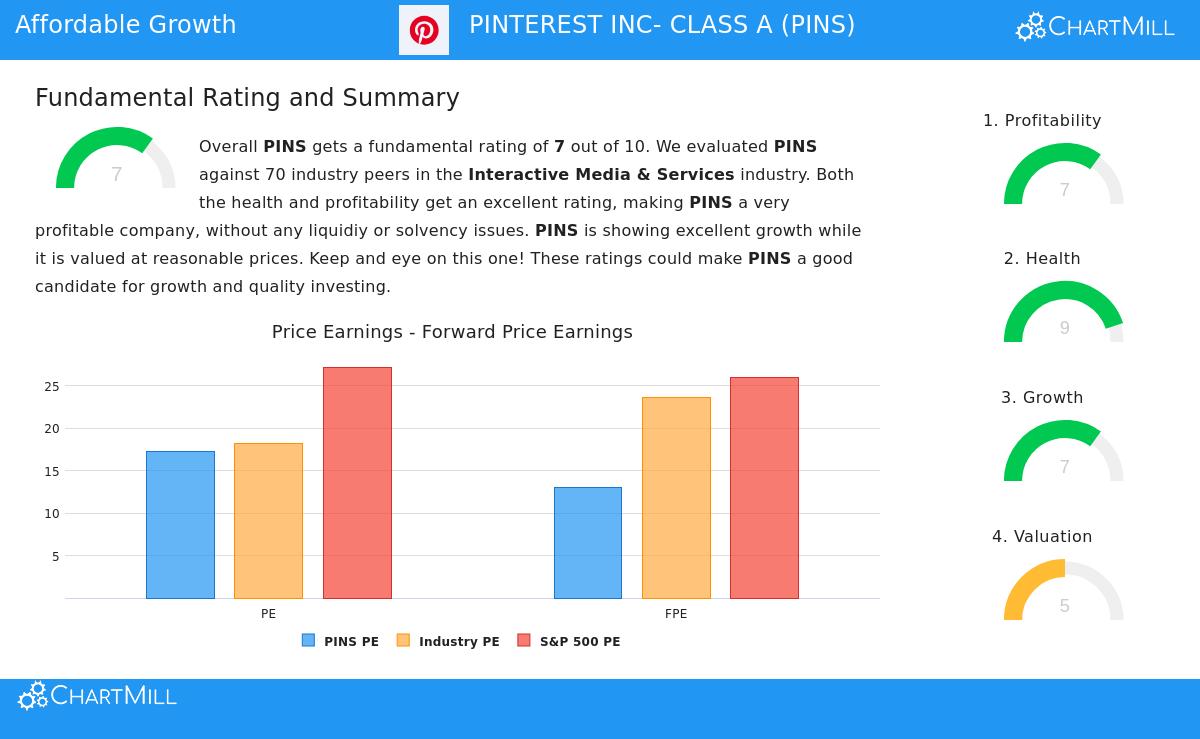

A stock with good growth can still be a bad investment if bought at a too high price. This is where the price test becomes most important. Pinterest gets a neutral Price score of 5, which, in the setting of a growth search, is okay—it shows the market has not priced the company as perfect.

- Good Relative Measures: With a Price-to-Earnings (P/E) ratio of 17.27, Pinterest is priced lower than 67% of similar companies in the Interactive Media & Services field. Its Forward P/E of 13.07 is also under the current S&P 500 average.

- Growth Adjustment: The PEG ratio, which changes the P/E for growth, shows a right price. The report clearly says the company's acceptable profit and expected earnings growth may support its current measure, stopping it from being called "overpriced."

- Cash Flow View: The Price-to-Free Cash Flow ratio also suggests a somewhat low price relative to the field, with Pinterest being lower than 74% of similar companies.

For an affordable growth plan, this price view is key. It suggests investors are not paying a guesswork extra but are instead getting growth possibility at a price that seems sensible relative to both the market and the company's own field.

Basic Money Force: Profit and Condition

Lasting growth cannot happen without a firm money base. Pinterest scores highly here, with very good scores for Money Condition (9) and Profit (7). These scores give trust that the growth is built on a steady base.

- Very Good Money Condition: The company has an Altman-Z score of 16.76, pointing to very low near-term failure risk and doing better than 93% of the field. Importantly, Pinterest has no debt and has a large current and quick ratio above 8, showing great cash to pay for operations and investments without strain.

- Good Profit Measures: The company turns revenue to profit well, with a Profit Margin of nearly 49%, better than 96% of similar companies. Its Return on Equity (41.19%) and Return on Assets (36.03%) are among the best in the field, showing effective use of owner money.

These parts are key for the affordable growth plan. Superior money condition lowers downside risk and gives a cushion during market drops, while high profit suggests the business model is firm and can pay for future growth from within.

End and More Study

Based on its basic report, Pinterest Inc shows an outline that fits the goals of an affordable growth investor. It shows a clear pattern of good revenue growth with speeding earnings expectations, trades at a price that is sensible relative to its field and growth outlook, and is held up by a very firm balance sheet and high profit. This mix of growth, price, and quality is the three-part goal that searches like the "Affordable Growth" filter are made to find.

It is significant to note that while the S&P 500's short-term direction is currently positive, the long-term direction stays neutral, highlighting the importance of stock-specific basics in the current setting.

For investors curious about looking at other companies that meet similar rules of good growth, sensible price, and acceptable money force, more results can be found by checking the Affordable Growth stock search.

Disclaimer: This article is for information only and does not make up money advice, a suggestion, or an offer or request to buy or sell any securities. The study is based on basic data and scores given by ChartMill.com. Investors should do their own study and think about their personal money situation before making any investment choices. Past results are not a sign of future results.