The Big Picture: A War That Markets Can No Longer Ignore

What started as an already-tense geopolitical backdrop turned outright alarming when Iran announced it had blocked the Strait of Hormuz, threatening to destroy any vessel attempting to cross the critical chokepoint. For four consecutive trading days now, the drumbeat of the U.S.-Iran conflict has been impossible to drown out, and on Tuesday, Wall Street finally flinched.

After absorbing Monday's shocks with surprising composure, the three major indexes opened sharply in the red. At their session lows, the Dow was down more than 1,200 points, the S&P 500 had shed 2.5%, and the Nasdaq was off nearly 2.7%.

The late afternoon saw a meaningful recovery, thanks in large part to President Trump's announcement that the U.S. Navy will escort oil tankers through the Strait of Hormuz and that the Development Finance Corporation will provide political risk insurance for maritime trade at "a very reasonable price." But the rebound only softened the blow.

At the closing bell, the Dow Jones Industrial Average finished at 48,501, down 403 points, or 0.83%. The S&P 500 closed at 6,816, losing 0.94%, while the Nasdaq Composite ended at 22,516, off 1.02%.

Oil: The Elephant in the Room

Brent crude settled at $81.40 per barrel, up nearly 5% on the day and more than 11% since Friday.

WTI crude closed at $74.56. The volatility was extraordinary, at one point during the session, Brent was up over 8%, before Trump's naval escort comments temporarily drove prices sharply lower, only for them to grind back up by the close.

The geopolitical context explains why. Iran has not only blocked the Strait of Hormuz, but also launched air strikes against energy infrastructure across the broader Middle East region. Trump's own timeline is sobering: he indicated the conflict could last another four to five weeks, adding that the U.S. "has the capability to go far longer than that."

JP Morgan has put a number on the downside scenario: if the conflict drags on longer than three weeks, producers in the region may exhaust their storage capacity, potentially pushing oil toward $100–$120 per barrel. That's not a fringe view, it's a base case that investors are starting to price in.

The Macro Implications: Inflation Is Back on the Table

Higher energy prices don't just sting at the pump, they complicate the Federal Reserve's calculus in a significant way. Markets had been comfortably pricing in two rate cuts later this year. That consensus is now wobbling.

The U.S. 10-year Treasury yield climbed 3 basis points on Tuesday to 4.06%, 14 basis points above where it closed on Friday, when it had just touched its lowest level in over a year. As Jennifer McKeown of Capital Economics noted, central banks will likely "look through" the energy shock rather than respond with hikes, but the door to near-term rate cuts is effectively closing if this conflict drags on.

Meanwhile, a curious and historically rare market signal emerged. Strategist Michael Brown of Pepperstone flagged that the S&P 500 fell more than 2%, gold dropped more than 4%, and the U.S. dollar index rose more than 1%, all simultaneously. The last time that combination occurred was October 2008, at the height of the financial crisis.

It signals a kind of forced liquidation environment where even traditional safe havens get sold. The dollar's strength, by contrast, reflects its reserve currency status and the relative advantage the U.S. enjoys as a net energy exporter. The euro bore the brunt of dollar strength, dropping 0.7% to 1.1616 against the dollar.

Retail Shines Through the Gloom

Not every corner of the market was a disaster zone. Two retailers managed to stand out as bright spots on an otherwise dark day.

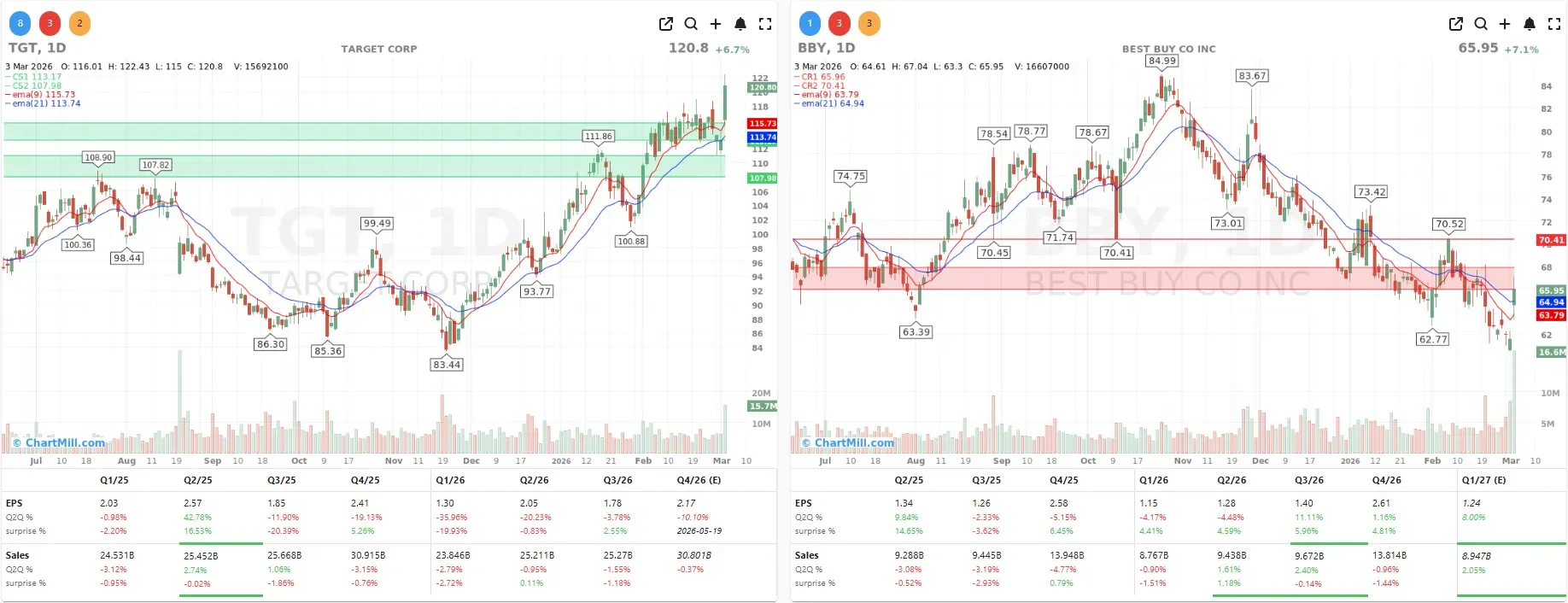

Target (TGT | +6.74% | $120.80) delivered an upside earnings surprise that investors clearly welcomed.

Fourth-quarter adjusted EPS came in at $2.44, comfortably ahead of the $2.16 analyst consensus. For the full year, Target guided for EPS between $7.50 and $8.50, well above the $7.68 Wall Street had penciled in, alongside 2% revenue growth.

New CEO Michael Fiddelke also signaled confidence in the company's turnaround, citing strong February sales trends across clothing, beauty, and food. Capital expenditure will rise by more than $1 billion to approximately $5 billion this fiscal year, targeting supply chain improvements, technology upgrades, and more than 30 new store openings.

Frankly, given the macro backdrop, seeing a traditional retailer put up numbers like this and rally 7% on a broadly awful market day speaks volumes about the underlying business momentum.

Best Buy (BBY | +7.08% | $65.95) also delivered a beat, posting adjusted Q4 EPS of $2.61 versus the $2.47 expected, even as revenue of $13.81 billion came in slightly below the $13.88 billion consensus.

The market clearly decided that margin improvement matters more right now than top-line softness. New and emerging product categories - AI glasses, 3D printers, PC gaming handhelds, health rings - contributed positively, partially offsetting softness in home theater and appliances.

MongoDB: The Day's Most Punishing Decline

If Target was the story of resilience, MongoDB (MDB | -22.24% | $252.73) was the cautionary tale.

The database software company reported results that actually beat expectations for Q4, but the market zeroed in on a guidance miss for Q1: management guided for revenue of $659–$664 million, just shy of the $662 million consensus, with EPS guidance of $1.15–$1.19 against the expected $1.21.

In isolation, those are small misses. But they landed in a market with very little patience for any sign of decelerating growth from premium-valued software names.

MongoDB has been a long-time darling of the cloud and database sector, and the first real signal that its expansion is cooling triggered the stock's largest single-day decline on record. There's a broader message here for investors: the bar for software growth stories remains brutally high.

Other Notable Movers

-

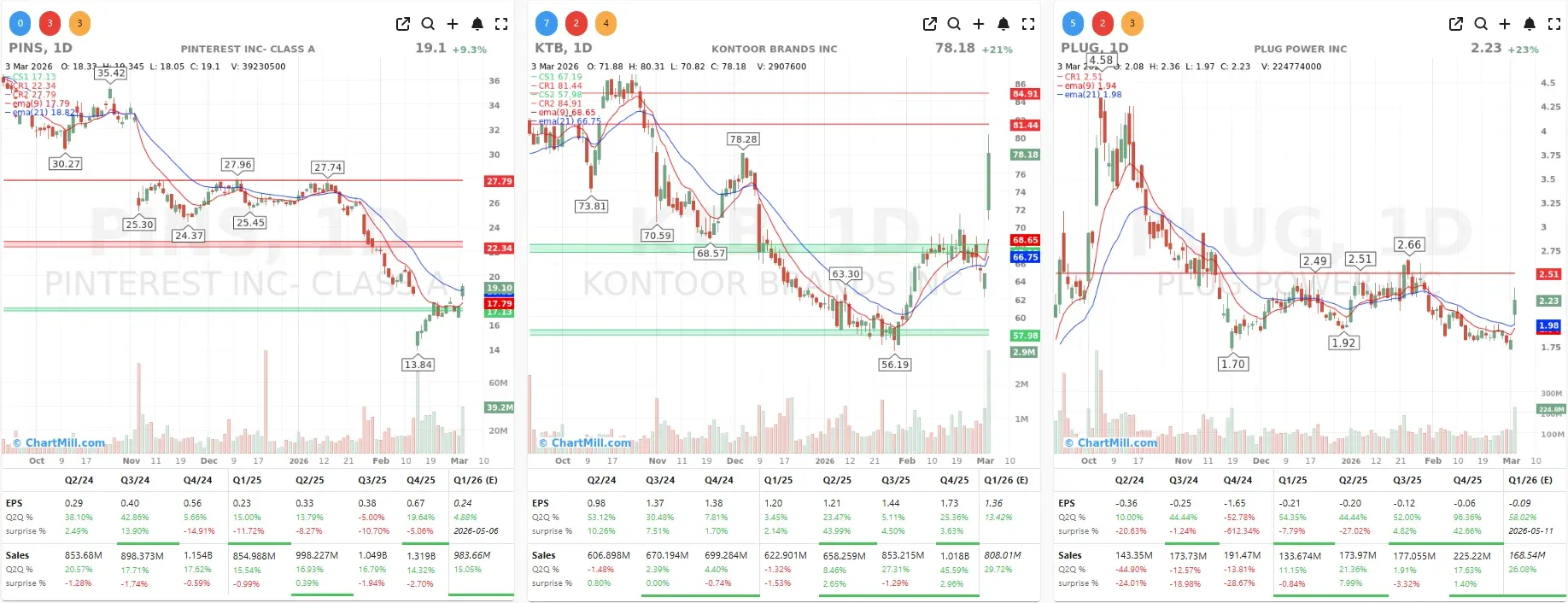

Plug Power (PLUG | +23.2% | $2.23) surged after reporting a smaller-than-expected quarterly loss, giving the hydrogen technology sector a brief moment of optimism. The company still requires additional capital to reach its 2028 targets, but the improved loss trajectory was enough to reignite enthusiasm.

-

Kontoor Brands (KTB | +20.61% | $78.18), parent company of Wrangler and Lee jeans, jumped sharply on a strong Q4 report and upbeat full-year guidance. Management guided for adjusted EPS of $6.40–$6.50, comfortably above the $5.96 analyst estimate.

-

Pinterest (PINS | +9.27% | $19.1) rose after activist investor Elliott Investment Management disclosed a $1 billion stake in the company. Elliott indicated the funds would be directed toward an accelerated share buyback program, a signal that even in a tough market, engaged shareholders can be a meaningful catalyst.

-

On the downside, Micron Technology (MU | -7.99% | $379.68) and fellow memory chipmakers fell more than 8%, following sharp declines in Korean counterparts Samsung and SK Hynix. After being among the year's best performers on AI-driven memory demand, profit-taking arrived with a vengeance.

-

Credo Technology (CRDO | -14.81% | $97.3) dropped despite reporting better-than-expected Q4 results, as its forward guidance disappointed investors who had set a high bar for the AI connectivity specialist.

-

Quantum Computing (QUBT | -10.01% | $7.73) extended its rough stretch, with quarterly revenue declining even as costs climbed.

What to Watch on Wednesday

The macro calendar picks up meaningfully. The ADP private payrolls report drops in the morning, the first employment gauge ahead of Friday's official BLS jobs number. The Fed's Beige Book will also be published, giving investors an anecdotal read on economic conditions across the 12 Federal Reserve districts. In a week dominated by geopolitical noise, the Beige Book could be a useful temperature check on whether the broader economy is still on solid footing.

On the earnings front, results from Broadcom, Okta, and Abercrombie & Fitch are expected and could shift sentiment in semiconductor, cybersecurity, and consumer discretionary sectors respectively.

Bottom Line

Tuesday was a day that reminded even the most seasoned investors why geopolitics can't be dismissed as background noise. The Iran conflict has moved from a weekend headline into a genuine market-moving variable, one that threatens to disrupt energy markets, pressure inflation, and delay the rate cuts that so many portfolios have been positioned for.

The recovery from session lows is encouraging, but it came courtesy of a presidential Tweet, not a change in fundamentals. Markets remain in reactive mode, and until there's a clearer picture of how the Strait of Hormuz situation resolves - or doesn't - volatility will remain elevated.

ChartMill Market Desk

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Breadth Rolls Over Again as Sellers Dominate the Tape