Investors looking for growth openings often face the task of balancing solid expansion possibilities with acceptable valuations. The "Affordable Growth" investment method handles this by focusing on companies that show good growth paths while keeping acceptable financial condition and earnings, all without having extreme market prices. This method tries to find businesses set for continued expansion but available at costs that do not completely show their future possibilities, possibly offering good risk-return balances for investors with long time horizons.

Growth Prospects

ONTO INNOVATION INC (NYSE:ONTO) shows good growth attributes that fit well with the affordable growth method. The company's past results show solid expansion, while future outlooks point to continued progress. The growth rating of 7/10 shows this even view of past results and future chance.

Important growth measures include:

- Past EPS growth averaging 36.96% each year over recent years

- Sales increase averaging 26.41% per year in the past

- Expected EPS growth of 15.71% each year based on coming estimates

- Projected sales growth of 13.58% per year going forward

While the company's newest quarterly EPS growth of 5.92% and sales growth of 6.38% show some slowing from past highs, the basic growth path stays acceptable. The change from outstanding past growth speeds to still-good forward views shows a normal development process more than a worrying deceleration. This change is common for companies moving from early high-growth stages to more maintainable expansion modes, which can often show interesting entry points for investors.

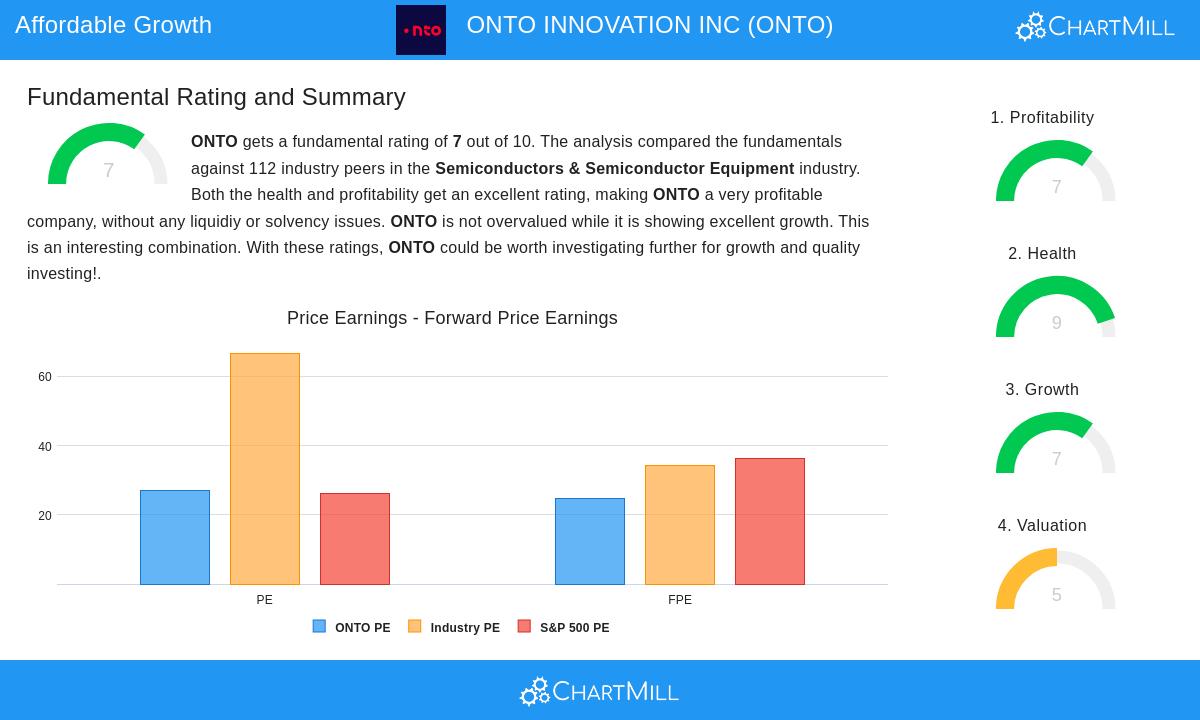

Valuation Assessment

The valuation view for Onto Innovation presents a noteworthy case where standard measures tell different stories. With a valuation rating of 5/10, the company sits in acceptable ground compared to industry friends, though some measures seem high in simple terms. This varied valuation outline is frequent among growing semiconductor equipment companies with good competitive stands.

Notable valuation traits:

- P/E ratio of 27.07, a bit above the S&P 500 average of 26.15

- Forward P/E of 24.61, under the S&P 500's forward average of 36.12

- Enterprise Value to EBITDA ratio lower than 70.54% of industry friends

- Price/Free Cash Flow ratio lower than 81.25% of semiconductor equipment companies

The valuation becomes more interesting when thinking about the company's growth speeds and earnings. While the simple P/E multiple might make some investors stop, the forward multiple discount to the wider market joined with better growth views makes an interesting setup. The company's good market position in semiconductor metrology and inspection equipment gives some reason for higher valuations relative to slower-growing industrial friends.

Financial Health and Profitability

Onto Innovation's excellent financial condition and acceptable earnings give important support for the affordable growth idea. The company has a perfect health rating of 9/10 and a profitability rating of 7/10, pointing to good operational performance and balance sheet strength. These traits lower investment risk while supporting continued growth spending.

The company's financial power is clear in:

- No debt, putting it with the best in the industry for leverage measures

- Current ratio of 9.49 and quick ratio of 7.89, pointing to strong cash position

- Altman-Z score of 24.39, showing very low failure risk

- Profit margin of 17.46%, doing better than 81.25% of industry friends

- Operating margin of 21.25%, also in the top group of the industry

- Return on invested capital of 9.62%, better than 78.57% of rivals

This mix of no debt, strong cash position, and very good earnings gives Onto Innovation important financial room to handle industry changes while continuing to put money into growth projects. The company's skill to create healthy returns on capital while keeping a clean balance sheet is especially useful in the capital-heavy semiconductor equipment field.

Investment Considerations

The basic study of Onto Innovation shows a company that fits well with affordable growth standards. The full fundamental analysis report gives more detail across all rating groups. The company's place in the semiconductor equipment industry gives contact to several long-term growth forces, including advanced packaging, compound semiconductors, and the continuing shrinking of semiconductor parts. These building trends support maintained demand for the company's metrology and inspection answers.

While the company does not give dividends, this matches the growth focus of the method, as money is put back into business expansion instead of given back to shareholders. The mix of acceptable valuation, good growth views, excellent financial condition, and acceptable earnings creates an interesting profile for investors looking for growth at acceptable costs in the technology field.

For investors wanting to find more companies that fit this investment method, the Affordable Growth screen gives other choices that meet these standards. This screening process can help find other possible chances that balance growth chance with acceptable valuations and sound basics.

Disclaimer: This article presents factual information and analysis for educational purposes only and does not constitute investment advice, recommendation, or endorsement of any security. Investors should conduct their own research and consult with financial advisors before making investment decisions. Past performance does not guarantee future results, and all investments carry risk including potential loss of principal.