For investors looking to balance the search for growth with a degree of caution, the "Growth at a Reasonable Price" (GARP) or "Affordable Growth" strategy offers a practical middle path. This method tries to find companies showing solid growth potential that are not yet valued at very high levels, thus aiming to reduce some of the risk found in pure growth investing. A systematic way to apply this is by filtering for stocks with good fundamental scores in growth, profitability, and financial soundness, while checking that the price remains acceptable. One stock that recently appeared from such a filter is ONTO INNOVATION INC (NYSE:ONTO), an important company in the semiconductor equipment industry.

Fundamental Snapshot and Growth Profile

A detailed fundamental analysis of Onto Innovation shows an overall rating of 7 out of 10, with its growth part receiving a solid 7. This score indicates a company in a firm expansion period, backed by both its past performance and future outlook.

- Historical Growth: Over the last few years, Onto has produced a strong record. Revenue has increased at an average yearly rate of 12.55%, while Earnings Per Share (EPS) has risen by an average of 20.68% per year.

- Future Outlook: The growth narrative is forecast to speed up. Analyst projections suggest an average yearly EPS growth of 25.64% and revenue growth of 19.37% in the next few years. This expected increase is a key favorable sign for investors focused on growth.

- Recent Performance: It is important to note a small decrease in EPS over the last year (-7.66%), which is not unusual in the cyclical semiconductor field. However, the strong longer-term averages and much better forward projections imply this could be a short-term slowdown within a longer upward pattern.

For an Affordable Growth strategy, this good and speeding growth profile is the main driver. It gives the fundamental reason for investor attention, but must be examined alongside the current price.

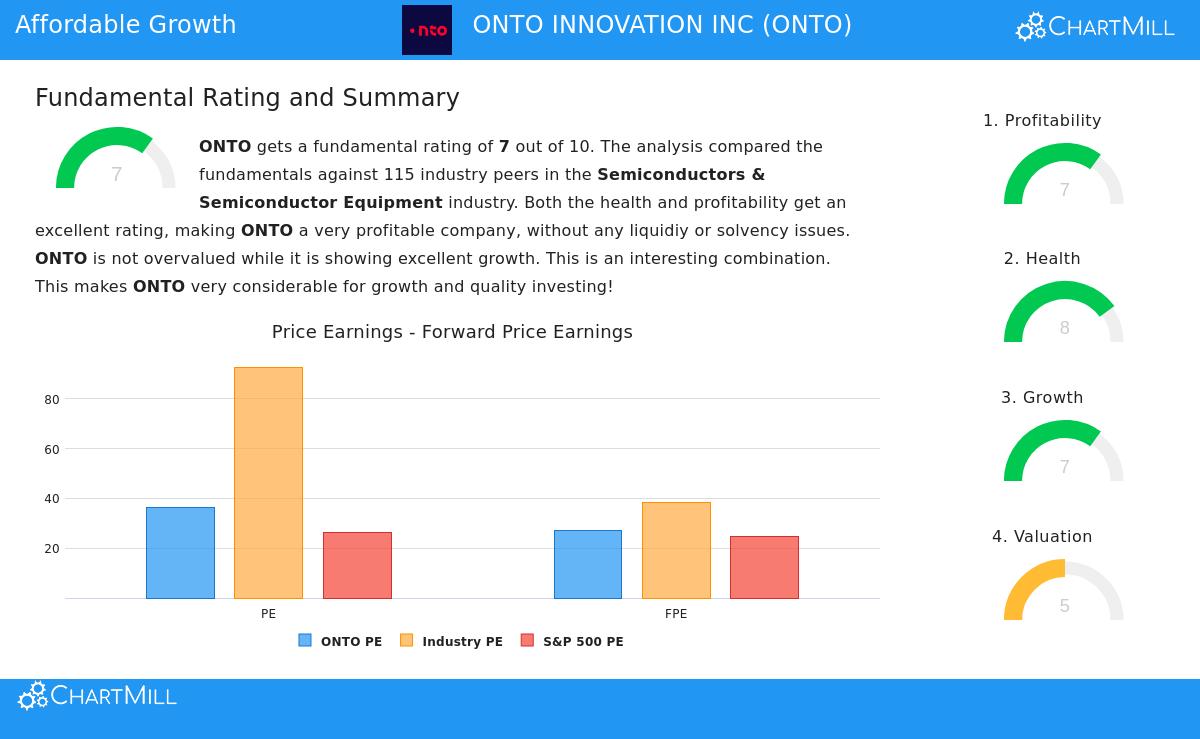

Valuation: Examining the "Affordable" Idea

The valuation rating for Onto Innovation is 5, which meets the minimum level of the filter's need for an "acceptable" valuation. This middle score points to a varied situation, common for a good growth company that is not low-priced, but may not be overly costly compared to its opportunities.

- Price/Earnings Metrics: Onto's current P/E ratio of 36.38 is high next to the wider S&P 500 average. Yet, within its own semiconductor equipment industry, it is less expensive than almost 74% of similar companies. Its forward P/E of 27.03 is similar to the S&P 500 average.

- Cash Flow and EBITDA: More positive signs come from other valuation measures. The company's Price/Free Cash Flow ratio is lower than over 82% of industry rivals, and its Enterprise Value/EBITDA ratio is also more appealing than about 68% of the sector.

- Growth Adjustment: Importantly, when growth is included through the PEG ratio, Onto's valuation seems more reasonable. The analysis states that its "PEG Ratio... shows a fair valuation of the company," and that a higher P/E can be acceptable given its projected earnings growth of more than 25%.

This detailed valuation view is key to the Affordable Growth argument. While not a bargain stock, Onto's price seems connected to its better growth and profitability measures compared to industry peers, not just speculation.

Foundation: Profitability and Financial Soundness

A growth narrative is only lasting if based on a firm base. Onto Innovation scores a 7 for profitability and an 8 for financial soundness, offering that important stability for the GARP investor.

Profitability Advantages:

- The company has strong margins, with an Operating Margin of 19.42% that is better than 78% of the industry. Both its Gross and Operating Margins have been getting better.

- Returns on capital are sound, with a Return on Invested Capital (ROIC) of 7.97% exceeding over three-quarters of industry peers.

Outstanding Financial Soundness:

- Onto keeps a very clean balance sheet with no debt, an uncommon and significant benefit that puts it near the top in its field for stability.

- Liquidity is strong, with a Current Ratio of 5.79 and a Quick Ratio of 4.43, showing more than enough ability to cover near-term needs and put money into future growth.

These high scores in soundness and profitability are what make the growth and valuation numbers believable. They lower the risk of the investment by demonstrating the company is run well, produces good cash flows, and has the financial strength to handle industry changes and pay for its growth plans from within.

Conclusion and Next Steps

Onto Innovation illustrates the Affordable Growth filter's reasoning. It shows the necessary mix of solid, speeding growth projections (a rating of 7) and a valuation (rating of 5) that, while not inexpensive outright, seems acceptable relative to its industry and future outlook. This center is supported by very good financial soundness and firm profitability, which support the durability of its growth path.

For investors wanting to review other companies that match this systematic GARP model, additional results from the Affordable Growth filter are available here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, an endorsement, or a recommendation to buy, sell, or hold any security. Investing involves risk, including the potential loss of principal. Readers should conduct their own thorough research and consider their individual financial circumstances and risk tolerance before making any investment decisions.