In the world of investing, few strategies have lasted as long or shown as much success as value investing. This method is based on finding companies selling for less than their true worth, an idea introduced by Benjamin Graham and later supported by Warren Buffett. The aim is to discover good businesses that the market has incorrectly priced for a short time, giving an investor a "margin of safety." One useful way to spot these chances is to look for stocks that show good fundamental condition and earnings, but are priced in a way that seems separate from their real strength. This pairing points to a possible low price, where a good company might be bought for less than it is worth.

A recent filter using this thinking has pointed to Novartis AG-Sponsored ADR (NYSE:NVS) as a stock that deserves more study. The Swiss drug maker, with its wide range of new treatments and biosimilars, seems to make a strong argument when studied using important fundamental measures. A close look at its finances shows a picture that matches the ideas of looking for good companies at low prices.

Valuation: A Main Part of Value Investing

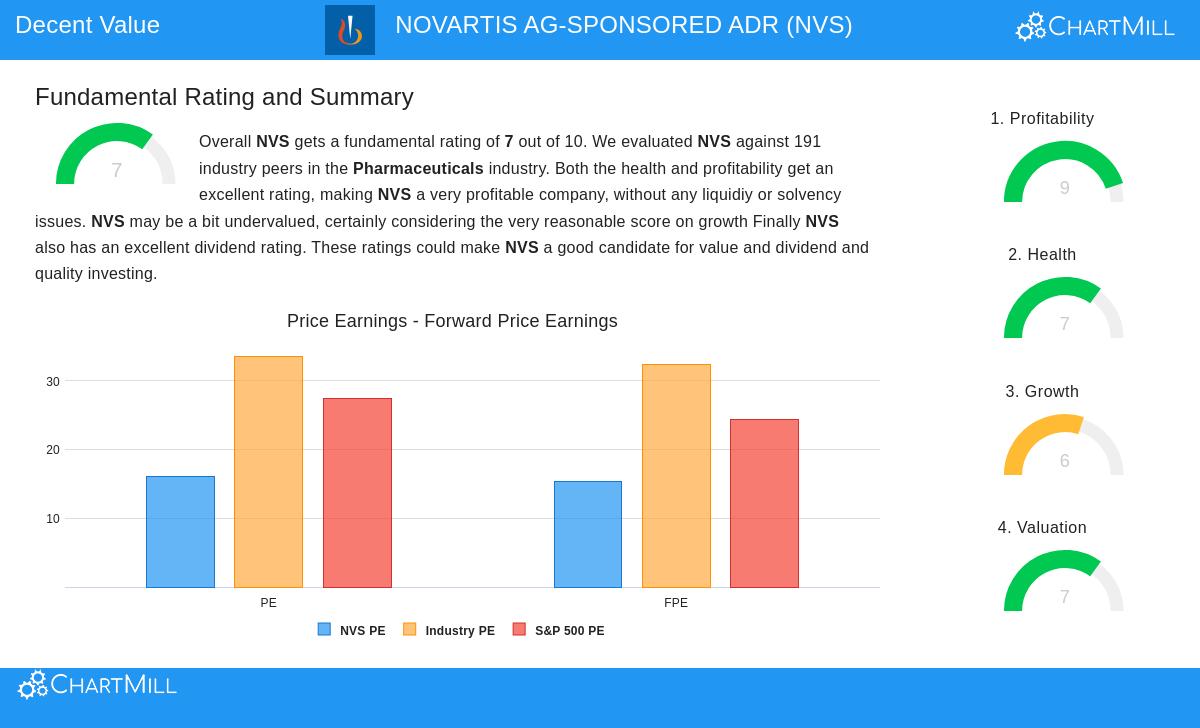

The main idea of value investing is buying an asset for less than its value. For Novartis, the valuation numbers indicate the market might be giving such a chance. The company's present Price-to-Earnings (P/E) ratio of 15.98 is much lower than the industry average of 33.55 and the wider S&P 500 average of 27.38. This lower price is even clearer when looking ahead, with a Price/Forward Earnings ratio of 15.30 next to an industry average of 32.38.

- Price-to-Earnings (P/E): 15.98 (Industry Avg: 33.55)

- Price/Forward Earnings: 15.30 (Industry Avg: 32.38)

- Enterprise Value/EBITDA: Priced lower than 84% of industry competitors.

This fairly low price is especially interesting because it is not due to weak results. Rather, it happens together with strong earnings, which is an important difference. A low P/E ratio is less attractive if the company's earnings are falling. For Novartis, the price seems to pay investors well for the company's current earnings and future increase, a central idea in the hunt for a real value stock.

Earnings & Financial Condition: The Base of Safety

Value investing is not just about buying low-priced stocks, it is about buying sound companies at low prices. A good earnings profile and stable financial condition give the margin of safety that Benjamin Graham stressed. Novartis does very well in these areas, which lowers the danger often linked to low-priced stocks.

The company's earnings score is very high, pushed by top-tier margins and returns. Its Return on Invested Capital (ROIC) of 22.36% and Operating Margin of 33.11% each do better than about 95% of its drug industry peers. This shows very efficient use of money and strong pricing ability for its products.

Financially, Novartis shows high ability to pay debts. Its debt is well-supported by free cash flow, needing only around 1.87 years of FCF to repay all debts, a measure that beats 94% of the industry. While its current and quick ratios point to closer management of working capital, the overall debt picture, backed by a strong Altman-Z score, suggests a basically sound balance sheet able to handle economic changes. This financial strength is exactly what value investors want to make sure the company can last until the market sees its full value.

Increase: The Driver for Value to Be Seen

For a low-priced stock to finally reach its true value, it often needs a trigger. Lasting increase provides that driver, showing that the business is not still and that its earnings can grow over time. Novartis displays a good growth path that backs its price argument.

Recent results have been good, with Earnings Per Share (EPS) growing 21.33% and Revenue rising 12.18% over the last year. Looking forward, experts predict mid-to-high single-digit percentage growth in both EPS and Revenue each year. This stable, dependable growth in a defensive area like healthcare indicates the company's cash flows are lasting. For a value investor, this steady growth helps close the distance between today's market price and a higher future true value, lessening the need for only changes in market feeling.

A Stock for the Value-Centered Portfolio

The combination of these points, a low price, excellent earnings, sound financial condition, and steady growth, creates an image of a high-quality business that may be trading at a price under its true value. Novartis works in the necessary healthcare sector, giving some safety from downturns, and gives shareholders a dependable dividend yield now near 3.06%, which is much higher than industry and market averages.

This profile is what value-focused filters are made to find, companies where the market's present judgment seems separate from the fundamental truth of the business. It represents the idea of seeking a margin of safety not through risky guesses, but through measured study of financial power and price.

For investors wanting to study other companies that fit similar standards of fair price, good earnings, condition, and growth, more study can be done using set filters. You can find more possible stocks from this "Fair Value" method by checking the filter results here.

Disclaimer: This article is for information only and does not make financial advice, a suggestion, or an offer to buy or sell any security. Investing has risk, including the possible loss of original money. Readers should do their own complete study and think about their personal money situation before making any investment choices.