In the search for investment opportunities, many strategies exist, but few have the enduring history of value investing. At its center, this method, supported by figures like Benjamin Graham and Warren Buffett, involves finding companies trading for less than their intrinsic value. The aim is to find good businesses that the market has temporarily mispriced, providing a "margin of safety" for the investor. One way to find such candidates is to look for stocks with good basic foundations, like profitability and financial condition, that are also trading at low prices. This pairing indicates a company is not only low-priced, but low-priced without a clear cause, possibly offering a strong chance for the patient investor.

A recent search for "good value" stocks, which looks for companies with high valuation marks while keeping good scores in growth, condition, and profitability, has identified Novartis AG-Sponsored ADR (NYSE:NVS). The Swiss pharmaceutical leader, with its large collection of new medicines and biosimilars, seems to show a situation where market price may not completely show basic strength. An examination of the company's detailed basic report shows the numbers behind this view.

Valuation: Trading at a Lower Price Than Peers

For a value investor, a low price is the starting point. It shows the possible difference between price and worth. Novartis gets a 7 out of 10 on ChartMill's Valuation Rating, meaning it is priced well compared to its own past and its industry.

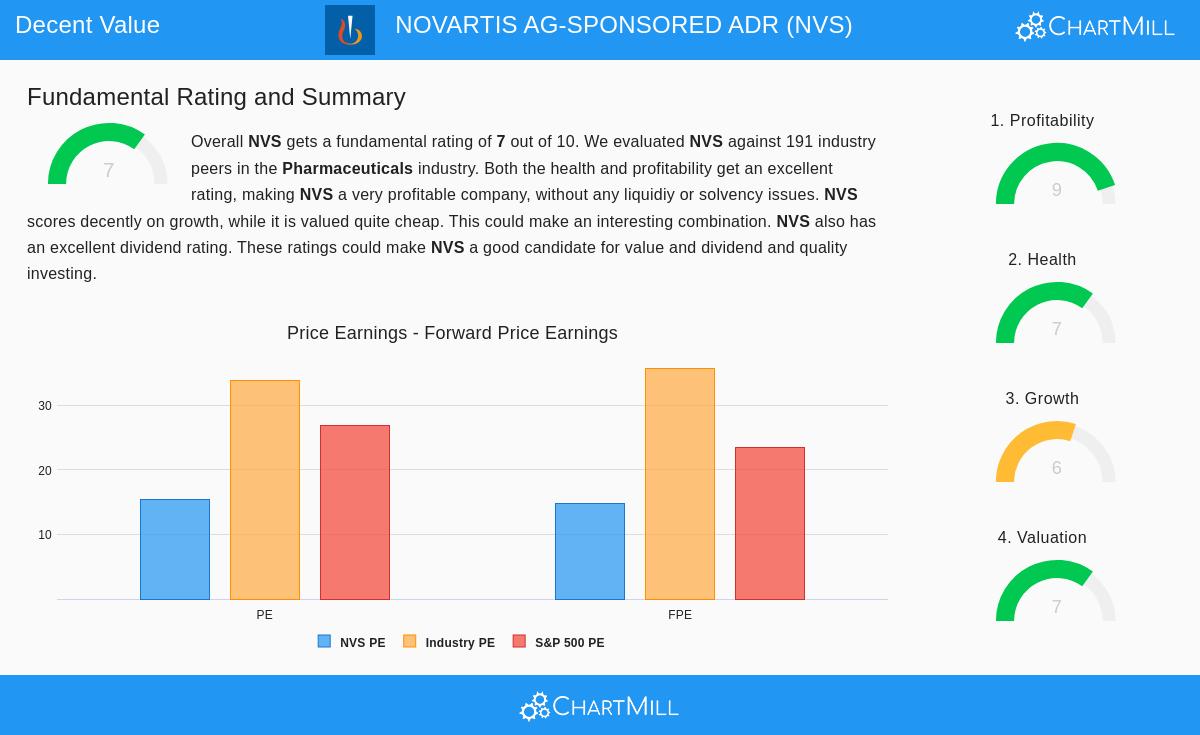

- Price-to-Earnings (P/E): At 15.41, NVS's P/E ratio is seen as a fair price on its own. However, the important point is in the comparison. This ratio is lower than 85% of its peers in the pharmaceuticals industry, where the average P/E is above 33.

- Forward P/E and Enterprise Value: The pattern continues with future and cash-based measures. A Forward P/E of 14.75 is lower than 82% of the industry, and its Enterprise Value to EBITDA ratio is lower than 84% of competitors.

- PEG Ratio: Maybe most significant for a growth-focused value investor is the small PEG ratio, which changes the P/E for expected earnings growth. This shows the market may not be fully paying investors for the company's future growth potential.

This overall valuation view is key for the strategy. It suggests investors are not paying extra for Novartis's business, possibly creating the margin of safety value investors look for.

Profitability & Condition: The Base of Quality

A low-priced stock is only a good buy if the company is basically sound. This is where the danger of a "value trap"—a low-priced stock that remains low-priced—is reduced by checking profitability and financial condition. Novartis does very well here, with a top Profitability Rating of 9/10 and a good Health Rating of 7/10.

Profitability Positives:

- High Returns: The company produces a Return on Invested Capital (ROIC) of 22.36%, doing better than 97% of its industry. Its Return on Equity is a notable 32.47%.

- Good Margins: A Profit Margin of 25.69% and an Operating Margin of 33.11% are near the top in the sector, showing efficient operations and pricing ability.

Financial Condition Check:

- Solvency is Good: With an Altman-Z score of 4.16 and a small Debt-to-Free Cash Flow ratio of 1.87 years, Novartis has no bankruptcy risk and can easily handle its debt.

- Liquidity Detail: The report mentions weaker current and quick ratios, which often point to short-term cash concerns. However, it explains this by saying that given the company's "top solvency and profitability," these ratios may not show a real cash problem and could be linked to the details of its global business activities.

For the value investing process, this strong profitability and overall financial condition are essential. They give confidence that the low-priced asset is a good business able to handle economic changes and increase value over time.

Growth & Dividend: The Driver for Value Recognition

A low-priced company must also have a way for the market to see its worth. Steady growth provides that catalyst. Novartis has a Growth Rating of 6/10, showing acceptable momentum.

- Recent Momentum: Over the last year, the company has reported good growth with Earnings Per Share (EPS) up 21.33% and Revenue increasing 12.18%.

- Future Predictions: Analysts think this positive trend will continue, with EPS expected to grow at an average rate of 9.35% each year in the near future. Importantly, the revenue growth rate is predicted to speed up compared to its past average.

Also, with a Dividend Rating of 7/10, Novartis gives a shareholder return that improves the value case. Its 3.18% dividend yield is much higher than both the industry and S&P 500 averages, and it is backed by a steady 10-year payment history and workable payout ratios. For value investors, a steady dividend can provide income while waiting for the market to re-price the stock.

Conclusion

Novartis shows a profile that matches key ideas of value investing: it is priced lower than its pharmaceutical peers, yet it is built on a base of high profitability and good financial solvency. Along with acceptable growth potential and a steady, above-average dividend, the stock fits the "good value" search's aim—finding basically sound companies trading at low prices. While the pharmaceutical sector deals with ongoing tests from patent ends and innovation cycles, Novartis's size, research pipeline, and current financial measures suggest it is prepared to handle them.

This review of Novartis came from a methodical search for investment ideas. If you want to look at other companies that fit similar standards of good valuation, profitability, condition, and growth, you can see the full Good Value Stocks search for more possible chances.

Disclaimer: This article is for information only and does not make up financial advice, a suggestion, or an offer to buy or sell any security. Investing includes risk, including the possible loss of principal. You should do your own study and talk with a qualified financial advisor before making any investment choices.