In the hunt for investment chances, many investors use a disciplined, basic method that tries to find companies selling for less than their true value. This process, called value investing, uses filters to find stocks that seem priced low by the market using important financial measures, while also showing basic business soundness. One filter looks for companies with good valuation marks, meaning they may be priced well, along with fair marks in profit, financial condition, and expansion. This mix tries to find not only low-priced stocks, but basically good businesses the market may not have noticed for now.

A recent filter using this "fair value" method has pointed to NICE LTD - SPON ADR (NASDAQ:NICE) as a possible choice. The Israeli business software company, which provides customer service and financial crime compliance tools, shows an interesting picture for investors looking at price. Based on ChartMill's basic review, NICE gets a total mark of 6 out of 10, but its part scores show a more detailed view that fits well with value-focused rules.

An Interesting Valuation View

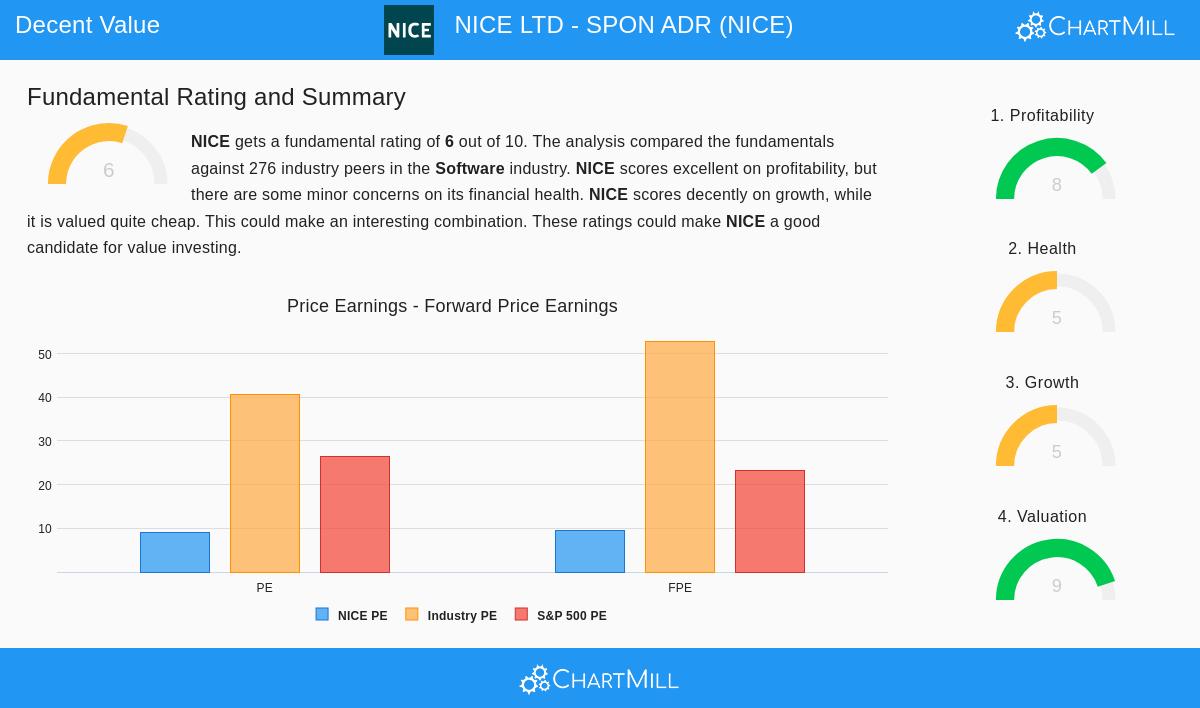

The most notable part of NICE's basic report is its valuation mark, which gets a high 9 out of 10. This mark is key for a value filter, as it clearly shows if a stock is trading at a lower price compared to its earnings, cash flow, and industry friends. For value investors, a high valuation mark hints at a bigger "safety gap," a central idea of the method that offers protection from mistakes in review or unexpected market drops.

The report lists several numbers that build this good valuation:

- Price-to-Earnings (P/E) Ratio: At 9.15, NICE's P/E ratio is called "very fair." It is priced lower than 89% of its software industry friends and is much under the S&P 500 average of 26.51.

- Forward P/E Ratio: The future-looking number of 9.47 also shows a fair valuation, lower than 88% of the industry.

- Enterprise Value/EBITDA and Price/Free Cash Flow: Using these cash-flow-based multiples, NICE is valued at a lower price than over 91% of companies in its field.

These numbers imply the market is pricing NICE cautiously, possibly making a chance for investors if the company's basic results keep going.

Basic Profit Soundness

While a low price is needed, value investing ideas caution against "value traps"—companies that are low-priced for a cause, often because of weak or worsening business basics. This is where NICE's profit mark of 8 out of 10 becomes important. A solid profit mark shows the company is making real earnings from its work, a main point in judging its true value and lasting power.

The basic review notes several areas of soundness:

- The company has been profitable with positive operating cash flow in each of the last five years.

- Important return measures like Return on Assets (10.83%) and Return on Invested Capital (11.19%) put NICE in the best group of its industry, doing better than over 86% of friends.

- Profit and operating margins are not only good but have gotten better in recent years.

This solid profit gives a firm base, suggesting the low valuation is not a sign of a failed business plan but could be a market pricing error.

Reviewing Financial Condition and Expansion

The filter also asked for fair marks in financial condition and expansion, which work as extra screens to avoid dangerous or still companies. NICE's condition mark is a middle 5, with the report noting a clear balance sheet—the company has no debt—which is a big plus for stability. However, it carries a warning about a rise in shares available over the past year, which can lessen current shareholders' value if not matched by equal earnings expansion.

The expansion mark is also a 5. The past record is firm, with Revenue expanding at an average yearly rate of 11.69% and Earnings Per Share (EPS) expanding at 15.93% over recent years. The future view, though, shows a predicted slowing. Revenue is still forecast to expand at a good 8.47% yearly, but EPS expansion is expected to slow to about 5%. For a value investor, the shown past expansion joined with fair future hopes can be okay, mainly when matched with a very low earnings multiple.

Final Point: A Value Case in Software

NICE shows a situation that fits a disciplined value method. Its very high valuation mark shows it is trading at a big discount to the wider market and its own industry. This discount exists next to a very good profit picture and a debt-free balance sheet, which helps lower the risk often linked to very low-priced stocks. While its expansion may be changing to a more steady speed, its past record and continued revenue growth suggest a stable, cash-making business.

The mix of a low price compared to earnings and solid basic facts makes NICE a stock worth more look for investors using a value-based filter method. The full basic review report for NICE gives a closer look into all the numbers talked about.

For investors wanting to find other companies that fit this picture of good valuation paired with fair basics, you can look at more results using the Fair Value Stocks filter on ChartMill.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or a deal to buy or sell any securities. The information given is based on supplied data and should not be the only ground for any investment choice. Investing has risk, including the possible loss of original money. Always do your own review and think about talking with a qualified financial advisor before making any investment choices.