The investment philosophy of legendary fund manager Peter Lynch has long been a foundation for investors looking to find quality growth companies at fair prices. His strategy, often called Growth at a Reasonable Price (GARP), focuses on lasting earnings growth, sound financial health, and appealing valuations. It is a methodical process that steers clear of speculative, expensive stocks in favor of businesses with clear, established models that can provide steady returns over time. A recent filter using Lynch's main standards has highlighted one company that seems to fit these ideas closely: NICE LTD, SPON ADR (NASDAQ:NICE).

Fit with Peter Lynch's Main Standards

The Lynch filter looks for companies that show a particular mix of growth, earnings, and steadiness. NICE, a supplier of enterprise software for customer communications and financial crime compliance, satisfies many of these numerical checks.

- Lasting Earnings Growth: Lynch preferred companies with a reliable, lasting growth path, usually seeking a 5-year earnings per share (EPS) growth rate from 15% to 30%. NICE shows an EPS growth rate near 16.5% over the last five years, putting it directly within this target range. This points to a record of regular profit increase without the concerns of extreme growth that may not last.

- Appealing Valuation using PEG Ratio: Maybe the most important Lynch measure is the Price/Earnings to Growth (PEG) ratio, which tries to find stocks that could be priced low compared to their growth rate. A PEG ratio of 1 or less is seen as appealing. NICE's PEG ratio, calculated from its past five-year growth, is near 0.56, hinting the market may be pricing its historical growth pattern too low.

- Sound Profitability (ROE): Lynch searched for companies that create profits from shareholder equity with good effect. A Return on Equity (ROE) over 15% is a main filter. NICE's ROE of 15.8% meets this mark, indicating capable management and a profitable operation.

- Firm Financial Health: The method favors companies with firm balance sheets to endure economic changes. Two important health tests are:

- Debt/Equity Ratio: Lynch liked very little debt, with a perfect ratio under 0.25. NICE does very well here with a Debt/Equity ratio of 0.0, meaning no interest-bearing debt and a very strong balance sheet.

- Current Ratio: This checks short-term cash availability, with a figure over 1.0 being satisfactory. NICE's Current Ratio of 1.55 shows it has enough short-term assets to meet its immediate liabilities without strain.

Basic Health and Valuation Summary

A wider view of NICE's basic profile, as shown in its detailed analysis report, supports the image from the Lynch filter. The company receives a firm total basic rating, with specific high points in earnings and valuation.

The earnings figures are strong, with sector-leading margins and returns. The company's Operating Margin of 22.23% and Return on Invested Capital (ROIC) of 12.43% are better than a large portion of its software industry counterparts. This high degree of earnings is a central part of the Lynch method, as it offers a safety buffer and pays for future expansion.

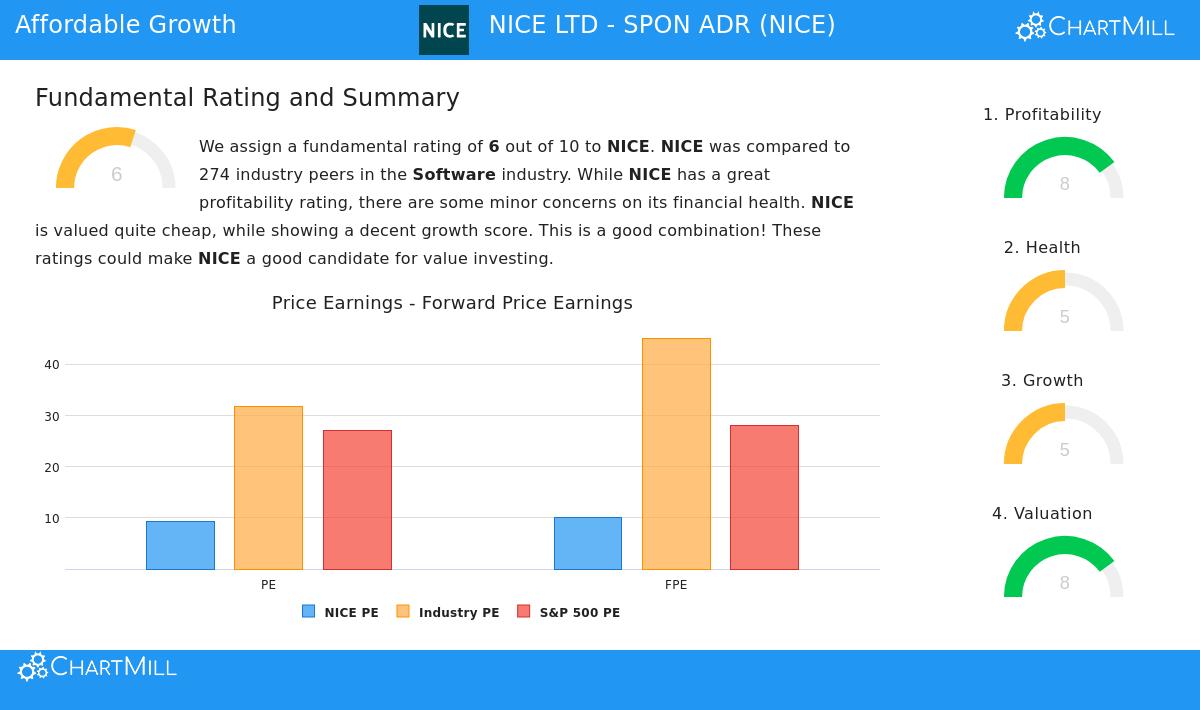

From a valuation view, NICE seems interesting. Its standard Price-to-Earnings (P/E) ratio of 9.32 and Forward P/E of 9.98 are not only much lower than present S&P 500 norms but are also less expensive than about 85-90% of its software industry rivals. This valuation gap, especially when combined with its historical double-digit EPS growth and sound earnings, is exactly the situation GARP investors look for.

The main point of care in the report relates to growth forecasts. While past growth has been sound, analysts predict a notable slowing in EPS growth ahead. This is a vital area for more study, as the Lynch method depends on the ongoing presence of fair growth, not only past results.

A Prospect for More Study

For investors following the ideas of Peter Lynch, NICE offers an interesting example. It meets the first numerical filters very well, showing a history of careful growth, outstanding financial health with no debt, high earnings, and a valuation that seems modest. The company works in the necessary, if sometimes "ordinary," areas of customer service software and regulatory compliance, sectors with lasting need that Lynch might favor.

However, the filter is only a first step. Lynch himself highlighted the need to know the business behind the data. The central question for a potential investor is if NICE can maintain a mid-teens growth rate in the next years, or if the expected slowdown is a lasting change. This needs more examination of its market standing, competitive edges, and future growth sources.

This review of NICE was found using a stock filter created on Peter Lynch's investment standards. You can review other companies that currently meet these same filters for lasting growth, firm finances, and fair prices by seeing the complete Peter Lynch Strategy filter results.

Disclaimer: This article is for information only and is not financial guidance, a suggestion, or an offer to buy or sell any securities. The review uses given data and a particular investment strategy model. Investors should do their own complete study and think about their personal money situation before making any investment choices.