For investors looking for a dependable source of passive income, a methodical screening process is needed to distinguish solid dividend payers from risky high-yield stocks. A typical approach uses filters for companies that provide a good dividend and also have the fundamental financial capacity to maintain and possibly increase those payments. This usually leads to searching for stocks with strong dividend ratings, along with acceptable ratings for earnings strength and balance sheet condition. These measures help find businesses that are producing enough profit, handling their debts prudently, and focusing on shareholder returns, a mix that can offer income and steadiness in an investment portfolio.

Magna International Inc (NYSE:MGA) appears as a prospect from this kind of screening method. As a worldwide automotive supplier based in Canada, Magna creates and builds a broad range of vehicle parts, including body frames, engines, seats, and driver-assistance technology. Its role as a major partner to car manufacturers globally offers a stable base, although it is naturally connected to the ups and downs of the worldwide auto sector.

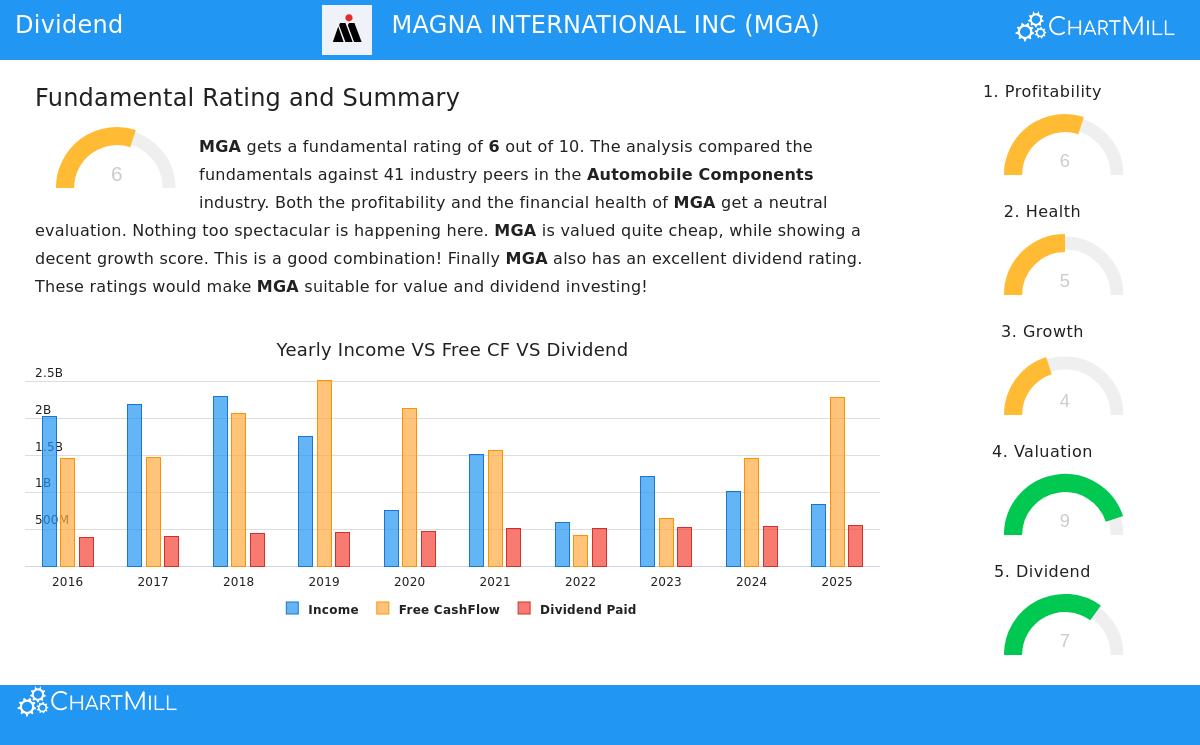

Dividend Attraction and Long-Term Viability

For investors concentrating on income, Magna’s dividend characteristics show several positive points, which are outlined in its detailed fundamental analysis report.

- Good Yield: The company now has an annual dividend yield of 3.26%. This is higher than the average yield for the S&P 500 (about 1.82%) and its group in the Automobile Components industry (average 0.66%). Magna’s yield is better than 95% of its industry rivals.

- Steady History: Dependability is important for dividend investing. Magna has built a steady record, having paid a dividend for at least 10 straight years without a cut. This history points to a company policy of giving capital back to shareholders during different market conditions.

- Increase and Distribution Balance: The dividend has increased at a yearly rate of about 4.55% over the last five years. This steady rise is favorable. Experts project the company’s earnings per share (EPS) to increase more quickly (over 10% each year) in the near future, which may allow for further dividend raises. A point to consider is the present payout ratio, which is at 65.62% of earnings. This is above the level typically viewed as most secure, showing a large part of profit is being paid out. Investors should watch this ratio to confirm earnings growth stays ahead of dividend growth, maintaining the payout.

Supporting Business Basics: Earnings and Condition

A high dividend yield is less attractive if the company cannot support it. The screen's requirement of "acceptable profitability and health" is key here, as they verify the dividend's feasibility. Magna’s ratings in these areas give background for its dividend rating.

- Earnings Evaluation: Magna has a ChartMill Profitability Rating of 6. The review indicates the company is regularly profitable with positive earnings and cash flow. Its return on equity (6.64%) and return on invested capital (7.13%) are good, doing better than most industry peers. While its profit margins are modest—typical in the automotive supply business—they have gotten better lately. This basic earnings ability is necessary as it creates the cash required to pay the dividend.

- Financial Condition Review: With a ChartMill Health Rating of 5, Magna’s balance sheet presents a varied situation. Positively, the company has been lowering its share count and keeps a sensible debt-to-equity ratio of 0.38, indicating a good mix of debt and equity funding. Its debt compared to free cash flow is also positive, meaning it could settle debts fast if required. The main issues are in liquidity measures; its current and quick ratios are below many industry peers, which could mean closer management of working capital. In total, the condition profile is sufficient but notes points for an investor to observe, especially in industry slowdowns.

Price Consideration

A frequently missed part of dividend investing is the cost paid for the income. Magna seems to present value here, with a ChartMill Valuation Rating of 9. The stock has a P/E ratio of 9.85 and a forward P/E of 8.08, which is low compared to the wider market and about 83% of its industry rivals. This pricing offers a buffer and adds to the higher yield, since the dividend is a bigger part of a lower stock price.

A Prospect for More Study

Magna International stands as a possible option for a dividend investor’s list. It gives a yield that is good on its own and compared to others, supported by a ten-year practice of shareholder payments. The supporting basics—sufficient earnings and a mostly stable, though not perfect, balance sheet—give a reason for why it cleared a methodical screen. The price adds a chance for share price growth to the income argument. Still, the higher payout ratio and exposure to a cyclical industry are elements that need constant attention.

For investors wanting to review other companies that match similar standards of good dividend traits paired with adequate financial condition and earnings, the Best Dividend Stocks screen offers a changing beginning point for more investigation.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation to buy or sell any security, or an endorsement of any investment strategy. All investing involves risk, including the potential loss of principal. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions.