The investment philosophy of legendary fund manager Peter Lynch, as detailed in his book One Up on Wall Street, focuses on finding well-run, expanding companies available at sensible prices, a strategy often called Growth at a Reasonable Price (GARP). Lynch supported a long-term, buy-and-hold method, concentrating on businesses with durable earnings expansion, sound financial condition, and prices that do not overvalue future potential. His approach uses particular quantitative filters to sort for these traits, highlighting an orderly system instead of speculative market timing.

One firm that now meets a filter built on Lynch's main rules is META PLATFORMS INC-CLASS A (NASDAQ:META), the parent firm of Facebook, Instagram, WhatsApp, and a frontrunner in virtual reality via its Reality Labs division. For investors looking for long-term GARP possibilities, Meta offers a strong example of how a large technology company can fit a classic value-focused growth plan.

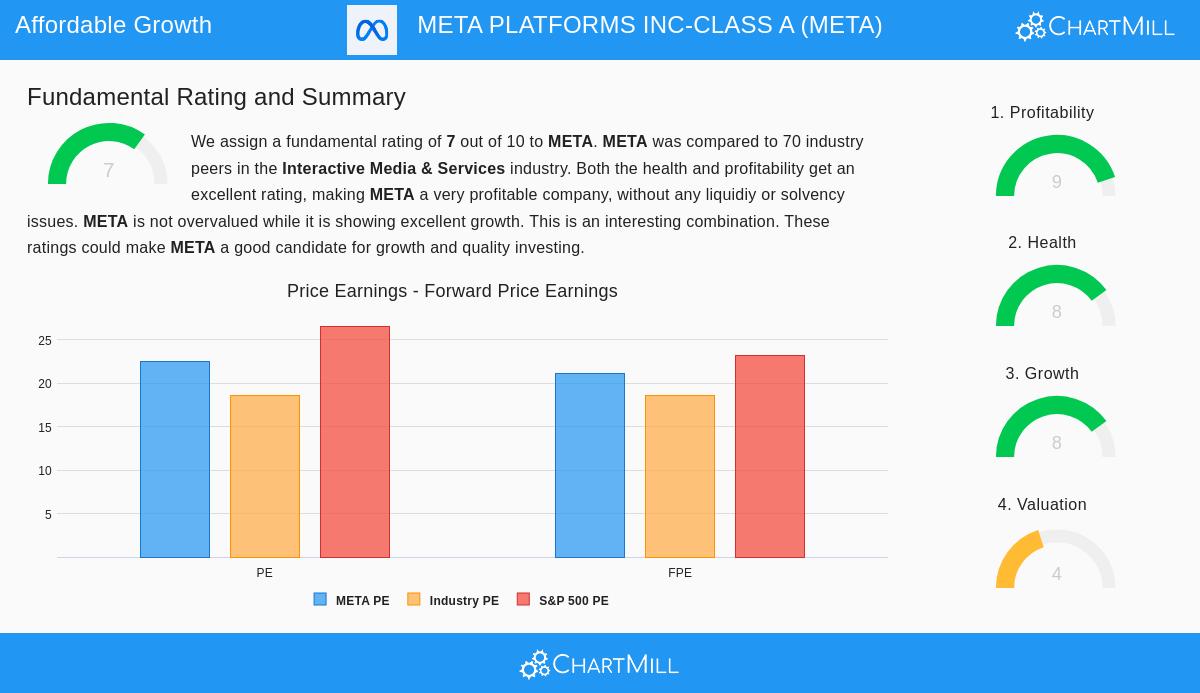

Fit with Peter Lynch Filtering Rules

The Peter Lynch filter looks for companies with a distinct profile: solid but maintainable historical expansion, high earnings, firm financial standing, and a good price when growth is considered. Meta's present financials match these rules closely.

- Maintainable Earnings Expansion: Lynch preferred companies with a steady record of earnings growth, usually between 15% and 30% each year, as quicker expansion is frequently not maintainable. Meta's 5-year average Earnings Per Share (EPS) growth of 22.8% sits directly within this desired zone, showing a firm and stable historical increase in earnings.

- Sensible Price (PEG Ratio): A central part of Lynch's plan is the Price/Earnings to Growth (PEG) ratio, which tries to find stocks that might be priced low compared to their expansion rate. He usually sought a PEG of 1 or lower. Meta's PEG ratio, calculated from its last 5-year growth, is about 0.99, meeting this important standard and hinting the market may not completely account for its historical growth path.

- High Earnings (Return on Equity): Lynch saw a strong Return on Equity (ROE) as a mark of an effective and profitable business. He often used a minimum level of 15%. Meta's ROE of 30.2% greatly passes this need, showing a notable skill to produce earnings from shareholder equity.

- Financial Condition (Debt & Liquidity): Careful financial management was important for Lynch. He liked companies with little debt and enough cash. Meta's Debt-to-Equity ratio of 0.15 is much lower than the filter's limit of 0.6 (and even Lynch's tighter liking for below 0.25), showing very little use of debt funding. Also, its Current Ratio of 1.98 easily passes the filter's need of 1.0, indicating a firm ability to meet near-term bills.

Fundamental Condition and Expansion Outline

A wider view of Meta's fundamental report supports the image shown by the Lynch filter. The company receives a high total fundamental score, led by high performance in two areas Lynch stressed: earnings and financial condition.

- Notable Earnings: Meta's margins lead its industry, with an Operating Margin above 43% and a Profit Margin close to 31%. Its efficiency measures are also strong, with Return on Invested Capital (ROIC) of 26.6% much higher than its cost of capital, meaning it is building major value for shareholders.

- Firm Financial Soundness: The company holds a very strong balance sheet with an Altman Z-score pointing to very small failure risk. Its large free cash flow production lets it put money into future projects like AI and the metaverse while also paying for a big share buyback effort, another feature Lynch liked.

- Expansion Path: While future EPS growth is predicted to slow from its excellent past rate, experts still forecast a good growth rate in the low double-digits, backed by ongoing revenue growth. This move toward a more maintainable, yet still firm, expansion outline fits the Lynch idea of avoiding trendy stocks with improbable growth hopes.

You can examine the complete fundamental study for META here.

Investor Points

For the GARP investor, Meta presents a distinct case. It is a leading, cash-producing leader in its field that still shows expansion features commonly linked with smaller firms. Meeting the Peter Lynch filter implies its present market price does not seem to ask for a high cost for ideal conditions, instead giving a sensible price for its quality and growth. Still, investors must think about the company's major investments in long-term, uncertain projects like the metaverse, which currently reduce total earnings, and the constant regulatory attention facing the technology industry. These are the non-quantitative factors Lynch would require investors to study completely after the quantitative filter gives the first sign.

The Peter Lynch plan is made to methodically find companies with these balanced features. If you want to review other stocks that now meet this orderly growth-at-a-reasonable-price filter, you can see the complete list of outcomes here.

Disclaimer: This article is for information only and is not financial guidance, a support, or a suggestion to buy, sell, or hold any security. Investing has risk, including the possible loss of original money. Always do your own research and think about talking with a registered financial advisor before making any investment choices.