In the search for long-term investment opportunities, many investors turn to the principles of legendary fund manager Peter Lynch. His strategy, often categorized as Growth at a Reasonable Price (GARP), focuses on finding companies with strong, sustainable growth, excellent financial health, and a share price that does not overpay for that future potential. It is a disciplined method that prioritizes fundamental strength over market speculation. A filter using Lynch’s main criteria recently identified Lululemon Athletica Inc (NASDAQ:LULU) as a stock deserving closer examination from investors with a similar long-term view.

Using the Peter Lynch Framework

Peter Lynch’s methodology is constructed on specific filters made to distinguish quality growth companies from overhyped or financially weak ones. The main ideas include a history of strong but sustainable earnings growth, high profitability, a firm balance sheet, and a valuation that rewards investors for the growth they are purchasing. For a stock like Lululemon, the filter assesses several specific measures that fit this philosophy.

- Sustainable Earnings Growth: Lynch preferred companies increasing earnings per share (EPS) between 15% and 30% each year over a five-year period. Growth above 30% was often seen as unsustainable. Lululemon’s five-year EPS growth rate of 24.37% sits well within this target range, indicating a history of solid, yet potentially maintainable, expansion.

- Valuation Relative to Growth (PEG Ratio): Perhaps the central part of the GARP method, the Price/Earnings to Growth (PEG) ratio measures if a stock’s price is sensible relative to its earnings growth. A PEG ratio of 1 or below is usually seen as attractive. Lululemon’s PEG ratio, based on its past five-year growth, is 0.52, indicating the market may be undervaluing its historical growth path.

- Financial Health and Profitability: Lynch required companies with firm balance sheets and high returns on capital.

- Debt/Equity Ratio: Lululemon’s Debt/Equity ratio is 0.0, meaning it operates with no interest-bearing debt. This meets Lynch’s own strict preference for a ratio below 0.25 and puts the company in a very strong financial state.

- Current Ratio: At 2.13, Lululemon’s Current Ratio shows more than enough liquidity to cover its short-term obligations, passing another of Lynch’s health tests.

- Return on Equity (ROE): An ROE above 15% signals efficient use of shareholder capital. Lululemon’s ROE of 38.67% is exceptional, showing highly profitable operations.

Fundamental Analysis Summary

A wider fundamental analysis of Lululemon supports the strengths found by the Lynch filter. The company receives a high total score, with particular strength in financial health and profitability. Its balance sheet is very clean, with no debt and firm liquidity measures. Profitability margins, including operating and net profit margins, are near the top in the Textiles, Apparel & Luxury Goods industry. While future growth expectations have become more conservative compared to the strong past five years, analysts still forecast steady mid-to-high single-digit growth in revenue and earnings.

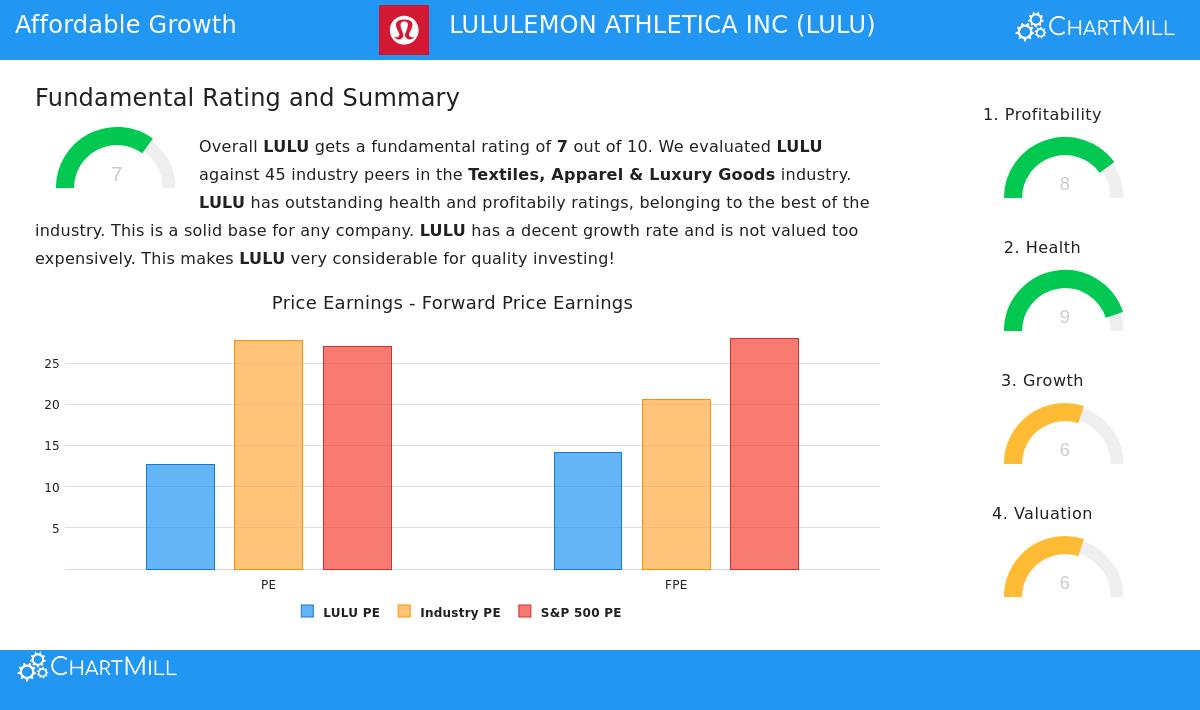

From a valuation standpoint, Lululemon trades at a Price-to-Earnings (P/E) ratio that is viewed as sensible both relative to the wider S&P 500 and its own industry peers. This, together with its better profitability, forms the "reasonable price" argument within the GARP thesis. For a detailed breakdown of these measures, you can examine the full fundamental analysis report for LULU.

Investment Case for the Long-Term Investor

For an investor following Peter Lynch’s philosophy, Lululemon presents a strong example. The company has clearly executed a strategy of premium brand building and careful expansion, leading to the powerful earnings growth and excellent profitability measures the filter identified. Its debt-free balance sheet provides great operational flexibility and stability in uncertain economic times, a main factor for long-term holding.

The central question for a GARP investor is if the company’s future growth supports its current valuation. The low PEG ratio, calculated from its strong past growth, indicates the market may not be fully valuing the company’s quality and brand strength. While future growth is expected to be more moderate, the mix of a powerful brand, clean financials, and a sensible valuation creates a base for potential long-term increase of shareholder value. It represents the Lynch ideal of a well-understood business with a lasting competitive advantage trading at a sensible price.

Finding More Opportunities

Lululemon is one of the companies that passed a specific filter based on Peter Lynch’s investment rules. Investors curious about finding other companies that meet these standards for sustainable growth, financial health, and sensible valuation can view the complete list of results via the Peter Lynch Strategy stock screener.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. The analysis is based on data and a specific investment strategy framework; investors should perform their own complete research and consider their personal financial circumstances before making any investment decisions.