For investors looking for chances where the market price may not completely show a company's inherent strength, a methodical screening method can be a helpful first step. One such technique finds stocks that join an attractive valuation with good fundamental condition, earnings strength, and acceptable expansion potential. This method tries to find companies that are not only low-priced, but are financially stable and operationally efficient, possibly providing a safety buffer for investors focused on value. A recent filter for "acceptable value" stocks, which looks for a high valuation grade together with acceptable grades in other important fundamental categories, has pointed out Lantheus Holdings Inc (NASDAQ:LNTH) as a name deserving more detailed study.

A Detailed View of the Fundamentals

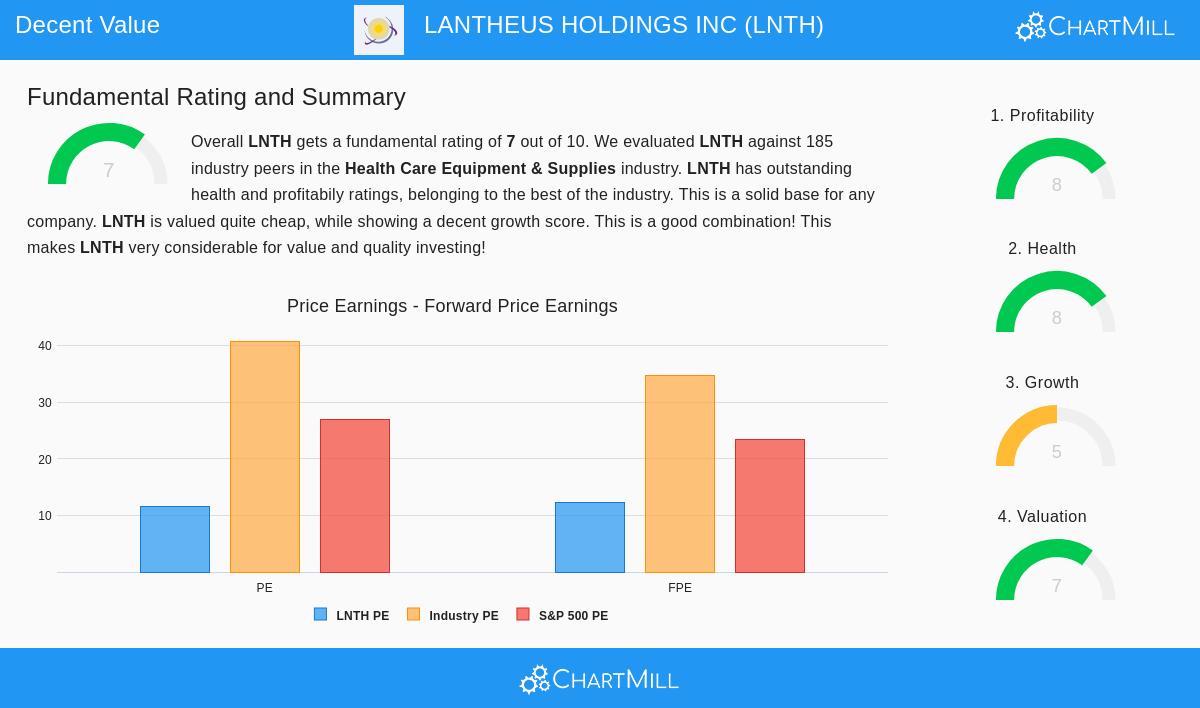

Lantheus Holdings, a supplier of diagnostic imaging and nuclear medicine products concentrating on oncology and cardiology, gets an overall fundamental grade of 7 out of 10 from ChartMill. This grade comes from a thorough review across five important categories: Valuation, Financial Health, Profitability, Growth, and Dividend. The company's profile indicates it works in the specialized and increasing area of precision diagnostics and radiopharmaceuticals, which sets the context for its financial numbers.

Valuation: The Main Draw The central idea of value investing is to find securities selling for less than their true value. Lantheus's valuation numbers seem to back this idea firmly.

- Its Price-to-Earnings (P/E) ratio of 11.57 is much lower than both the industry average (~40.76) and the wider S&P 500 average (~26.87), putting it in the less expensive range of its Health Care Equipment & Supplies sector group.

- The Price-to-Free Cash Flow and Enterprise Value-to-EBITDA ratios show a comparable picture, with LNTH being priced more affordably than about 97% and 88% of its industry rivals, in turn.

- Even on a future basis, with a Price/Forward Earnings ratio of 12.27, the stock is priced at a lower level compared to both the market and its industry.

This set of low earnings multiples implies the market might be pricing Lantheus's current earnings ability and cash flow creation below its peers.

Financial Health: A Steady Base A firm financial base is important for a value investment, as it lowers bankruptcy danger and gives the company steadiness to handle difficulties and put money into future expansion. Lantheus gets an 8 out of 10 for Financial Health.

- Solvency: The company has an Altman-Z score of 4.23, showing low short-term bankruptcy danger and doing better than almost 75% of its industry. Importantly, its debt is well-supported by free cash flow, with a Debt-to-FCF ratio of 1.37, meaning it could in theory pay off all debt in just over a year.

- Liquidity: With a Current Ratio of 2.67 and a Quick Ratio of 2.49, Lantheus has enough liquidity to meet its short-term responsibilities easily.

This sound health grade gives assurance that the company is on firm ground, a key point when judging a seemingly low-priced stock to steer clear of possible "value traps."

Profitability: Quality at a Lower Price High earnings strength is frequently a sign of a good business, and when discovered at a low valuation, it can be especially interesting. Lantheus does very well here with a Profitability grade of 8.

- The company has strong margins, with an Operating Margin of 22.63% and a Profit Margin of 10.99%, doing better than over 94% and 85% of industry peers.

- Its effectiveness in using capital is also notable, with a Return on Invested Capital (ROIC) of 13.60% and a 3-year average ROIC of 16.25%, both much higher than the industry average.

These numbers show that Lantheus is not just a low-cost stock, but an earning and effectively managed business. For a value investor, this suggests the low valuation may not be because of poor operations but possibly other reasons.

Growth: A Varied but Controllable Scene While pure value stocks occasionally lack high expansion, a filter for "acceptable value" wants a middle ground. Lantheus's Growth grade is a neutral 5, showing a change period.

- Past Results: The company has an excellent long-term history, with Revenue increasing at an average yearly rate of 34.59% and Earnings Per Share (EPS) increasing at 42.10% over recent years.

- Recent and Future View: More lately, expansion has slowed. Revenue increased a slight 1.95% last year, and EPS dropped. Experts anticipate slower, single-digit growth in both revenue and earnings going forward.

This slowing in expansion path is probably a main reason in its current valuation. For a value investor, the important question is whether the market has over-punished the stock for this shift from historically high expansion rates, especially given its continued earnings strength and financial health.

Final Thoughts and Points to Ponder

Lantheus Holdings shows a profile that matches several ideas of value investing. It trades at valuation multiples much lower than its industry and the wider market, while at the same time showing better profitability and very firm financial health. This pairing, a possibly under-priced cost for a fundamentally stable and earning business, is exactly what filters like the "Acceptable Value" screen try to find.

Naturally, the slowed expansion outlook is a key reason for investors to consider. The investment argument probably depends on whether Lantheus can maintain its high earnings strength and firm market position in its specific diagnostic and treatment areas, and if its future products can later speed up expansion again. The company's firm balance sheet and cash flow give it the means to carry out its plan.

For investors curious about finding other stocks that fit similar standards of good valuation combined with acceptable fundamentals, more study can be done using the Acceptable Value Stocks screen on ChartMill.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The analysis is based on data and grades provided by ChartMill, and investors should do their own research and talk with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.