If anyone still doubted that AI is the market’s north star, Monday’s session put that to rest.

The Nasdaq rose another 0.5%, powered by Amazon’s billion-dollar deal with OpenAI, while the Dow Jones slipped 0.5% as most industrials stumbled. Once again, the story wasn’t broad market strength, it was Big Tech leading the charge.

Amazon’s AI Play: $38 Billion for Cloud Dominance

Amazon's (AMZN | +4.00%) cloud arm AWS will supply OpenAI with access to hundreds of thousands of Nvidia GPUs, an agreement valued at roughly $38 billion.

The deal strengthens Amazon’s already growing position in AI infrastructure, adding to its earlier partnership with Anthropic and marks another milestone in the race for computing power dominance.

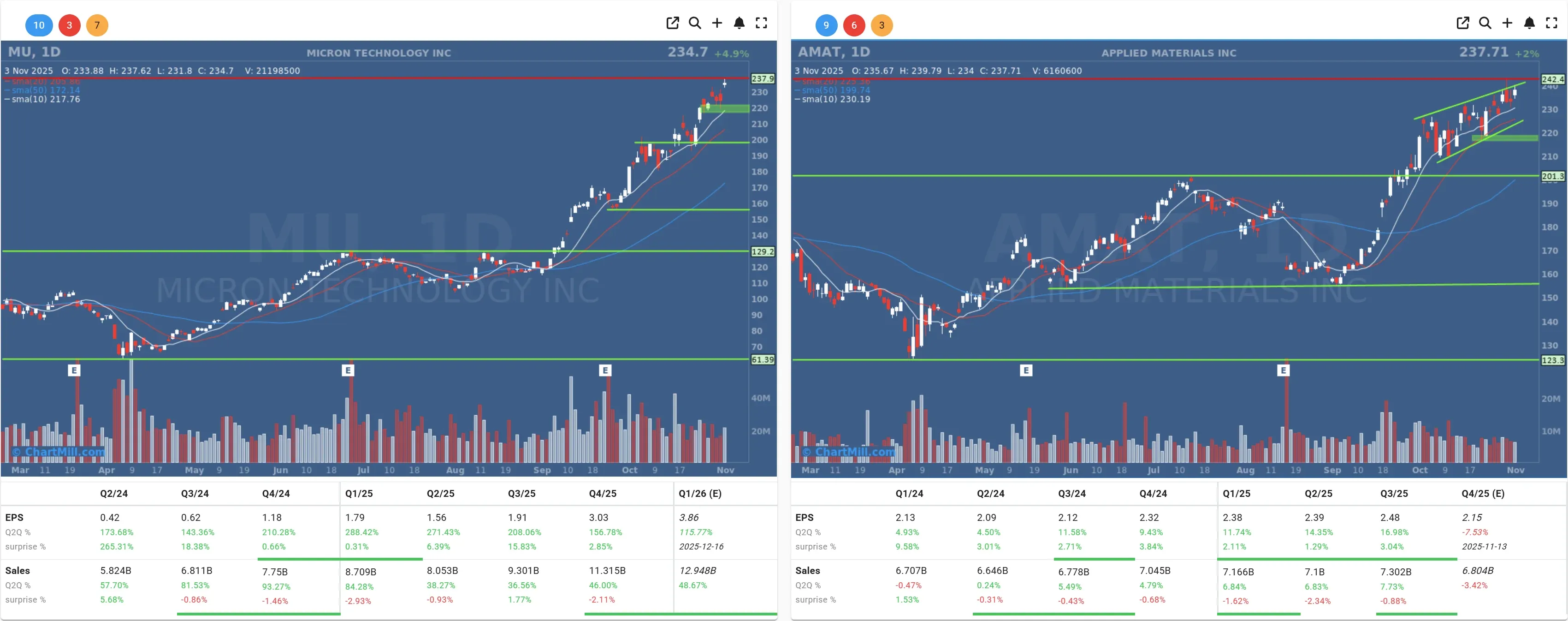

Investors loved it. Amazon’s stock surged nearly 4%, Nvidia followed higher, and even secondary players like Micron (MU | +4.88%) and Applied Materials (AMAT | +1.98%) caught a bid.

Cipher Mining (CIFR | +22.04%) stole the spotlight, though. The crypto miner inked a $5.5 billion, 15-year data center lease with Amazon, turning its bitcoin-mining facilities into AI compute farms. It’s a smart pivot, AI is proving to be the new gold rush for these data-heavy businesses.

The Bigger Picture: Narrow Leadership and Economic Unease

Despite the tech fireworks, 319 of S&P 500 stocks ended in the red (+63%) yesterday. That narrow market breadth continues to worry me. When just a handful of megacaps prop up the index, corrections tend to hit hard and fast once enthusiasm fades.

That narrow market breadth continues to worry me. When just a handful of megacaps prop up the index, corrections tend to hit hard and fast once enthusiasm fades. - ChartMill.com

On the macro side, October’s U.S. manufacturing data sent mixed signals. S&P Global reported accelerating factory growth thanks to stronger order books, yet ISM’s manufacturing index painted a gloomier picture—down to 48.7, signaling contraction. The disconnect suggests that while some firms are ramping up, others are stuck with growing inventories and weak export demand.

Meanwhile, Federal Reserve Governor Lisa Cook reiterated her support for last week’s rate cut, citing labor market weakness as a greater risk than inflation. Translation: the Fed may be open to cutting again in December if job data softens further. Wednesday’s ADP jobs report will be one to watch.

Palantir Impresses — Then Slips

Palantir (PLTR | -4.2% after hours) reported record results: revenue jumped to $1.18 billion with earnings of $0.21 per share, handily beating expectations.

Its U.S. commercial revenue surged 121% year-over-year, government contracts rose 52%, and full-year guidance was lifted to $4.4 billion. But after-hours traders still took profits, classic “buy the rumor, sell the news.”

M&A Spotlight: Kimberly-Clark Buys Kenvue

In a rare non-tech headline, Kimberly-Clark (KMB | -14.57%) announced a $48.7 billion takeover of Kenvue (KVUE | +12.32%), the Johnson & Johnson spin-off known for Tylenol.

Investors weren’t thrilled, KMB sank double digits on fears of overpaying.

Commodities and Currencies

-

Oil prices nudged higher as OPEC+ hinted at halting recent output increases.

-

Gold and silver barely moved, while crypto markets took another hit.

-

The euro weakened further to $1.1518 as bond yields inched up on both sides of the Atlantic.

Looking Ahead

Tech continues to dictate the market’s mood, but that dominance is becoming a double-edged sword. As long as AI keeps delivering blockbuster deals, bulls will stay energized. But with weak breadth and mixed macro data, the rally feels increasingly fragile.

I’ll be watching the ADP jobs report and any Fed comments closely this week. For now, Wall Street is living in a tale of two markets, AI heaven on one side, and everything else struggling to keep up.

Kristoff - ChartMill

Next to read: Breadth Crumbles Again as Mega Caps Mask Market Weakness