KB HOME (NYSE:KBH) stands out as a potential fit for long-term growth-at-a-reasonable-price (GARP) investors, based on criteria inspired by Peter Lynch’s investment philosophy. The homebuilder demonstrates solid fundamentals, sustainable growth, and an attractive valuation, making it a stock worth examining further.

Why KBH Fits the GARP Approach

- Strong Historical Growth: KBH has delivered an impressive 5-year average EPS growth of 24.25%, well above the minimum 15% threshold in Lynch’s strategy. This indicates consistent earnings expansion.

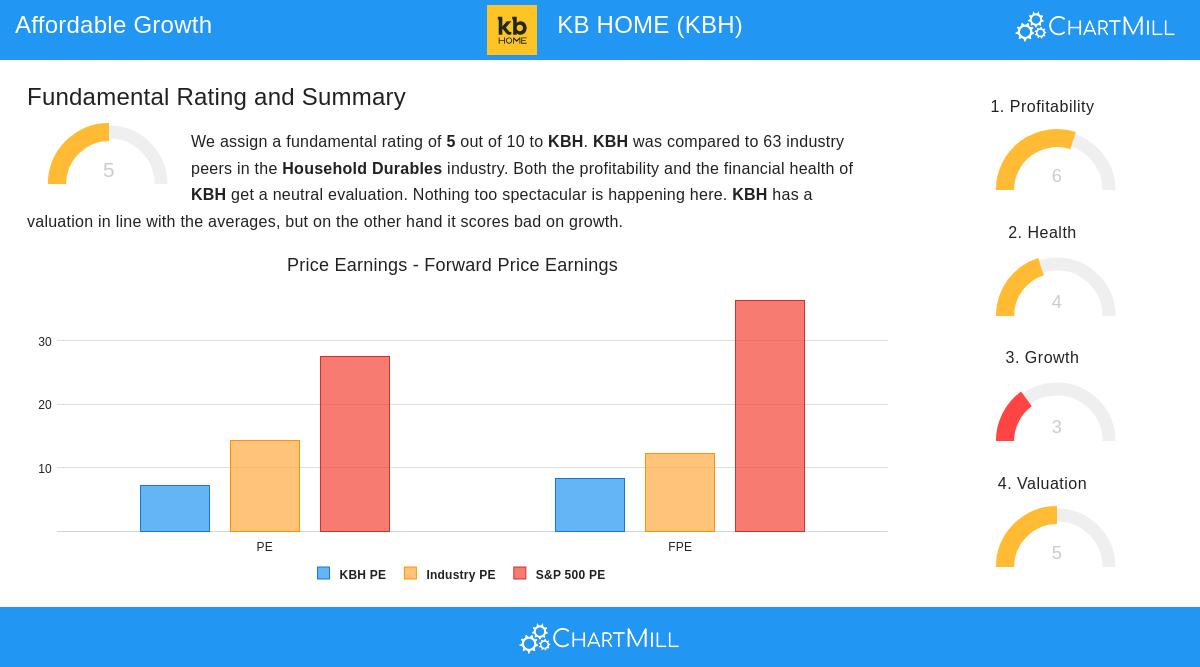

- Reasonable Valuation: With a PEG ratio of 0.29 (far below the preferred maximum of 1), KBH appears undervalued relative to its growth. Its P/E ratio of 7.14 is also significantly lower than both the industry and S&P 500 averages.

- Healthy Financials: The company maintains a Debt/Equity ratio of 0.44, reflecting prudent leverage, and a robust Current Ratio of 5.99, ensuring ample liquidity for short-term obligations.

- Profitability: KBH’s Return on Equity (ROE) of 15.18% meets Lynch’s criteria, signaling efficient use of shareholder capital.

Fundamental Analysis Summary

KBH holds a fundamental rating of 5/10, with strengths in profitability and valuation but weaker growth projections. Key takeaways:

- Profitability: Above-average margins and returns (ROE, ROIC) compared to peers.

- Valuation: Priced attractively relative to earnings and industry benchmarks.

- Growth Concerns: Expected near-term declines in EPS and revenue may weigh on performance.

For a deeper dive, review the full KBH fundamental analysis report.

Final Thoughts

While KBH’s growth outlook has softened, its historical performance, strong balance sheet, and discounted valuation make it a candidate for GARP investors. As always, further due diligence is recommended.

Our Peter Lynch Strategy screener lists more stocks meeting these criteria and is updated regularly.

Disclaimer

This is not investment advice. The observations here are based on available data at the time of writing. Always conduct your own research before making investment decisions.