For investors looking for reliable income, a disciplined screening process is needed to find truly sustainable dividend payers and avoid those with only surface-level appeal. One useful method involves selecting for companies that have a high dividend rating and also show good underlying profitability and financial soundness. This process tries to find businesses with the operational ability to keep and possibly increase their payouts over time, not those with high yields because of a falling share price or weak basics. A stock that recently appeared from this process is Johnson & Johnson (NYSE:JNJ).

Dividend Profile: A Track Record of Reliability

For dividend investors, consistency and growth are very important, and Johnson & Johnson’s past results in this area are a major positive. The company’s dividend story is one of notable reliability.

- Strong Growth History: JNJ has raised its dividend for at least 10 straight years, indicating a management focus on giving capital back to shareholders. More notably, the dividend has increased at a yearly rate of about 9.24% over the last five years, well above inflation and giving real income growth for long-term owners.

- Good Yield: The stock now provides a dividend yield of 2.48%. While not the biggest yield available, it is important to see this in comparison. This yield is higher than the average for the S&P 500 (about 1.87%) and is in the better part of its pharmaceuticals industry group, where the average yield is only 0.52%.

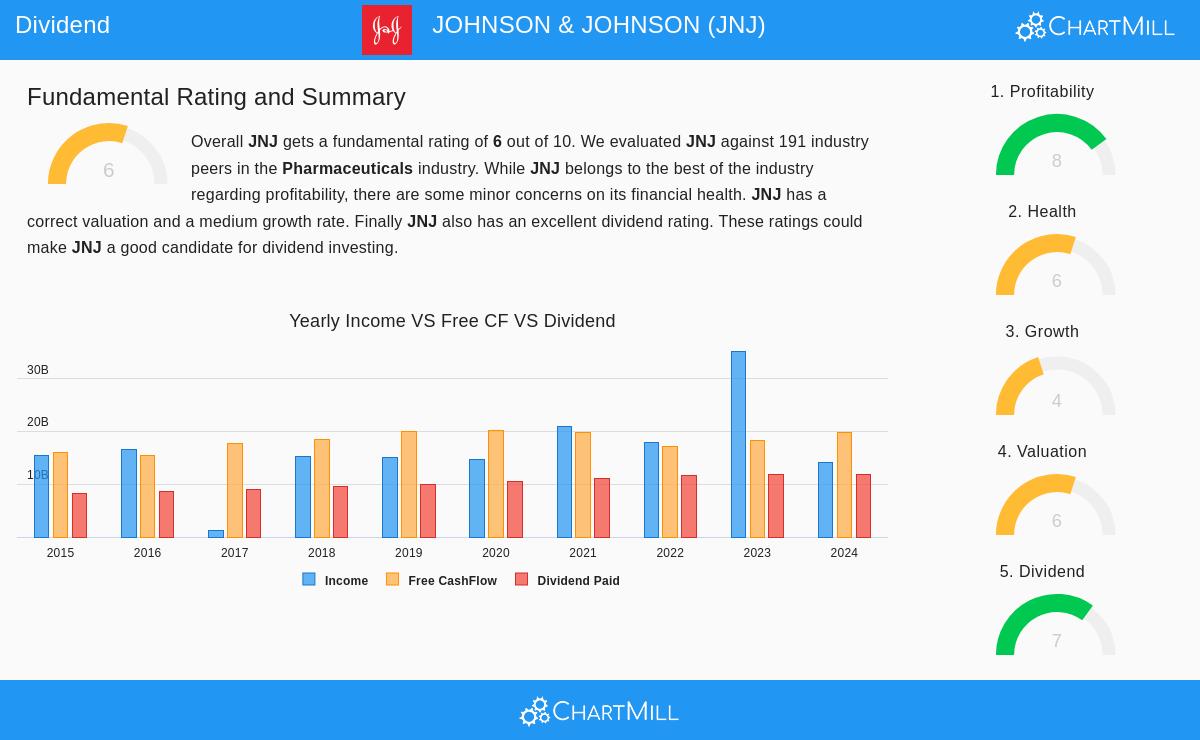

- Sustainability Factors: The main measure for checking payout safety, the payout ratio, is 48.70%. This shows the company uses just under half of its net income to pay the dividend. This level is often seen as acceptable, leaving plenty of kept earnings for putting back into the business, lowering debt, or other company projects. However, a point of attention from the fundamental study is that recent earnings growth has been lower than the dividend growth rate, a situation investors should watch to confirm long-term sustainability.

Supporting Strength: Profitability and Financial Health

A high dividend rating by itself is insufficient; it requires support from a sound business. This is where the screening rules for good profitability and health show their value, and JNJ performs well on these points.

Profitability Quality: Johnson & Johnson works with the efficiency and margin level of a top company in its field. Its profitability numbers are not just good; they are excellent.

- Return Measures: The company produces a high Return on Invested Capital (ROIC) of 14.68%, showing it uses shareholder capital well to build value. Its Return on Equity (ROE) of 31.69% is very good.

- High Margins: With a Profit Margin of 27.26% and an Operating Margin of 27.00%, JNJ keeps top-level profitability, doing better than over 90% of its industry rivals. This high profitability gives a wide advantage and a good cushion to guard the dividend during economic slowdowns.

A Firm Financial Base: Financial health makes sure a company can handle problems without putting its dividend at risk. JNJ’s profile here is not uniform but is finally steady.

- Good Solvency: The company’s Altman-Z score of 4.84 points to a very small near-term chance of financial trouble. Importantly, its debt is well-supported by free cash flow, with a Debt-to-FCF ratio of only 2.34 years, in the better part of its industry. This means JNJ could pay off all its debt with its present cash flow in a fairly brief period.

- Liquidity Detail: The screening rules asked for a minimum health rating, which JNJ satisfies, but the report mentions some lower short-term liquidity ratios (Current and Quick Ratios). Notably, the study explains this by saying that given the company’s very good solvency and profitability, these measures are less worrying and probably show the particular details of its global healthcare business rather than a basic liquidity problem.

Valuation Context

For income investors focused on the long term, valuation is important as it influences future total returns and yield-on-cost. JNJ’s valuation gives a detailed picture. Its Price-to-Earnings (P/E) ratio of 20.38 is above its own historical average but seems fair when measured against the wider S&P 500 (P/E of ~26.56) and is clearly less expensive than the average for its industry (P/E of ~32.98). This implies investors are not paying too much for this mix of yield, growth, and quality compared to other choices.

Conclusion

Johnson & Johnson represents the kind of company a disciplined dividend screen aims to find. It combines a respectable and increasing yield with the core qualities needed to maintain it: top-tier profitability and a basically sound balance sheet with good solvency. While investors should note the speed of earnings growth compared to dividend growth, JNJ’s established market positions, varied healthcare collection, and long record of shareholder returns make it a core possibility for a mixed dividend-focused portfolio.

The hunt for good dividend payers does not finish with one stock. You can review other companies that fit similar rules of high dividend quality, good profitability, and financial health by using the pre-configured "Best Dividend Stocks" screen on ChartMill.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The information presented is based on data provided and should not be the sole basis for an investment decision. Investors should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.