Value investing represents a time-tested approach to identifying companies trading below their intrinsic worth. This methodology, pioneered by Benjamin Graham and later refined by Warren Buffett, focuses on finding securities that the market has temporarily mispriced. The strategy emphasizes purchasing stocks with strong fundamentals, including healthy financials, consistent profitability, and reasonable growth prospects, at prices that provide a margin of safety. By applying systematic screening criteria, investors can identify potential opportunities that meet these strict standards.

INNOVIVA INC (NASDAQ:INVA) presents an interesting case study in value investing principles, particularly when analyzed through its detailed fundamental analysis report. The company's financial metrics across valuation, health, profitability, and growth dimensions suggest it may represent the type of undervalued opportunity that value investors historically seek.

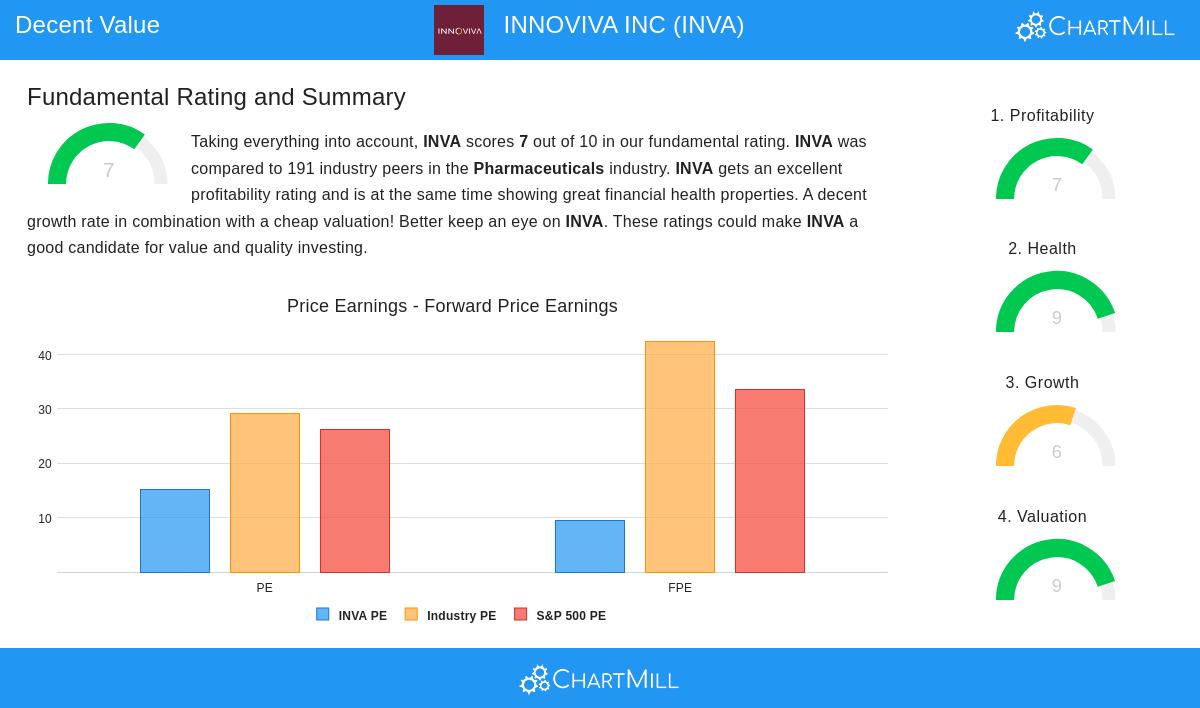

Valuation Metrics

The company's valuation profile stands out as particularly attractive, scoring 9 out of 10 in ChartMill's assessment. This high rating reflects several key advantages:

- Price-to-Earnings ratio of 15.23, significantly below the S&P 500 average of 26.28

- Forward P/E ratio of 9.49, substantially lower than the market's 33.61 average

- Enterprise Value to EBITDA ratio better than 98% of pharmaceutical industry peers

- Price-to-Free-Cash-Flow ratio cheaper than 93% of industry competitors

For value investors, these metrics indicate a potential margin of safety, a core principle in value investing where the market price provides a buffer against estimation errors in intrinsic value calculations. The company's valuation multiples suggest it trades at a substantial discount to both the broader market and its industry peers.

Financial Health Assessment

INNOVIVA demonstrates exceptional financial strength with a health rating of 9 out of 10. The company maintains:

- Current ratio of 14.12, indicating strong short-term liquidity

- Quick ratio of 13.33, surpassing 86% of industry peers

- Debt-to-equity ratio of 0.25, reflecting conservative leverage

- Altman-Z score of 3.18, signaling low bankruptcy risk

- Debt-to-free-cash-flow ratio of 1.38, suggesting rapid debt repayment capability

This strong financial position aligns with value investing's emphasis on companies with solid balance sheets that can withstand economic downturns and capitalize on opportunities during market dislocations.

Profitability Profile

The company earns a solid profitability rating of 7 out of 10, supported by:

- Return on assets of 8.91%, outperforming 91% of pharmaceutical companies

- Return on equity of 12.61%, better than 88% of industry peers

- Profit margin of 32.78%, exceeding 97% of competitors

- Operating margin of 43.21%, among the industry's highest

Value investors prioritize sustainable profitability as it indicates competitive advantages and operational efficiency. While the report notes some margin compression in recent years, the company's overall profitability remains impressive within its sector.

Growth Trajectory

With a growth rating of 6 out of 10, INNOVIVA shows promising development:

- Revenue increased 10.14% over the past year

- Five-year revenue growth averaging 6.57% annually

- Expected EPS growth of 83.16% annually in coming years

- Projected revenue growth of 12.04% per year

The accelerating growth profile, with future expectations surpassing historical performance, suggests potential catalysts that could help close the valuation gap. Value investors often seek companies where growth expectations are not fully reflected in current prices.

Investment Considerations

While INNOVIVA presents an attractive value proposition, investors should consider several factors. The company operates in the pharmaceutical sector, where intellectual property protection and regulatory developments can significantly impact future performance. Its royalty-based revenue model provides stability but also creates dependency on partner relationships and product performance.

The absence of dividend payments may deter income-focused investors, though this aligns with the company's strategy of reinvesting capital into the business. The projected acceleration in earnings and revenue growth, if realized, could serve as catalysts for price appreciation.

For investors interested in finding similar opportunities, the Decent Value Stocks screen provides a systematic approach to identifying companies with strong valuation characteristics alongside solid fundamentals.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice, recommendation, or endorsement of any security. Investors should conduct their own research and consult with financial advisors before making investment decisions. Past performance does not guarantee future results.