For investors looking for steady income, a systematic way to pick stocks is important. One useful tactic is to search for companies that provide a good dividend now and also have the basic financial soundness to maintain and possibly raise those payments in the future. This requires examining more than just the current yield to evaluate earnings, which support the dividend, and balance sheet strength, which shows the company can manage economic challenges without reducing its payout. A stock that performs acceptably in these three areas, dividend quality, acceptable profitability, and firm health, makes a strong argument for inclusion in a portfolio focused on dividends.

Hormel Foods Corp. (NYSE:HRL), the Minnesota-based packaged food company known for brands like SPAM, Skippy, and Applegate, appears as a candidate from this kind of orderly search process. The company's basic financial picture indicates it deserves further examination by investors focused on income.

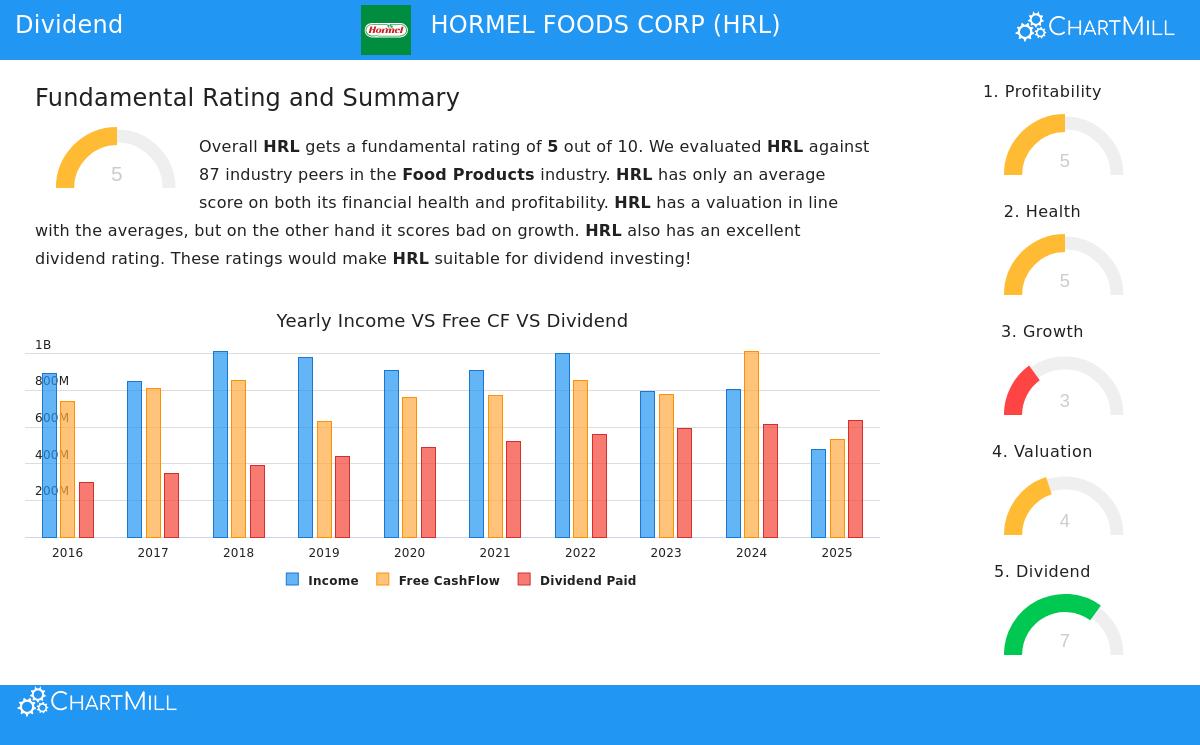

A Notable Dividend Profile

The main attraction of Hormel for dividend investors is its dependable and consistent income payment. The company's dividend measurements are good, especially when considered alongside other data.

- Good Yield: Hormel presently provides a dividend yield near 4.99%. This is much greater than the typical yield for the S&P 500 (near 1.82%) and the average for similar companies in the Food Products sector (about 2.27%).

- Established History: Reliability is vital in dividend investing, and Hormel demonstrates it. The company has both paid and raised its dividend for a minimum of ten straight years. This lengthy record of consistent payments offers some assurance of management's dedication to giving capital back to shareholders.

- Maintainable Increase: Although the dividend growth rate of about 4.9% each year is not high, it is stable and, notably, matches the company's expected earnings growth. This match is important for the tactic, as it implies the dividend raises are backed by the business's actual results instead of being paid for by borrowing or other short-term methods.

Supporting Basics: Profitability and Health

A high yield by itself can be misleading if the company's finances are weak. The search condition of needing "acceptable" profitability and health scores is meant to prevent this issue. Hormel's results in these categories, while not outstanding, offer a stable base.

Profitability is satisfactory, with the company regularly producing positive earnings and cash flow. Important measurement ratios like Return on Assets (3.57%) and Return on Invested Capital (5.99%) are good compared to others, doing better than most of its industry competitors. Still, investors should be aware of a pattern of falling profit, operating, and gross margins in recent years, which is a factor to watch. The "acceptable" profitability score accounts for this combination of firm past performance and recent margin challenges.

Financial Health is a comparative advantage. Hormel keeps a firm balance sheet with a good Altman-Z score of 3.54, showing a small immediate chance of financial trouble. Its liquidity is also acceptable, with a Current Ratio of 2.47, meaning it possesses sufficient short-term assets to meet its short-term obligations. While the company has added some debt lately and its payout ratio is now higher than usual, its general stability and liquidity situation stays firm, matching the search requirement for acceptable financial health.

Price and Growth Factors

From a strict price perspective, Hormel's stock seems fairly valued compared to the wider market and its industry. Its Price-to-Earnings and Forward P/E ratios are lower than the S&P 500 average and look good next to many industry rivals. This indicates the good dividend yield is not just because of a very low stock price.

The principal subject of attention, and the cause for the company's lower total basic score, is its growth path. Both sales and earnings per share have displayed very small growth or minor drops over the last year. While experts forecast a move back to slow, consistent growth in future years, Hormel is not a rapid-growth business. For a dividend investor using this search tactic, this is a reasonable compromise, since the main goal is safe income rather than share price gains.

Is It Suitable for a Dividend Portfolio?

Hormel Foods represents a typical example of a conservative income stock. It works in the stable consumer staples industry, has well-known brands, and maintains a long-standing practice of paying its shareholder dividend. The search process brings out its central advantages: a high, well-backed yield with a dependable increase history, supported by satisfactory profitability and a firm balance sheet. These are exactly the conditions meant to find companies that can deliver passive income during different market conditions.

For investors whose main aim is creating a flow of reliable dividend income, Hormel's characteristics are persuasive. It shows the kind of company that can act as a foundation in a dividend portfolio, providing yield and steadiness even without fast growth.

This review of Hormel was produced from a methodical search for good dividend-paying stocks. You can review the complete list of stocks that meet the criteria and perform your own review using the Best Dividend Stocks screen.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. The analysis is based on data and a search method, which involves inherent limitations. Investors should perform their own complete research, which includes examining Hormel's full fundamental analysis report, and think about their personal financial position and risk tolerance before making any investment decisions.