When looking for good dividend stocks, investors often work to balance an appealing yield with financial steadiness and lasting business performance. A systematic method looks for companies that not only have good dividend traits but also show steady earnings and acceptable financial condition. This process helps find businesses able to keep and possibly increase their dividend payouts over the long term, instead of those just giving high yields that could be unstable. By concentrating on these combined basic factors, investors can create a group of dividend-paying stocks with a lower chance of dividend reductions and better possibility for long-term income improvement.

Dividend Profile Analysis

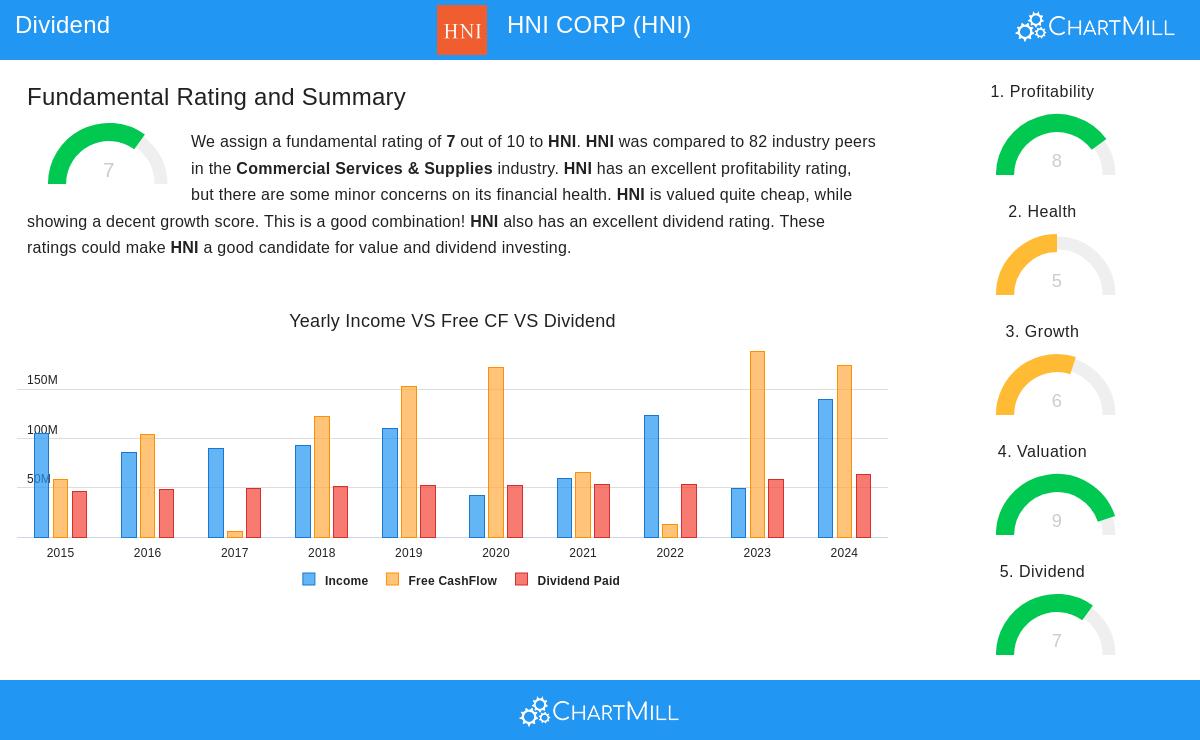

HNI CORP (NYSE:HNI) is a notable case for dividend-focused investors, receiving a ChartMill Dividend Rating of 7 out of 10. The company's dividend features show a middle ground between present income and lasting quality:

- Dividend Yield: At 3.09%, HNI gives a yield higher than both the industry average of 2.51% and the S&P500 average of 2.32%, putting it in the high end of its commercial services and supplies sector group

- Dividend Growth: The company keeps a small but steady yearly dividend growth rate of 3.58%, giving investors some safety from inflation

- Payment History: HNI has built a dependable record, having given dividends for at least 10 years without any cuts in that time

- Payout Ratio: With 42.87% of earnings used for dividend payments, the company keeps a maintainable payout level that balances shareholder returns with kept earnings for business investment

The mix of better-than-average yield, steady payment history, and acceptable payout ratio makes HNI especially interesting for investors looking for dependable income creation without high risk.

Profitability Assessment

Good profitability is the base for lasting dividend payments, and HNI does well here with a ChartMill Profitability Rating of 8. The company's skill in making returns greatly improves its ability to keep dividend payments:

- Return Metrics: HNI shows very good returns with an 18.24% Return on Equity and 11.95% Return on Invested Capital, doing better than about 85% of industry rivals

- Margin Performance: The company keeps acceptable margins in all areas, including a 5.73% profit margin and 9.04% operating margin, both placed in the high third of the industry

- Margin Trends: Importantly, all main margin groups have shown betterment in recent years, pointing to better operational effectiveness and pricing ability

These good profitability measures give important support for the dividend, as they show the company makes enough earnings to easily cover its dividend needs while paying for future growth projects.

Financial Health Considerations

While HNI's ChartMill Health Rating of 5 points to some areas to watch, the company keeps acceptable financial steadiness for dividend lasting quality:

- Solvency Strength: The company's Altman-Z score of 3.44 suggests no short-term bankruptcy worries, and its debt-to-free-cash-flow ratio of 2.74 shows it could pay back all debt needs in less than three years from operating cash flows

- Liquidity Position: The current ratio of 1.46 sits within normal limits, though the quick ratio of 0.93 hints at some possible issues in meeting short-term needs without inventory sales

- Debt Management: With a debt-to-equity ratio of 0.56, HNI keeps borrowing levels similar to industry peers, showing balanced use of debt funding

The company's acceptable solvency measures and workable debt levels give trust in its ability to handle economic changes while keeping dividend payments, though investors should watch the liquidity situation.

Valuation and Growth Outlook

HNI's good valuation and growth views make a strong total return possibility for dividend investors:

- Valuation Metrics: Trading at a P/E ratio of 12.85 and forward P/E of 10.82, HNI seems low-priced compared to both the S&P500 and industry averages

- Growth Expectations: Analysts predict good forward growth with earnings per share expected to rise by 17.14% each year, speeding up much from past growth rates

- Revenue Expansion: The company expects large revenue growth of 35.00% in coming years, suggesting basic business speed

The mix of acceptable valuation and speeding growth views indicates possibility for both price gains and dividend improvement, bettering the total return possibility for investors.

Investment Considerations

For dividend investors using a filtering method, HNI stands for the kind of middle chance that joins income creation with basic strength. The company's better-than-average yield, backed by good profitability and acceptable financial health, makes a strong case for income-focused portfolios. The acceptable payout ratio gives room for future dividend rises while keeping money for business spending. Investors can see the complete fundamental analysis report for more details into HNI's financial position and competitive benefits within the office furnishings and residential building products groups.

For investors looking for more chances that fit similar standards of good dividend traits joined with acceptable profitability and financial health, the Best Dividend Stocks screen gives often refreshed picks based on these basic filters.

Disclaimer: This article is for information only and does not make up investment advice, suggestion, or support of any security. Investors should do their own study and talk with a qualified financial advisor before making investment choices. Past results do not ensure future outcomes, and dividend payments depend on company choice and market situations.