For investors looking to balance the search for growth with prudence, the "Growth at a Reasonable Price" (GARP) method offers a practical middle path. This method looks for companies with steady growth, but steers clear of those with very high prices that assume perfect future results. By concentrating on businesses with good basic operations, including earnings and financial strength, combined with good prices, the method tries to find chances where the market might not completely recognize a company's growth path. One stock that recently appeared from this type of filter is HALOZYME THERAPEUTICS INC (NASDAQ:HALO).

A Platform for Growth

Halozyme is not a typical drug developer but a biopharmaceutical technology platform company. Its main asset is the ENHANZE drug delivery technology, which enables the subcutaneous delivery of injected drugs. This advance can change treatments that usually need long intravenous infusions into faster, more convenient injections, greatly helping the patient. The company's plan centers on licensing this technology to bigger biopharmaceutical partners, building a high-margin, royalty-based income source with several opportunities as partner products move through development and sales.

Strong Growth Path

The basic argument for Halozyme as a candidate for affordable growth starts with its notable growth measures, which are central to the GARP method. A company needs to show a clear ability to grow its business to merit investor attention, and Halozyme's recent results are solid.

- Revenue Growth: The company has shown very strong top-line increase, with revenue growing 31.19% over the past year and at an average yearly rate of almost 39% over recent years.

- Earnings Per Share (EPS) Growth: Bottom-line growth has been even more notable, with EPS rising by 48.55% in the last year and by an average of over 30% yearly in the past.

- Future Expectations: Analysts expect this trend to persist, with predicted average yearly EPS growth of 18.74% and revenue growth of 14.28% over the next years.

This mix of strong past performance and a good future growth outlook is exactly what growth-focused filters aim to find.

Good Valuation Picture

While growth is necessary, the "reasonable price" part is what distinguishes GARP from pure momentum investing. A stock must be priced in a way that does not already account for many years of perfect performance. Halozyme's valuation measures indicate it trades at an interesting point relative to both its own future and the wider market.

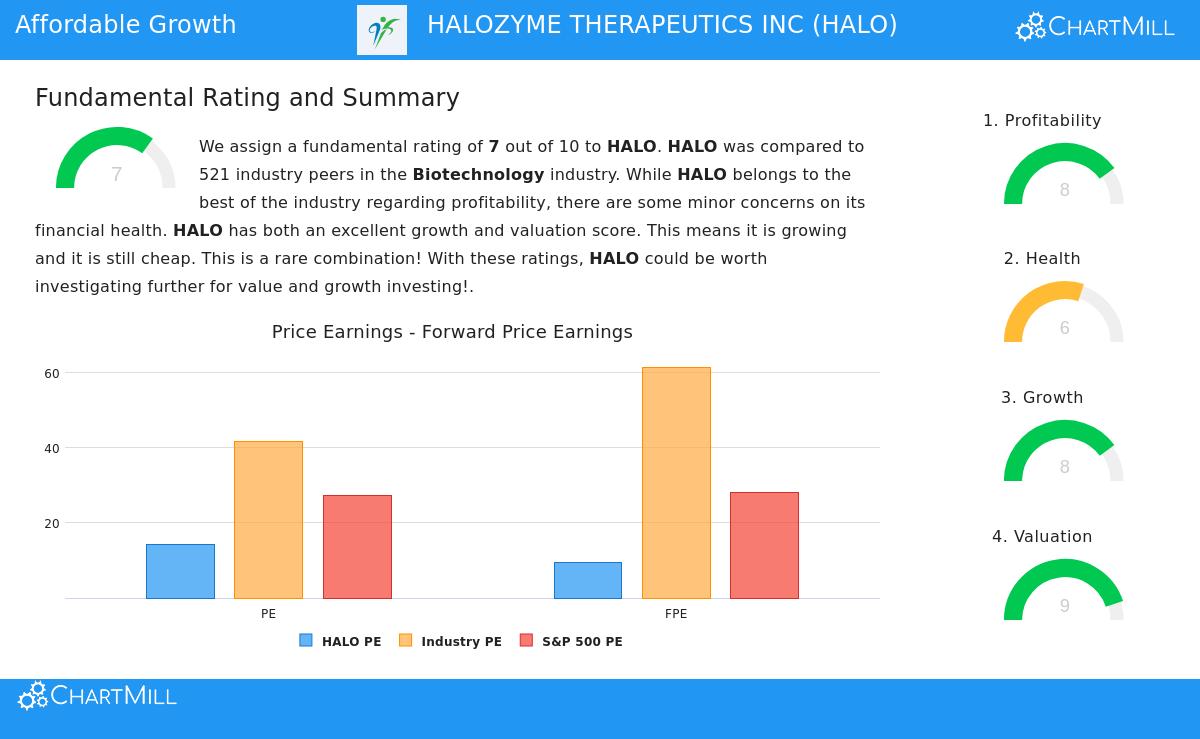

- Price-to-Earnings (P/E): The company's P/E ratio of 14.11 is seen as reasonable on its own. More significantly, it is less expensive than about 97% of similar companies in the biotechnology industry and is much lower than the S&P 500 average of 27.19.

- Forward P/E: Looking forward, the valuation seems even more interesting. Halozyme's forward P/E ratio of 9.53 is less expensive than almost 98% of its industry and below a third of the S&P 500's average.

- Other Multiples: The good valuation applies to other measures. The company's Enterprise Value to EBITDA and Price to Free Cash Flow ratios are also less expensive than over 96% of industry rivals.

This valuation view suggests the market may be applying a large discount to Halozyme, possibly because of its specialized platform model or wider sector mood, creating a possibility if its growth story continues.

Supporting Basics: Earnings and Strength

For a growth story to last, it must be supported by earnings and financial strength, important checks in an affordable growth filter to avoid "growth without regard to cost" cases. Halozyme performs well here.

Earnings are a particular strong point, with a ChartMill rating of 8 out of 10. The company has very high margins, including an Operating Margin of 59.33% and a Return on Invested Capital (ROIC) of 42.77%, which are near the best in its industry. This shows its platform licensing model is very efficient and can grow.

Financial Strength shows a more varied but generally acceptable situation, with a rating of 6. The company creates substantial value, as its ROIC is much higher than its cost of capital, and its debt levels compared to cash flow are workable and better than most peers. The main point to watch is its liquidity ratios (Current and Quick Ratio), which are sufficient but lower than many industry rivals. This is an item for investors to note, though it is offset by good solvency measures like a healthy Altman-Z score.

Conclusion

Halozyme Therapeutics presents an interesting profile for investors focused on the affordable growth category. It joins a new, royalty-creating technology platform with clear high-margin growth, both in the past and in projections. Importantly, this growth is available at a price that seems modest compared to its own industry and the wider market. While its financial strength has a small area to watch regarding liquidity, its excellent earnings provide good support. This match of solid growth, fair price, and sound basic operations is the core of a GARP investment case.

For investors interested in reviewing other companies that fit similar standards of acceptable growth, decent basics, and fair valuation, more results are available using this Affordable Growth stock screen.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The analysis is based on data and ratings provided by ChartMill, and investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.