For investors looking to assemble a portfolio of lasting, high-performing companies, the principles of quality investing offer a useful framework. This method centers on finding businesses with durable competitive strengths, sound financial condition, and the capacity to produce above-average returns on capital over many years. One applied technique for finding these companies is the "Caviar Cruise" stock screen, a systematic filter made to point out firms with a demonstrated record of profitable growth, effective capital use, and strong cash generation. The screen focuses on measurable data like steady revenue and earnings growth, high returns on invested capital, reasonable debt levels compared to free cash flow, and superior profits.

A recent run of this screen pointed to W.W. Grainger Inc. (NYSE:GWW) as a possible candidate. The industrial distributor of maintenance, repair, and operating (MRO) products seems to match several central ideas of the quality investing philosophy. By looking at the specific measures from the Caviar Cruise screen, we can evaluate how Grainger's financial profile compares.

Matching the Central Measures for Quality

The Caviar Cruise screen uses a group of basic filters to find companies with a good historical record. Grainger's reported data suggests it meets these important checks:

- Profitable Growth: The screen asks for a minimum 5% compound annual growth rate (CAGR) for both revenue and EBIT (earnings before interest and taxes) over five years. Grainger passes both points, with a revenue CAGR of 6.65% and a more notable EBIT CAGR of 13.83%. Importantly, EBIT growth rising faster than revenue growth—as seen here—points to better operational efficiency and possible pricing strength, signs of a quality business with competitive edges.

- Superior Capital Use: Maybe the most important measure for quality investors is Return on Invested Capital (ROIC), which calculates how well a company produces profits from its capital base. The screen requires an ROIC (leaving out cash, goodwill, and intangibles) above 15%. Grainger's number of 33.65% is outstanding, suggesting the company uses its capital with notable efficiency to build shareholder value.

- Financial Strength: To confirm stability, the screen checks debt against free cash flow (FCF), with a ratio below 5 seen as good. Grainger's Debt/FCF ratio of 1.92 is positive, showing it could pay off all its debt in under two years using its present cash flow. This gives a clear margin of safety and financial room to maneuver.

- Superior Earnings: The screen checks for "profit quality," calculated as the five-year average of free cash flow as a percentage of net income. A number above 75% shows that accounting profits are becoming real, usable cash. Grainger's average of 87.44% means high-grade earnings that are less likely to be affected by accounting changes and more ready for dividends, share repurchases, or new investment.

A Look at Grainger's Basic Financial Condition

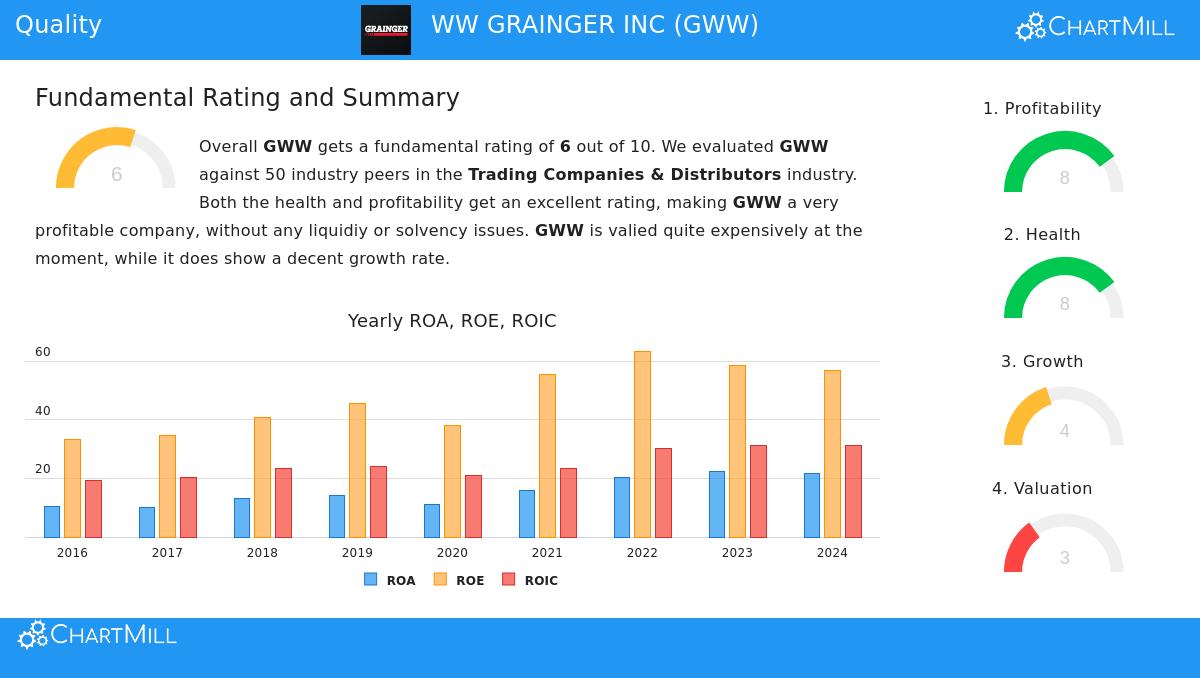

A check of Grainger's wider basic analysis report supports the image shown by the screen. The company gets a total score of 6 out of 10, with its best showings in profitability and financial condition.

- Profitability is a Main Positive: Grainger scores an 8 here, with high marks. Its ROIC of 27.94% and Return on Equity of 48.58% sit in the best group of its industry. Margins have shown good direction, and the company has had positive operating cash flow for years.

- Good Financial Condition: With a score of 8, the company's balance sheet is solid. The very good Debt/FCF ratio is mentioned, and its Altman-Z score of 11.42 shows very little bankruptcy risk. While the debt-to-equity ratio is typical for the industry, the report states the total debt level is very easy to handle.

- Price and Growth Points: The report notes price as a relative question, with a score of 3. Grainger's P/E ratio is seen as high on a basic view, though it matches industry and market averages. The growth score is a middle 4, recognizing good past growth in revenue and EPS but noting that analyst views for future growth are more measured. The dividend, while reliably increasing, gives a fairly low yield.

You can review the full, itemized basic analysis for GWW here.

Why This Fits with Quality Investing

The Caviar Cruise measures are not random, they are directly connected to the long-term aims of a quality investor. A high and increasing ROIC indicates a lasting competitive edge—in Grainger's situation, probably coming from its wide product range, distribution system, and established customer connections in the MRO field. A strong cash conversion number and low debt load give the toughness to handle economic slowdowns and the ability to seize chances without weakening shareholders. Together, these features describe a business made to increase value over many years, which is the final aim of the quality investing method.

Is It a Quality Stock for Your Portfolio?

W.W. Grainger offers a useful example of a company that meets a strict, number-based screen for quality traits. Its outstanding returns on capital, history of profitable growth, and strong balance sheet fit the aim of holding excellent businesses for the long term. For investors, the main point highlighted by the basic report is if the present market price, which seems high on some measures, properly pays for this high-grade profile. As with any screen, it works as a first step for more detailed study into the company's competitive place, leadership, and future growth sources.

Find Other Quality Candidates The Caviar Cruise screen can help find other companies with similar strong financial traits. You can see and adjust the present screen results here.

,

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation to buy or sell any security, or an endorsement of any investment strategy. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions.