The search for undervalued companies is a foundation of value investing, a method established by Benjamin Graham and commonly used by Warren Buffett. This approach focuses on finding stocks trading below their intrinsic value, usually identified through analysis of a company's financial condition, earnings, and future possibilities. A careful method needs not only locating an inexpensive stock, but one that is fundamentally healthy, steering clear of the dangers of "value traps" where a low price points to business problems instead of potential. One way to simplify this search is by using systematic filters that select for stocks with good valuation numbers combined with acceptable results in other important fundamental categories.

A recent scan using this "Decent Value" filter pointed to Frontdoor Inc (NASDAQ:FTDR), a company offering home service plans and warranties through brands such as American Home Shield. The filter looked for companies with a good valuation score, signaling a possibly low stock price, while also keeping adequate levels of earnings, financial soundness, and expansion. This mix is important; a low valuation by itself is not useful if the company loses money or carries too much debt. Frontdoor's fundamental report indicates it might be a situation where the market price does not completely account for its operational qualities.

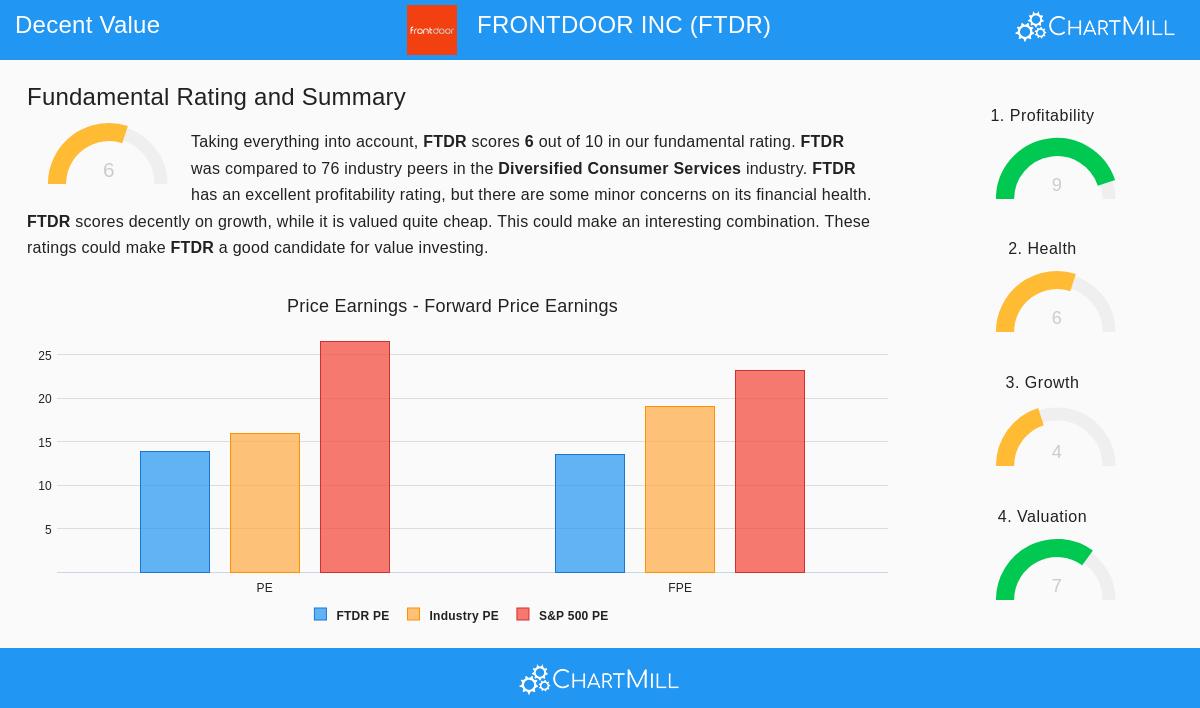

Valuation: An Appealing Entry Point

For value investors, valuation is the main area of focus. The aim is to pay much less than a company's intrinsic worth, creating a "margin of safety." Frontdoor's valuation numbers seem to provide this. Based on its detailed fundamental analysis, the stock is trading at a lower price compared to both the wider market and similar companies.

- Price-to-Earnings (P/E) Ratio: At 13.84, Frontdoor's P/E ratio is lower than the S&P 500 average of about 26.6. More significantly, it is lower than 75% of the companies in the Diversified Consumer Services industry.

- Forward P/E Ratio: The forward-looking number of 13.58 shows a similar situation, meaning a valuation lower than over 76% of industry rivals.

- Price-to-Free-Cash-Flow: This is a particularly important number for value investors, since free cash flow is a major part of intrinsic value estimates. Frontdoor is priced lower than almost 83% of its industry by this measure.

These numbers imply the market may not fully recognize the company's earnings and cash production ability, a typical beginning for value-focused study.

Profitability: A Base of Quality

An inexpensive stock is only a good investment if the business itself is sound. This is where Frontdoor's profile grows more interesting. Its profitability score is very high at 9 out of 10, putting it with the best in its industry. High profitability is a main protection against value traps, as it shows a workable, profitable business.

- The company has notable returns, including an 11.81% Return on Assets (better than 85.5% of similar companies) and a significant 83.23% Return on Equity (better than 98.7% of similar companies).

- Margins are good, with a Profit Margin of 12.87% and an Operating Margin of 20.70%, both placed in the high group of its industry.

- Importantly, Frontdoor has been regularly profitable and cash-flow positive for the past five years, showing business model strength.

This degree of profitability offers a firm base. It suggests the company's low valuation is not a sign of weak operations but could be a market mistake.

Financial Health: A Varied but Acceptable View

Financial health is the support that lets a company survive economic declines and spend for future development. Frontdoor's health score is a moderate 6, showing some points of quality next to areas for investors to watch. A value investor must evaluate if the balance sheet concerns are sufficiently balanced by the low stock price.

- Qualities: The company seems solvent with an Altman-Z score (3.50) that shows low short-term bankruptcy risk and is better than 80% of the industry. Its Debt-to-Free-Cash-Flow ratio of 3.41 is also positive.

- Note: The main point of attention is a somewhat high Debt-to-Equity ratio of 3.64, which shows a significant use of debt and is poorer than almost 79% of industry peers. However, this is partly balanced by the high profitability and cash flow, which indicate the company can manage its debt.

Growth: Steady History with Careful Future

Growth adds a possible driver to the value case. Frontdoor's growth score is a neutral 4, showing a firm historical record next to more limited expectations going forward. Value investors frequently look for companies with stable, foreseeable growth more than very high growth, as the latter is seldom found at a low price.

- Past Results: The company has produced strong recent growth, with Earnings Per Share (EPS) up 25.23% and Revenue up 11.88% over the past year. The 5-year average EPS growth rate is a solid 12.08%.

- Future Projections: Analyst estimates point to a reduction, with an expected average yearly EPS decrease of 8.44% and Revenue growth of about 5.23% over the next few years. This expected earnings drop is probably a major reason for the stock's low valuation.

For a value investor, the issue is whether the market has reacted too strongly to this expected reduction, particularly given the company's established high profitability and cash flow generation.

Conclusion

Frontdoor Inc. shows a profile that matches several value investing ideas. It trades at a noticeable discount to the market and its industry based on common valuation measures, while showing first-rate profitability and a mostly solvent financial state. The expected short-term earnings challenge clarifies the market's doubt but also forms the possible chance. The investment idea depends on whether the company's strong cash-producing business and leading market place in home warranties can maintain value over time, letting the stock price adjust to a higher intrinsic value.

This study of FTDR came from a systematic filter for decent value stocks. Investors curious about finding other companies that fit similar standards of good valuation combined with firm fundamentals can review the Decent Value Stocks screen on ChartMill.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The analysis is based on data and ratings provided by third parties. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.