For investors looking for chances where the market price may not completely show a company's basic strength, a disciplined screening method can be a helpful first step. One such process looks for stocks that show good fundamental condition and earnings, but trade at prices that seem low compared to these traits. This fits with main value investing ideas, which center on finding differences between a stock's price and its real business worth. The aim is to find companies that are financially stable and able, but priced as though they are not, possibly providing a buffer for people investing for the long term.

A recent filter using this idea found Frontdoor Inc (NASDAQ:FTDR), the company offering home service plans under names such as American Home Shield. The filter selected for stocks with a high ChartMill Valuation Rating (above 7) while also keeping acceptable scores in Earnings, Financial Condition, and Growth. This pairing indicates a company that is doing well but may be priced cautiously by the market. A more detailed examination of Frontdoor's fundamental report shows the details behind these scores.

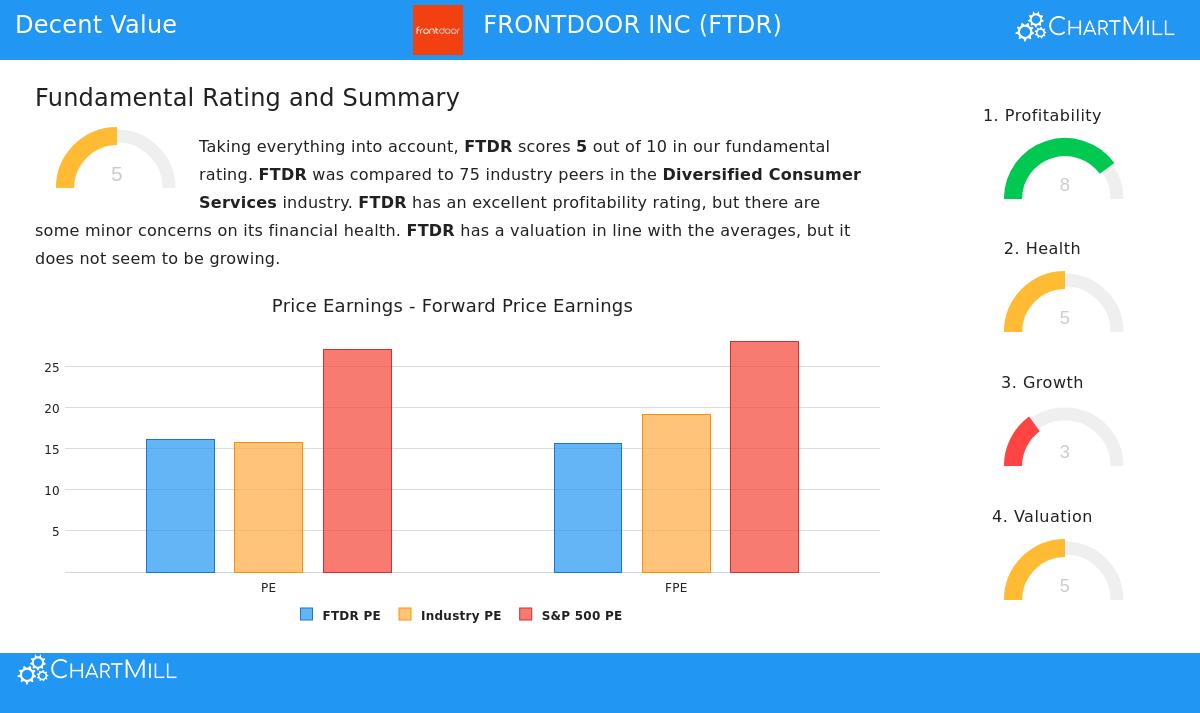

Valuation Measures: Trading at a Lower Price

The main attraction of FTDR from this filtering view is its price. The company's Valuation Rating of 7 comes from measures that look good next to both its industry and the wider market.

- Price-to-Earnings (P/E): FTDR's P/E ratio of 16.12 is seen as acceptable. However, it costs less than about 71% of similar companies in the Diversified Consumer Services industry and is much lower than the present S&P 500 average of 27.11.

- Forward P/E: The view is similar for the future, with a Forward P/E of 15.66. This is also under the industry average and notably less than the S&P 500's forward multiple.

- Enterprise Value to EBITDA & Price/Free Cash Flow: These other valuation measures support the idea. FTDR costs less than 65% of its industry based on EV/EBITDA and has a more attractive price than 80% of similar companies based on its Price/Free Cash Flow ratio.

While a high PEG ratio (which includes growth) and negative earnings growth forecasts soften the valuation view a little, the full data shows the stock is not priced for the best outcome. For an investor focused on value, this makes a situation where the company's operational positives, explained next, are being bought at an acceptable cost.

Earnings and Financial Condition: A Good Operational Base

A low-priced stock is only a worthwhile find if the basic company is stable. This is where FTDR's filter scores for Earnings (9) and Financial Condition (6) become important, as they cover the "quality" part of the search requirements.

Earnings are a clear positive for Frontdoor. The company produces notable returns on its capital:

- Return on Equity of 83.23% puts it in the highest group of its industry.

- Return on Invested Capital of 17.51% is also with the best in its field and has been above 20% on average for the last three years.

- Margins are strong, with a Profit Margin of 12.87% and an Operating Margin of 20.70%, both doing better than a big majority of industry rivals.

Financial Condition shows a more varied, but workable, picture. The company has no remaining debt, a big plus that leads to a good Debt-to-Free-Cash-Flow ratio. Its Altman-Z score shows no short-term bankruptcy danger. The main issue is a high Debt-to-Equity ratio of 3.64, which points to a dependence on debt for funding. However, it is important that this ratio is still lower than that of many industry peers, and the company's good cash flow production helps lower the connected risks. Liquidity measures like the Current and Quick ratios are sufficient and above industry averages.

Growth Points: A Developed Picture

The Growth rating of 4 is the lowest of the group and is the most important warning for the investment case. The report shows good past growth in Earnings Per Share, which has risen over 21% in the last year. However, the view has changed. Analysts now predict a drop in EPS over the next few years, while revenue is expected to increase at a slow rate. This forecasted reduction in earnings growth is the main element lowering the growth score and is probably a reason for the stock's lower valuation multiples. For a value investor, this highlights the value of the "buffer" given by the present price, the market seems to be including this difficult growth view, possibly lowering the price too much for the company's steady earnings and good market place in home warranties.

Conclusion

Frontdoor Inc. shows the kind of company a "acceptable value" filter tries to find: one with clearly good earnings and satisfactory financial condition, trading at price levels that do not seem to completely include these positives. Its high returns on capital and industry-best margins compare with a P/E ratio that is at a lower price than both its industry and the wider market. While its growth path is expected to slow and its use of debt is above preferred levels, these seem to be recognized in the present stock price. For investors using a value-focused plan, FTDR offers a situation where good company basics meet a careful market price, justifying more investigation.

Interested in finding other stocks that match this description? You can use this "Acceptable Value" filter yourself to see the present outcomes here.

,

Disclaimer: This article is for information only and is not financial guidance, a suggestion, or an offer to buy or sell any securities. The examination is based on given data and filtering methods described, which have built-in limits. Investors should do their own complete research and think about their personal money situation and risk comfort before making any investment choices.